As financial markets race up and down on the rudderless barrage of high frequency robots again this week, an excellent article from Germany’s DER SPIEGEL offers a thoughtful update on the erroneous and now eroding belief that central banks are in charge, able to drive growth or control stock markets.

In fact whether it be Janet Yellen, Mark Carney(ex-Goldman Sachs) or Mario Draghi(ex-Goldman Sachs), the relentless obsession with Central Bank circus reminds of how far away from productive, intelligent financial decisions the world remains, now 7 long years since the financial crisis first broke.

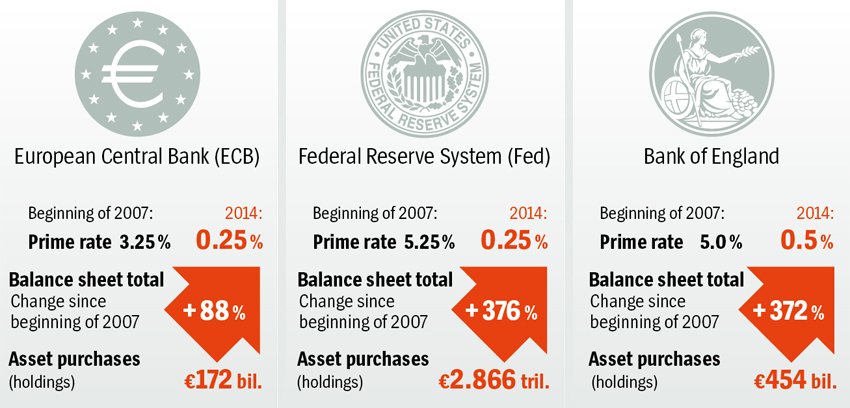

The following graphic captures the cost of 7 years of Central Bank hubris and political chaos, as policymakers continue to toss trillions into grotesquely bloated and recklessly governed investment banking conglomerates. In short: a flurry of foolish sound and fury, accomplishing nothing, while setting meaningful reforms and recovery further behind.

Read the whole excellent article here: Out of Ammo? The eroding power of central banks:

That’s because much of the money flowing into the financial sector did not reach the private sector in the form of credit, as central bankers had expected. Instead, banks are pumping it into the stock market, where prices have reached dizzying highs in recent months. Values are now approaching levels similar to those before Black Friday in 1929 and the bursting of the dotcom bubble 70 years later.

Part of the blame lies with politicians in Washington, who are unable to agree on the federal budget. Companies don’t invest as long as they don’t know how their tax burden will look in the coming years, and as long as they don’t invest, the economy will remain sluggish. The central bank’s fuel isn’t reaching the engine, [Dallas Fed Richard] Fisher warns, adding that it is bubbling in a giant gas tank that could explode at any moment.

If that happens, how can inflation be prevented, Fisher asks? How should the monetary watchdogs react if [when] the markets collapse? And how will citizens respond to the losses that the central bank will inevitably incur if treasury securities lose value? Will they accept this without complaint, or will they bend to the will of politicians on the fringes of the left and right, who argued in the last presidential election that the Fed should be placed under government control?

While ending this period of reckless policies will be a relief and a necessary step to recovery, none of it will be able to make whole on the trillions wasted and savers who will be further decimated in the next round of market losses.

Meanwhile even the much celebrated (and exorbitantly paid) Mr. Carney (“The Star” as Der Spiegel sardonically dubs him) is deservedly losing his luster in England–an inevitable outcome when one over-promises and under-delivers so much:

“…the newcomer’s aura has faded considerably. As the British pound strengthens and real estate prices rise to worrying levels in several regions, Carney is coming under growing criticism. Many are beginning to notice that the Bank of England’s balance sheet is still completely bloated, because England’s monetary watchdogs bought large amounts of government debt during the crisis.

“I suspect,” says Martin Weale, a member of England’s Monetary Policy Committee, “people might be expecting a bit too much of (central banks).” In the end, he explains, a central bank has only one central instrument: the interest rates. “You can’t deliver four or five different things with it.”