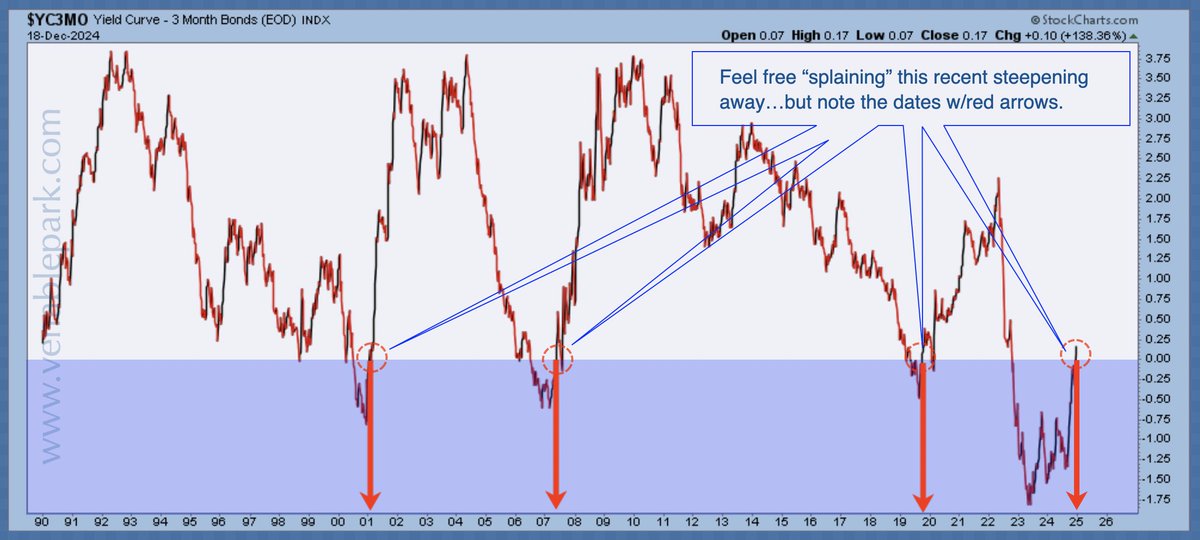

Relentless QE from central banks pushed borrowing rates (and thus investment yields) to all time lows over the past 5 years, and two mounting costs appeared.

One was that the world piled on trillions more in debt at every level from households to corporations and governments, leaving the economy today more levered and fragile than it was heading into the 2008 credit crisis. The second, is that the people who have savings to lose and/or manage for other people, have become increasingly more inclined to reach for higher risk securities. As this buying pushed prices skyward, capital risks surged. As with all such cycles, the longer and higher prices have climbed, the more confident and convinced people become of their investment ‘genius’.

In North America one of the areas attracting much confident capital has been high risk corporate debt and equity products focused on (can’t lose?) real estate–commercial (retail and office space) and multi-unit residential. Prices in established cities like New York, Houston, San Fransisco, Vancouver, Calgary and Toronto went wild.

The trouble is that surging investor flows have produced even more properties/supply, more leverage and increasingly weaker investment prospects. This was always destined to end badly. The only question has been when. And ‘when’ seems to have started. See US Commercial Property prices drop for first time in 6-years:

U.S. commercial real estate prices dropped in January for the first time since 2010, a sign of weakening demand by investors after a six-year rally that pushed values to records.

The Moody/RCA Commercial Property Price Index slipped 0.3 percent from December, Moody’s Investors Service said in a statement Monday. The decline was led by office and industrial buildings, which each had a price drop of more than 1 percent.

“This is a significant milestone that signals that a shift in sentiment among commercial-property investors is under way,” Moody’s said in the statement.

Volatility in financial markets may be hurting real estate demand. Rates of return are falling and it’s “very difficult” to bundle and sell real estate loans, hindering debt financing for transactions, Jon Gray, head of real estate for Blackstone Group LP, said at a conference last week. His company is the largest private equity property investor, with about $94 billion under management in real estate.