As we have seen repeatedly throughout history, highly levered housing is full of downside for buyers/borrowers, the economy and taxpayers (thanks to government-backed mortgage insurance). Finally the Canadian government has announced that it wants to introduce ‘risk-sharing” with lenders. What a novel concept–re-connecting the risk of capital loss on bad loans to those who have extracted front-end profits initiating them! As mortgage lenders and realtors cry foul at the prospect of slowing sales, it is outrageous that it has taken so long for this commonsense nexus to be put back into the lending decision. See: What Ottawa’s new mortgage rules could mean for Canada’s banks:

Ottawa also announced that it will launch a public consultation in the coming months to examine the possibility of introducing “lender risk-sharing.” This means banks would have to pay a deductible on mortgage insurance provided by Canada Mortgage and Housing Corp. and its private counterparts, and effectively shoulder more of the risk for mortgage defaults.

Banks would also be forced to retain more capital and raise their funding costs, which would likely be passed on to consumers with higher mortgage rates.

“We’ve had some concerns with regards to the Canadian banks in terms of their growth prospects. And when you’ve got Canadian consumers as leveraged as they are, you do have the risk of credit losses mounting, but maybe more immediately is the difficulty in achieving the same rates of growth,” Horan said.

Yes this will necessitate higher down-payments, and less buyers, and that is precisely what is needed to reintroduce some realistic pricing into the real estate equation in Canada. It should have been this way from the outset. The mess irresponsible lending policies have made, is all around us, and we will all be paying for the clean up. See Toronto Life, Mortgages for all:

“…Toronto is where all the euphemisms converge: non-prime mortgage lending to bruised-credit borrowers by less-regulated entities—better known as “shadow lending”—has existed for ages, but it has been on the rise over the last few months in this city, and elsewhere in Canada as well. The Bank of Canada is nervously keeping tabs on the non-prime trend and in the past year has begun sounding alarm bells. “A sizable proportion of new, uninsured mortgages are being issued to riskier borrowers,” it announced last December, calling the situation “worrisome.”

To repeat: booking sales on things like autos and real estate to buyers who cannot actually afford to pay for them is not business genius, it’s a Ponzi operation that enriches a few for a while and then comes back to exact a painful cost from our economy, household stability and social fabric. Higher lending standards and lower prices are needed to restore some fiscal sanity and sustainability. Both appear to be happening now, at long, long last. See: More evidence Vancouver housing bubble is bursting.

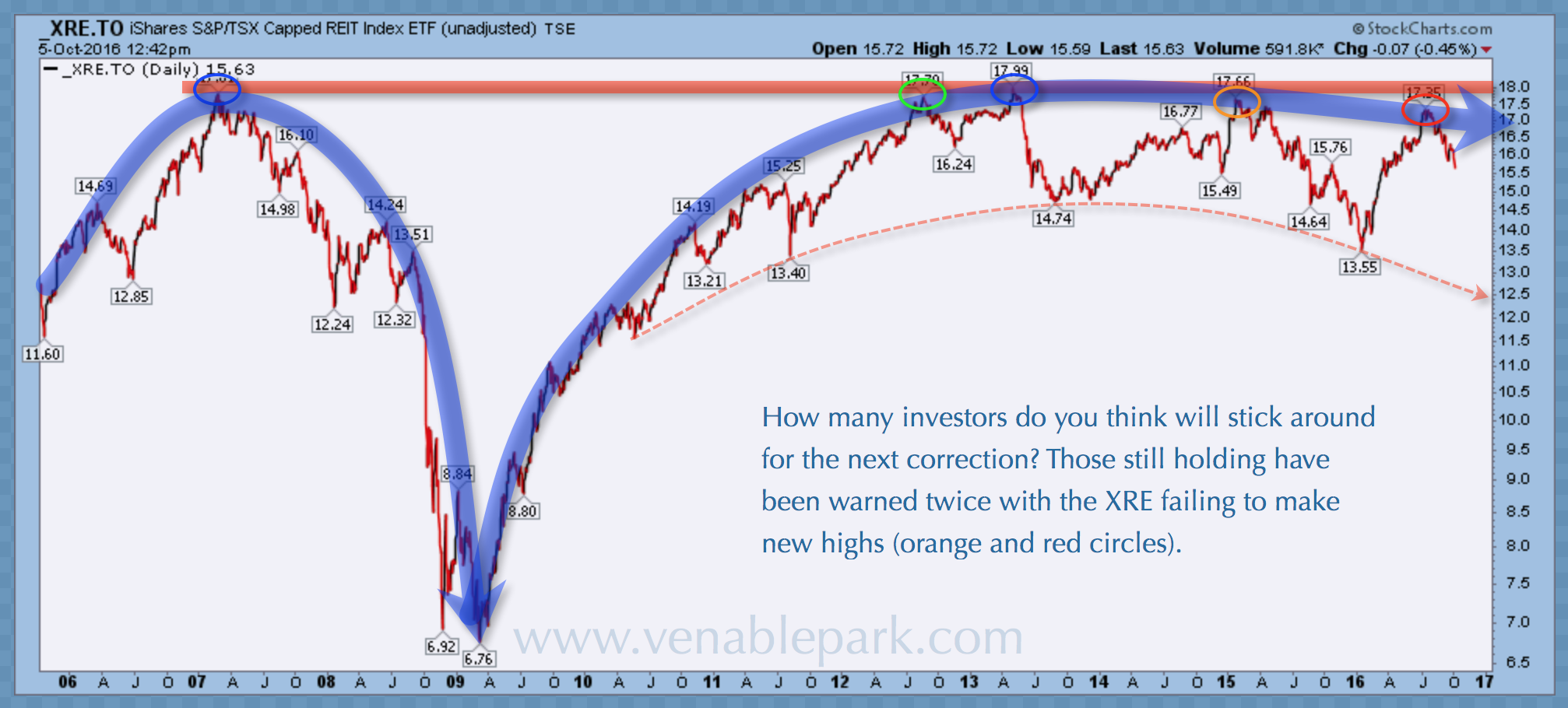

Same goes for the companies that invest in Canadian real estate and are now up to their max in over-valued assets. This chart courtesy of my partner Cory Venable, shows the Canadian Real estate investment trust ETF (XRE) since 2006 on an ex-dividend basis, and what happened to share prices in 2008-09 (-57%) as well as the loss risk facing holders today. Down nearly 9% since July, much greater mean reversion is very likely still to come as Canadian realty prices continue to roll over, loan defaults spike and vacancies mount. Far from the ‘conservative’ income investments, so many thought they were enjoying, REIT holders today have a dangerous tiger by the tail.

As REITs follow real estate into a much deserved repricing cycle, the over-bought Canadian banks (here the XFN in purple) are surely not far behind. The easy money, lax lending hallucinogens that levitated both sectors over the past 5 years, are due to retreat.