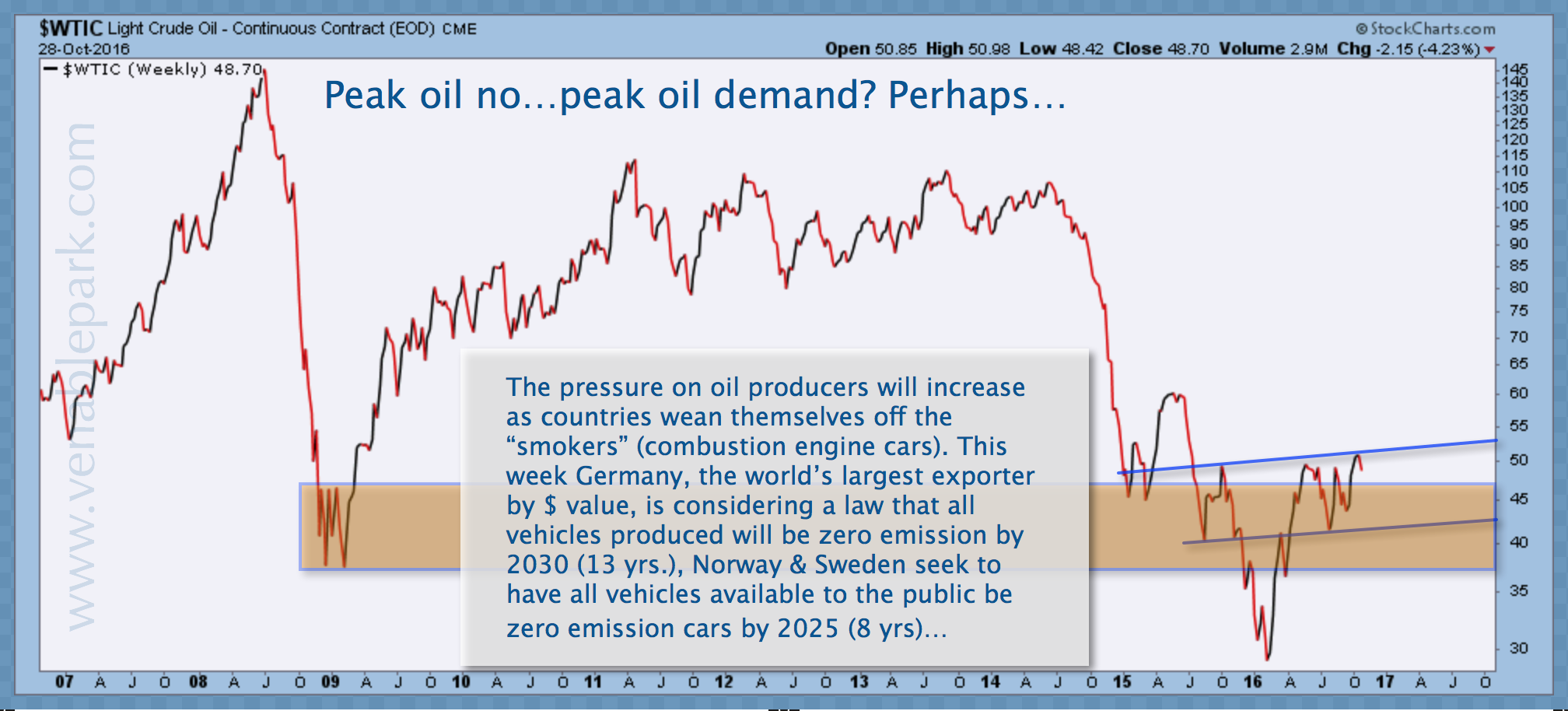

Oil (WTIC) fully retraced its September 28 to October 19 “OPEC freeze” hope rally this morning. Down nearly 12% from the latest October peak around $52/barrel, it broke below $46 in early trading. Trouble is OPEC’s output hit an estimated all time high of 33.82 million barrels a day in October, even as members Iran, Nigeria, Libya and Iraq are still seeking an exemption from production cuts in any agreement that may be reached on November 30. Never mind the long history of members cheating and pumping more even when they do agree on output limits, if OPEC members can’t freeze, a world of non-OPEC members certainly have no reason to. The credit bubble of 2005-15 enabled so much over-investment in this space. Sunk costs now in, everyone that can pump has reason to continue.

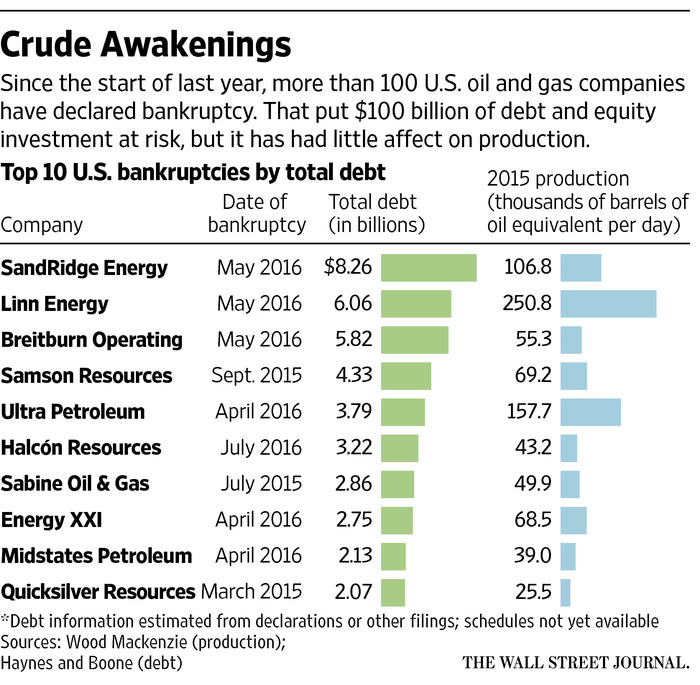

The other gusher taking many oil bulls by surprise is coming from ‘zombie’ energy suppliers (coal, oil and gas) that were driven into bankruptcy over the past year and yet are continuing to produce full-out nonetheless. The Wall Street Journal explains in Bankruptcy bust: How zombie companies are killing the oil rally:

Energy investors have long hoped that falling prices would solve themselves by driving producers into bankruptcy and stanching the flood of excess supply. It turns out that while bankruptcy filings are up, they have barely impacted fossil-fuel markets.

Energy investors have long hoped that falling prices would solve themselves by driving producers into bankruptcy and stanching the flood of excess supply. It turns out that while bankruptcy filings are up, they have barely impacted fossil-fuel markets.

About 70 U.S. oil and gas companies filed for bankruptcy in 2015 and 2016. They now produce the equivalent of about 1 million barrels a day, about the same as before they declared bankruptcy, according to Wood Mackenzie. That represents about 5% of U.S. oil-and-gas output…

This is exactly the way chapter 11 was meant to work. The process is designed to save companies that can be saved, and many energy companies are using it to lighten their heavy debt loads, adapt to lean times and keep producing.

Investors that recklessly funneled cash into this sector over the past few years, are likely to keep losing, while theories of ‘peak oil’ supply continue to disappoint believers.

Peak oil demand growth meanwhile, has turned down with the slowing global economy and emerging secular boom in alternative energies and increased efficiency. Though prices have now retraced into the range of the 2008 cycle lows (brown band on chart below $38 to $47 area), the case for sustained weakness remain stronger today than 2008, given a world much more in debt, with sagging cash flows from stagnant wages and low yields, meeting a boom in smart tech energy solutions that lower fuel expenditures. Lower costs for consumers could not arrive at a better time, as households begin the necessary work of rebuilding their balance sheets with cash savings, and highly levered, obscenely over-valued, long duration assets come back down to earth.