Behind the increasing stress and mismanagement of our natural world, financial mismanagement is the next most pressing issue of our times. A new C.D. Howe report urges the need to address Canada’s government pension deficits with an extension of the age before eligibility. But that is just the tip of the iceberg on the reforms needed in this area.

A new report from the C.D. Howe Institute is arguing demographic challenges necessitate slowly raising the age of eligibility for old-age benefits. In the report, released Tuesday, the think tank’s Robert Brown and Shantel Aris write that the increasing proportion of senior citizens relative to the overall workforce means Canada will have to act.

Here is a direct video link.

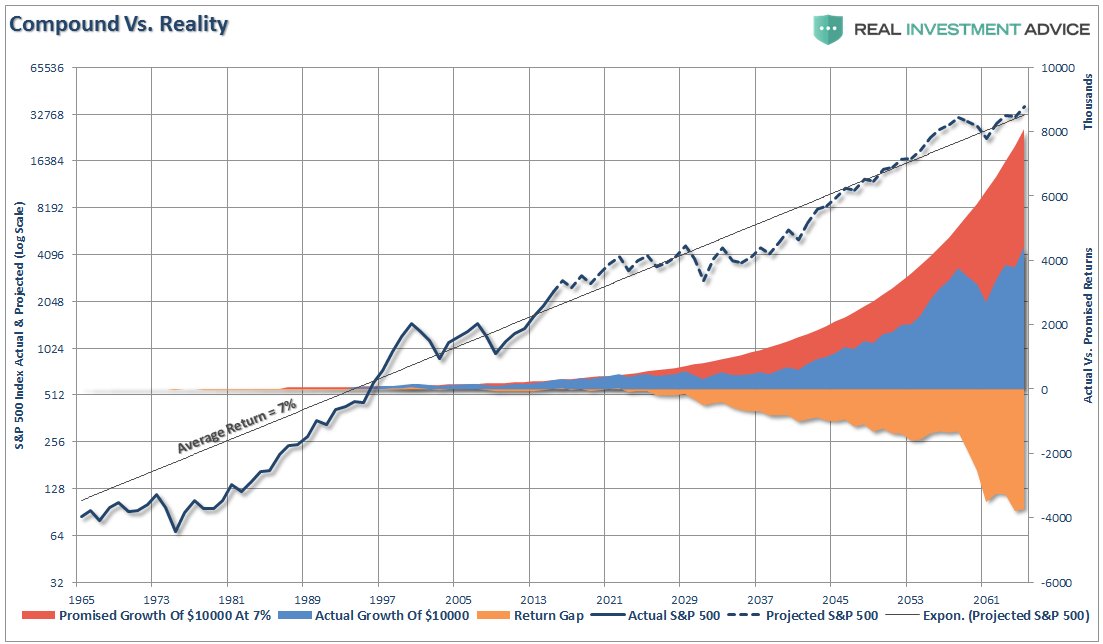

The below chart courtesy of Lance Roberts offers context for this discussion. This shows the ominous gap between the ‘official’ 7% average return target (black line) being used by US pension funds today (similar to most other countries as well as the majority of individual retirement plans that continue to target returns of 7%+) and the actual returns generated (in blue) since the current secular bear in financial markets began in 2000. We can see that actual returns have dramatically undershot targets since the 2008 financial crisis. And that is notwithstanding, trillions in government-backed capital reflating financial assets back to record valuation levels in record time.

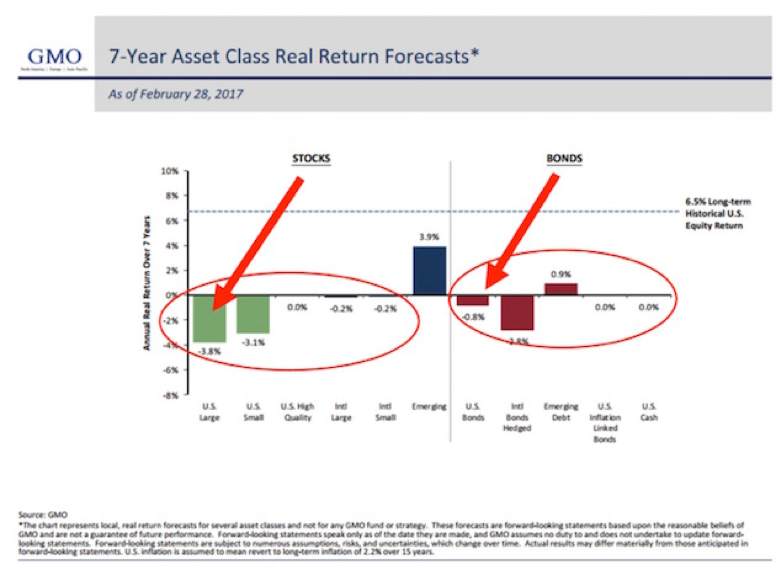

But worse, now that we are already back at nose-bleed highs for financial assets, going forward the return prospects are even lower. In fact history attests that starting from 10-year-average equity PE’s above 20 for stocks, the average annual total return over the next 20 years has been less than 3%. Over the next 7 years, real returns are likely to be negative as shown here in GMO’s 7-year asset class real return forecasts. Imagine what these results will do to pension and savings deficits which are already many trillions today, just in North America. At the same time, the trend of herding into passive indexes and ETFs at present price levels, will not help, but rather only compound the downside from here. This is no time to be passively holding on to overvalued assets and hoping for miracles.

The mess that central banks and 20 years of destructive financial ‘engineering’ has wrought, cannot be hoped and dreamed away. The best chance anyone has in this environment is to not mindlessly take the bait and hold unattractively priced assets, but rather to focus instead on reducing leverage, while building principle and liquidity in order to purchase higher yielding assets in the next bear market. That takes patience and counter-cyclical thinking to be sure, but the alternatives of accepting untenable capital risks for insufficient yields, and indefinite financial frustration and hardship, are much more unappealing.