Auto makers are releasing April sales numbers today and so far, all are reporting a fourth monthly decline, sending their share prices lower. See Every major carmaker whiffs on sales.

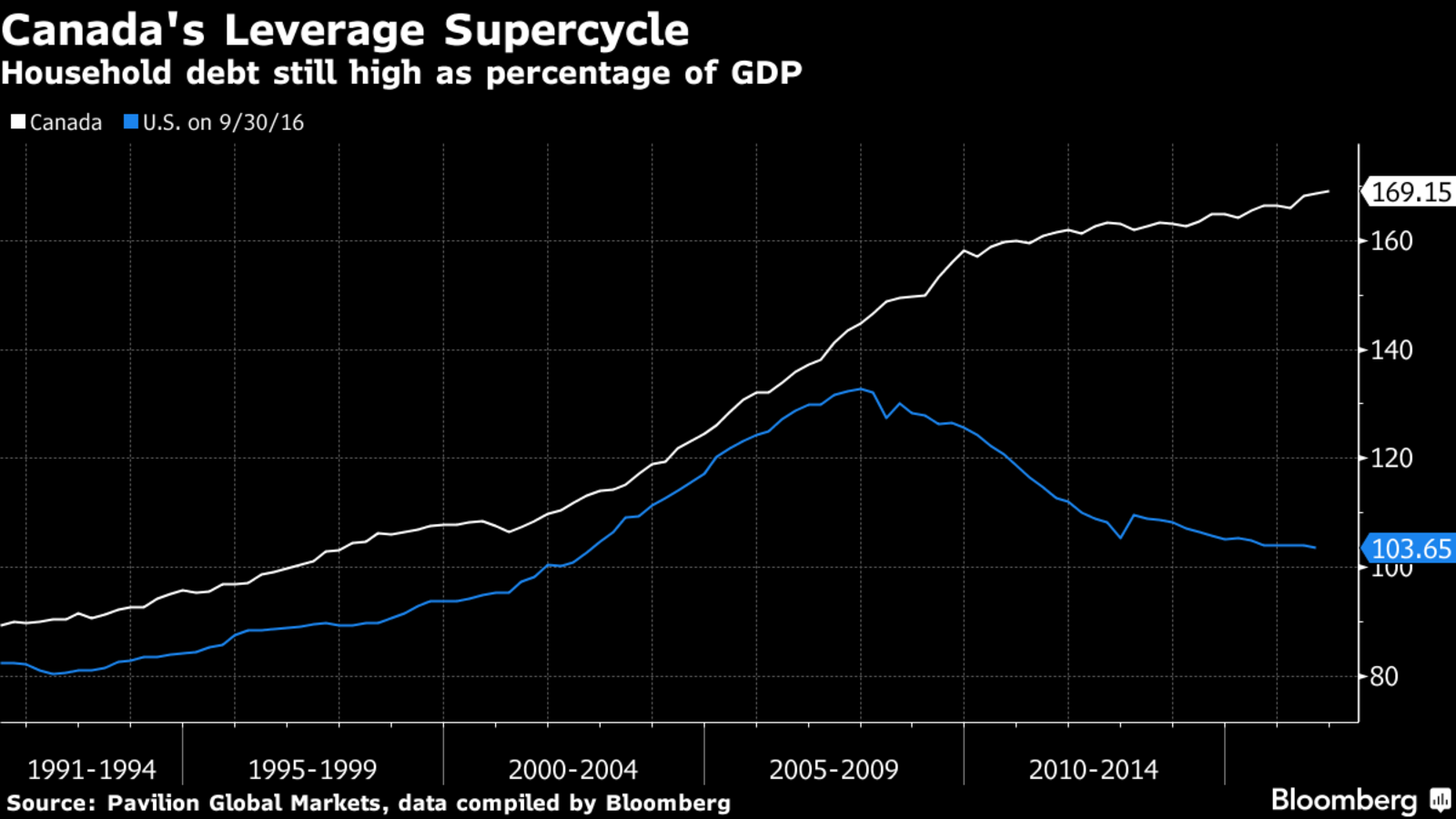

After seven straight years of prodding purchases with increasingly lax lending and uber-generous incentives, disappointment and mean reversion are due. No expansion can last forever, especially one this inherently self-destructive. Canada for one, has never had higher household leverage as shown here since 1990.

Weak auto sales weighed down consumer spending and hurt GDP growth in the first quarter. A year over year decline in 2017, would mark the first since the last recession.

At the same time, the other debt-enabled piston of the consumer-led economy–real estate and related services–is looking more precarious as mortgage magicians meltdown. This chart shows the spread from industry leader Home Capital to the shares of the other non-bank lenders who helped to fund Canada’s consumer debt bubble the past 8 years.

So far the broader Canadian financial sector index (XFN) is only down some 2% since March 1, 2017. But we should make no mistake, bank lenders are also heavily exposed to both household credit and the commercial realty sector.

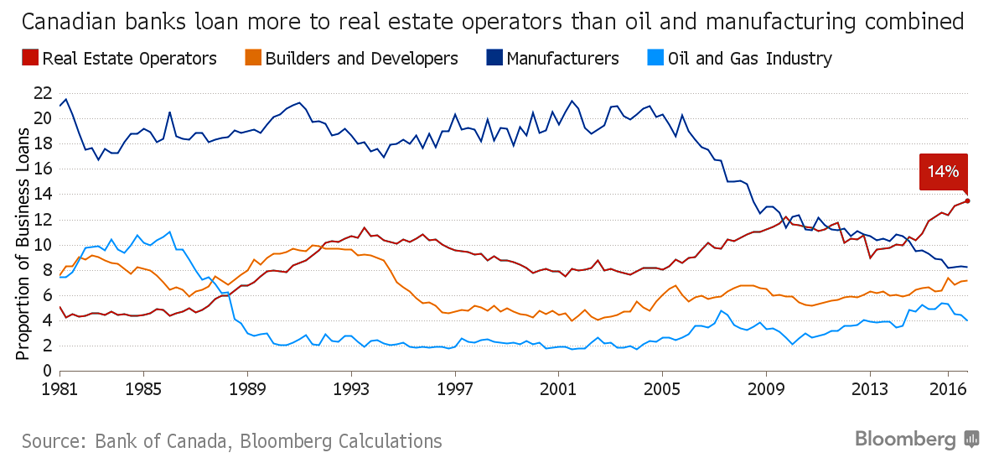

As shown below, realty operators are now a full 14% of the business loans held by Canadian banks–more than oil and manufacturing loans combined. Note that real estate operator loans have led since the oil and manufacturing sectors turned down in 2014.

If the concerns here were contained to just a few borrowers at the margin, that would be easier to overlook. But debt burdens and shrinking revenues are the rule today, not the exception. And knock-off effects connect from the economy through the stock market, which in Canada is about 70% concentrated in just energy and financial shares.

This means that all of the mutual funds, ETFs and asset allocators who are all set up to track the broader index, are also over-exposed to the financial and energy sectors, as both move through a secular consolidation likely to persist for several years.

Tracking markets up is great, it’s tracking them back down that sets holders back years in wasted time and money. And yet, that’s precisely what most advisors, managers and products, are designed to do.