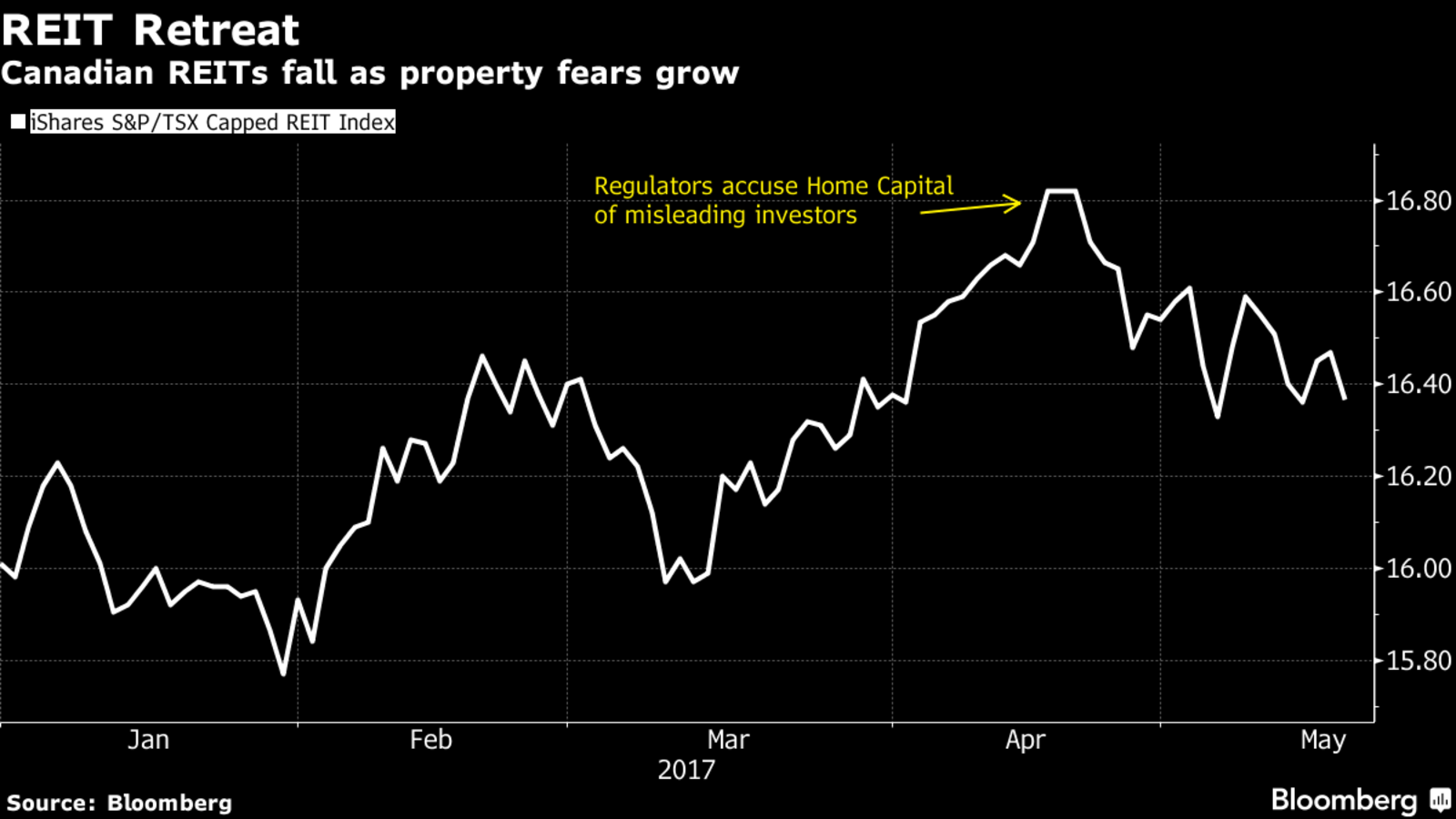

On an ex-dividend basis, the Canadian Real Estate Investment Trust Index (XRE) is today some 9% lower than its prior cycle peaks in both March 2007 and April 2013, and has fallen 3% since the Home Capital meltdown intensified last month.

But if past cycles are prologue, the price-indiscriminate capital that flooded into this sector, desperate for yield the past 4 years, faces much further downside ahead. The problems here go way beyond Home Capital, to a sector that has been grossly over-built, over-bought and over-valued.

The REIT index lost 62% of its value between March 2007 and 2009. Eight years of excessively rising debt and property prices since, have set the sector up for another cycle of deep disappointment. After mean reversion, buyers will find yields about double current levels with a fraction of the current capital risk. In the meantime though, downside risks are due. See: Hit bottom on Home Capital?:

Problems at Canada’s REITs go beyond Home Capital’s woes. A slump in oil prices has hurt demand for property in Alberta, the country’s big cities are seeing rents fall far behind price gains, which dents revenue, and online shopping has shrunk traffic at malls. Finally, in times of broad market stress, REITS behave more like stocks rather than safer bonds, according to Pavilion Global Markets Ltd.

“We find the risk-reward in Canadian REITs to be quite poor in the current environment,” Alex Bellefleur, an analyst at Montreal-based Pavilion, wrote in a strategy note Wednesday. “In the context of Canada’s property bubble, we would stay away from this asset class.”