The mainstream response to falling interest rates over the past decade has been to increase stock weightings in the hopes that capital gains and dividends will support more income than guaranteed deposits can provide. But at the most extreme security valuation levels in history this approach is designed to be financially devastating, especially to those who are at or within 10-12 years of retirement.

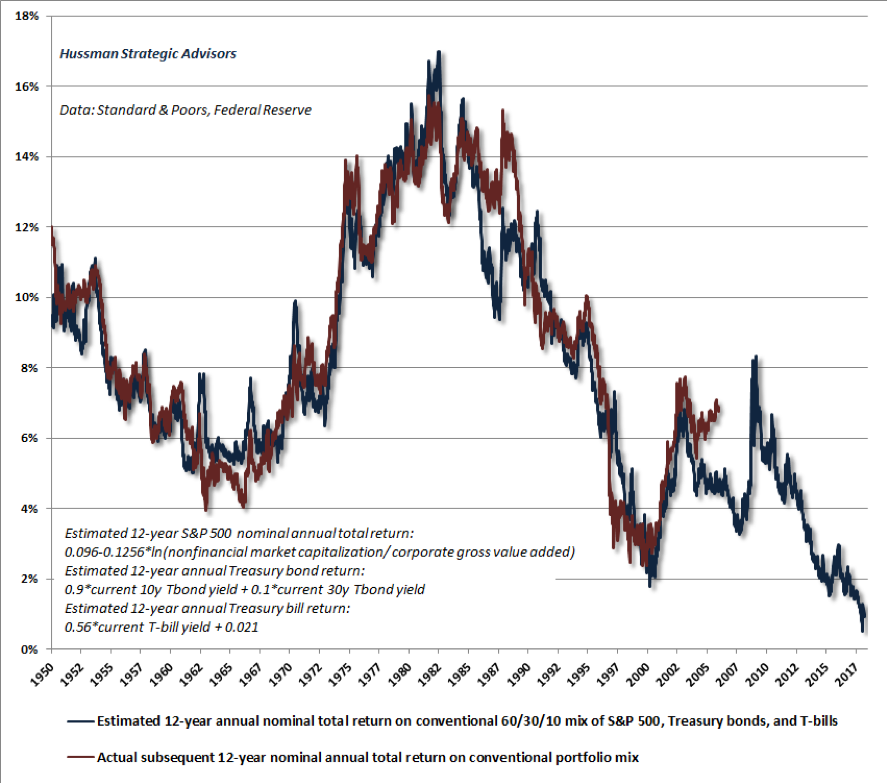

As patiently explained and factually demonstrated by John Hussman this month in The Arithmetic of Risk a conventional portfolio of passive assets (60% stocks, 30% bonds, and 10% cash) has never been more full of risk and bereft of return prospects, than at any time in history. Not in 1929, not in 2000, not ever before.

As shown in his chart below, from current levels nominal expected returns for a 60/40 portfolio over the next 12 years are less than .5% a year (black line)–before any fees or inflation.

Portfolios holding more than 60% stocks today, face even lower return prospects–fully negative over the same time period.

For those trying to withdraw annual income targets while their savings are earning zero and negative returns, the capital evaporation rate is likely to be highly distressing.

The only pragmatic, rational approach in today’s high risk circumstances, is to steer clear of return-free risk now so that we are ready and able to buy investment assets worth owning again once prices have come back down to the higher yielding, lower risk range.

Facing facts and adjusting financial plans accordingly are a necessary part of our financial sustainability today and for the future.