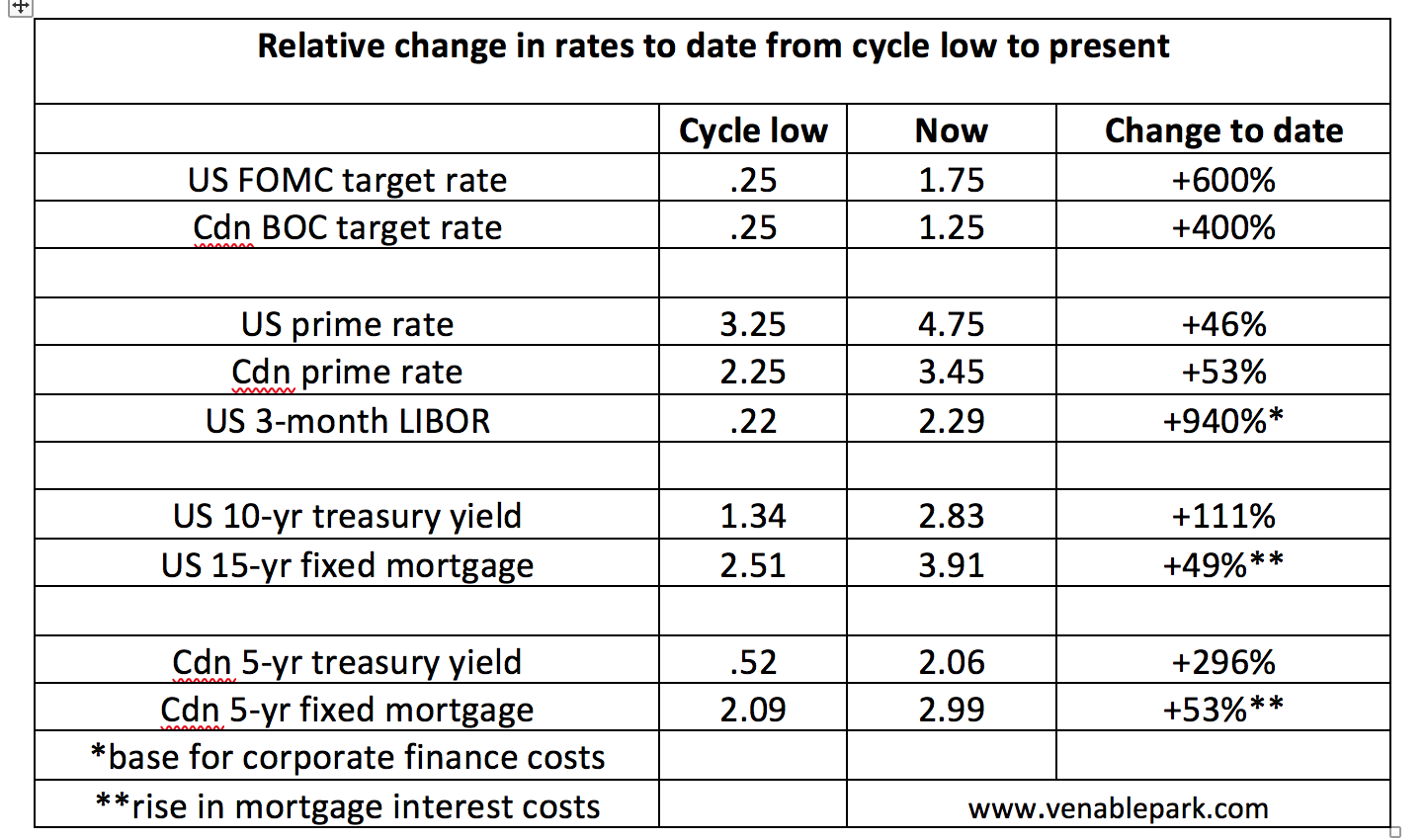

While interest rates have risen over the past couple of years, it’s true that they are still well below the mean of the past 30 years. More importantly however, the net change in key borrowing rates from this cycle’s lows to present has already been intense.  This table summarizes the net change to date for key reference rates in Canada and the US. We note that a lesser 425% tightening of the Fed funds rates from 1% in June 2003 to 5.25% by June 2006, was enough to trigger the ‘great’ recession starting in December 2007. And households and businesses domestically and globally are much more levered/indebted today than they were in 2006.

This table summarizes the net change to date for key reference rates in Canada and the US. We note that a lesser 425% tightening of the Fed funds rates from 1% in June 2003 to 5.25% by June 2006, was enough to trigger the ‘great’ recession starting in December 2007. And households and businesses domestically and globally are much more levered/indebted today than they were in 2006.

Cash flows are feeling the crimp of increased finance costs, even as brave central bankers say they have much more tightening to do. Somehow we doubt their nerve will hold as spending continues to drop and credit strains and defaults build in this late, great credit cycle Frankenstein that they have helped create.

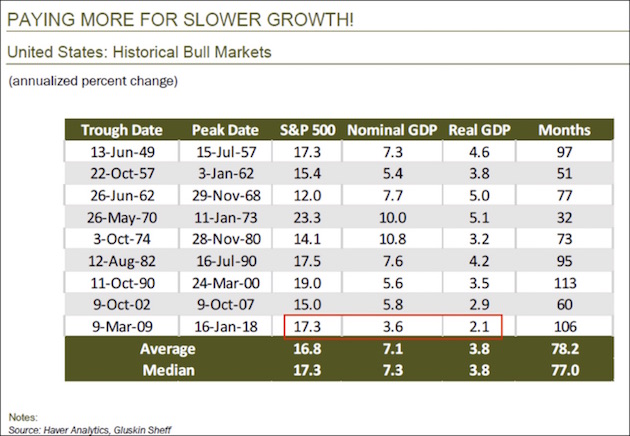

This next table, courtesy of economist David Rosenberg, summarizes how late the present stock market cycle has run compared wit h the other expansion periods over the past 69 years. At 106 months to January 2018, only the October 1990 to March 2000 run was 7 months longer when it ended in a nearly 3-year -50%+ bloodbath for stock holders from March 2000 through February 2003. The tech index of course, dropped by 78%, and many individual shares went to zero.

h the other expansion periods over the past 69 years. At 106 months to January 2018, only the October 1990 to March 2000 run was 7 months longer when it ended in a nearly 3-year -50%+ bloodbath for stock holders from March 2000 through February 2003. The tech index of course, dropped by 78%, and many individual shares went to zero.

The 1990-2000 expansion began from much lower stock valuation multiples than today (the 17-year secular valuation low was in 1982), and this cycle stock buyers have been paying up for much lower growth rates. As shown above, the nominal annual growth rate (GDP) of the US economy at 5.6% during the 1990-2000 expansion was 55% higher than the 3.6% rate averaged since 2009. The recent cycle stands out for having the weakest growth rates on record–about half the historic average.

Corporate issuers and underwriters have made off like bandits during this manic cycle of indiscriminate buyers-run-wild. Soon, holders will realize that the price wasn’t right and they are left with losses to show for it.

“What were we thinking?” people will ask. The answer of course: most weren’t thinking, they were just hoping they could gamble, win, keep playing and somehow keep the proceeds without ever cashing out. Suffice to say, the odds aren’t favorable.