The Atlanta Fed is out today with its latest mark down in the US GDP growth estimate for Q1 2018:

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2018 is 1.9 percent on April 16, down from 2.0 percent on April 10. The nowcast for first-quarter real personal consumption expenditures growth declined from 1.1 percent to 0.9 percent after this morning’s retail sales release from the U.S. Census Bureau.

Here is their chart.

Economic growth is slowing, not just in the US, but worldwide. Despite China’s officially proclaimed 6.8% growth rate in the first quarter today, Capital Economics estimates that it was closer to 4.8%, down from around 6% six months ago.

As explained in the latest Q1 2018 Hoisington Quarterly Review, unprecedented debt abuse over the past 8 years is now compounding an economic slowdown globally, while rendering the economy increasingly immune to the efficacy of monetary stimulants in truncating the coming recession. Here’s why:

The fact that there is such a long lag between policy change and economic impact is critical in analyzing the circumstances today. For instance, suppose the Fed is able to identify the next recession on day one. Also, suppose that on the first day of the recession the Fed drops the federal funds rate to zero. Due to the economy’s extreme over-indebtedness, along with long monetary policy lags, a minimum of one and half years could elapse before even a slight economic recovery is experienced. But, recovering from the next recession, the lag could be much longer since interest rates are so close to the zero bound and indebtedness continues to rise to record levels. Both will interfere with the potency of the liquidity effect. Thus, despite a rapid Fed response, a long recession could ensue.

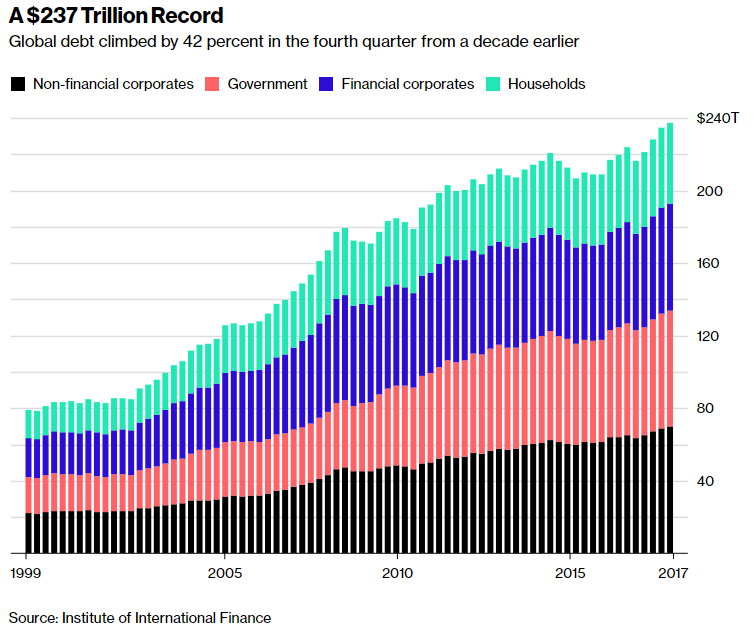

Where savings is present consumption denied, debt is future consumption denied. And here is an updated portrait of the debt now weighing on the world’s future consumption.