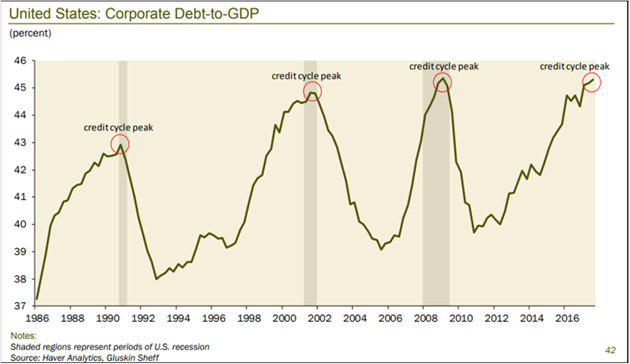

As shown here, corporate debt as a percentage of GDP has reached historic cycle extremes once more, similar to levels that preceded the last 3 recessions (olive bars). As energy prices and interest rates have risen the past 2 years, free cash flow is naturally eroding.

Meanwhile covenant-light bonds–those lacking in usual capital protections for investors– have been more than 80% of those issued over the past 5 years. As defaults rise, losses are coming to yield-desperate buyers who have been acting like suicidal speculators.

It’s not just ‘junk’ debt but also investment grade corporate bonds that are vulnerable. As shown in this chart of the investment grade corporate bond index (LQD) since 2003, high leverage and depleted cash levels cause all types of corporate bonds to be sold along with equities at the end of each credit cycle. Attractive investment opportunity comes for those who buy near cycle bottoms when income yields will be 2 and 3 x present levels, with a fraction of the capital risk (because valuation multiples are much lower). Not there today, but we can see good things coming to those who wait.

Follow

____________________________

Cory’s Chart Corner

Load More