The Wall Street Journal runs this week with a detailed expose on the crisis of insufficient savings and income among Baby Boomers. This problem will be an enduring international preoccupation from here, as older folks battle young folks and other critical social needs for increasingly scarce resources. See: A generation of Americans is entering old age the least prepared in decades. Low incomes, paltry savings, high debt burdens, failed insurance—the U.S. is upending decades of progress in securing life’s final chapter.

This is what comes of poor planning, and of allowing financial sales wolves to shepherd masses of herd-following sheep–sheep who too easily abdicate personal discipline around their money habits and decisions. Despite incessant tinkering at the regulatory edges no meaningful reforms, in our widely destructive and dominating financial sector, have been made thus far. The farce of it all, is a sick joke. For an important update see: For big banks, breaking the rules is a trade secret.

Among the relentless barrage of fantastical marketing, it is crucial to comprehend that equities, and all the funds and products that are full of them, are routinely toxic investments when they are bought/held at rich valuations.

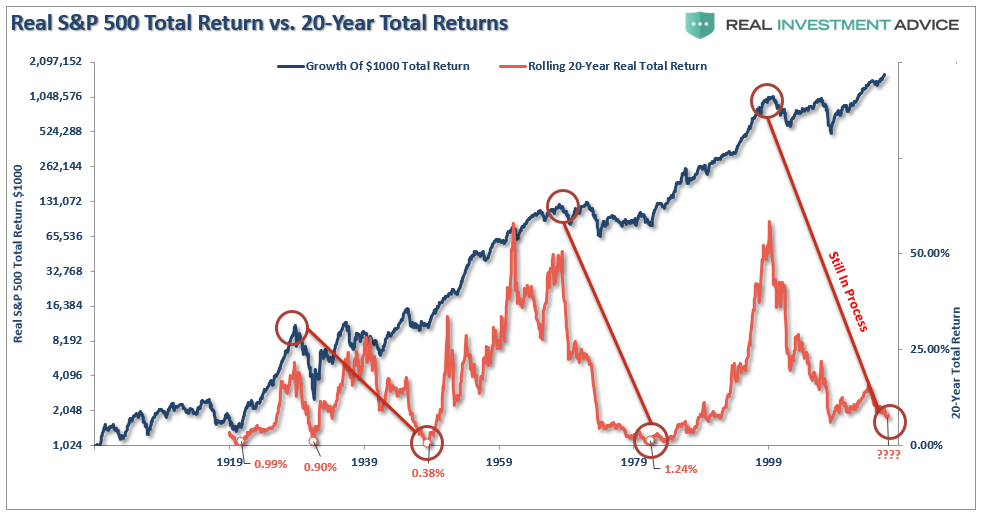

Indeed as shown in this excellent chart from Lance Roberts below, the total real return for equities (even impossibly assuming no fees and that all dividends were reinvested) have had four 20-year periods since 1900 of near zero returns (see periods noted in red below). The fifth period, that began from all time obscene valuations in 1999, is still ongoing and poised to fulfill its zero return destiny in the next bear market, now overdue. Whether one understands, acknowledges or ignores–these are the facts we are all navigating: pensions, governments, businesses and individuals. There is no alternative reality planet to choose.

There are smart, self-disciplined, pragmatic steps that individuals can take to prosper through these conditions. These are all focused on fiscal discipline: on controlling and reducing spending, minimizing debt and over-valued investment assets, building and protecting savings, and preserving liquidity with a plan to buy what others will be liquidating. These steps are all the opposite of what the mainstream and masses are doing.

As Lance concludes, in The Myths of stocks for the Long Run-Part IV:

The “power of compounding” ONLY WORKS when you do not lose money…after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe…

There is no reason to “benchmark” your portfolio to some random index. The index is a mythical creature, like the Unicorn, and chasing it takes your focus off of what is most important – your money and your specific goals. Investing is not a competition and, as history shows, there are horrid consequences for treating it as such. This is why incorporating some method of managing the inherent risk of investing over the full-market cycle. I would question those who tell you not to do so as they are likely acting from a position of incompetence or self-interest. In the long run, you probably will not beat the index, but you are likely to achieve your financial goals which is why you invested to start with.