David Rosenberg can be helpful because he is one of the few economists who looks for negative trends in the data rather than just blue skies and sunshine. His comments on the implications of a ‘Powell pause’ in this clip are lucid. Here is a direct video link.

This ‘elephant in the room’ could send stocks into a tailspin, Wall Street bear David Rosenberg warns from CNBC.

Incongruent, however, is that while warning of late cycle recession risks and a housing downturn in Canada, Rosenberg was suggesting people move capital into Canadian stocks this month. True, Canadian equities are trading at cheaper valuations than US stocks today, but they are still near cycle highs, and stocks are stocks–they pretty much all tank in recessions and bear markets. ‘Defensive’ they are not.

Even in 2001, when Canada did not officially follow the US into recession, the Canadian stock market still lost half of its value along with US markets. A similar magnitude of losses happened in 2008, even though Canadian realty was then much less levered and more stable than US housing. Of course, that was then, today Canada is worse off.

Rosenberg’s firm Gluskin Sheff, a Canadian-based asset manager, may expect their chief economist to talk in support of their Canadian equity holdings. This would be unfortunate because Gluskin hired Rosenberg to come and help rehabilitate their risk-management image after their portfolio losses in the 2008 cycle. Given that Gluskin’s own share price (GS.TO) has fallen 50% since 2014 and 35% since just July, it seems the firm is under pressure once more. Unfortunately, remaining long and adding to Canadian equity positions, heading into a recession, is unlikely to help them or their clients. But since most asset management firms are paid the highest fees from equity allocations, this tends to be a constant mantra.

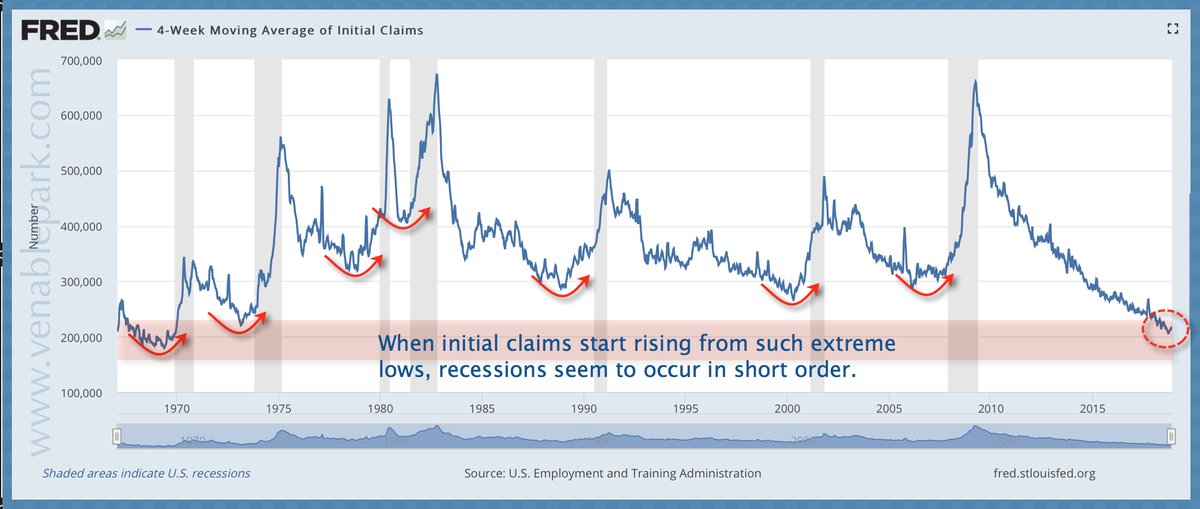

Further on cycle point this morning, US initial claims for jobless benefits moved higher. As shown in my partner Cory Venable’s chart below since 1965, when initial claims start rising from extreme lows, recessions (grey bars) have historically been imminent.