It is typical of dramatic price appreciation cycles, for people to believe that those with the means to buy expensive assets are somehow impervious to credit cycles, and will continue to buy and not sell, regardless of stresses that may impact the masses.

Until recently, for example, it was common for people to say that Vancouver and Toronto realty prices were unlikely to decline because the cities were world class and high-end buyers don’t care about mundane things like down payment requirements, interest rates and taxes. History attests that this just ain’t so.

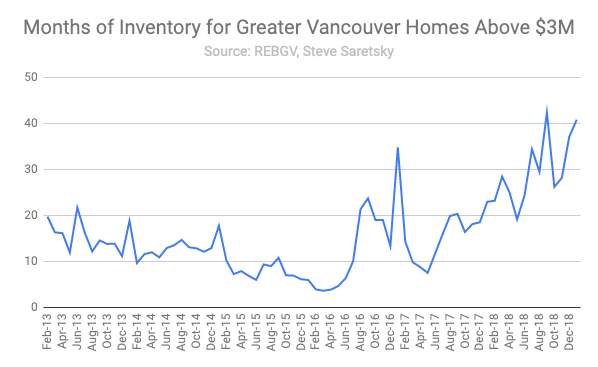

To the contrary, expensive properties are generally the most illiquid and vulnerable to a correction as buyers retreat and owners look to raise cash and downsize costs. Case in point, see: Vancouver’s luxury home market accumulating a logjam of inventory:

As is typical in all housing corrections, luxury properties are the first on the chopping block while also suffering the steepest of price discounts. This is ultimately the result of a much smaller buyer pool that, when it shrinks, creates liquidity constraints. As the housing cycle turns, and liquidity dries up the luxury market becomes extremely prone to volatility and wild price gyrations. As a result, bank credit also seizes up, further hampering liquidity when it is most needed.

It appears this phenomenon is playing out in the Greater Vancouver housing market. With global growth slowing, and Chinese capital controls becoming even more severe, luxury home sales have ground to a halt.

As shown below, at the present rate of sales in the $3m+ price category, the Vancouver market now has 41 months of inventory today compared with four months worth at the peak of the buying frenzy in early 2016.

As always, the cure to high prices ends up being high prices, and it’s very likely that this much overdue correction phase is only just begun.

As always, the cure to high prices ends up being high prices, and it’s very likely that this much overdue correction phase is only just begun.