The Canadian dollar has gained 4.3% against the U.S. dollar since the start of 2019 for reasons that include, a softer greenback on expectations of US rate cuts, some rebound in commodity prices as the U$ has weakened, stronger Canadian gross domestic product for April (backward-looking) and a trade surplus in May (backward-looking) for the first time in ten months. See: Loonie soars as the Canadian economy firms while the US wobbles.

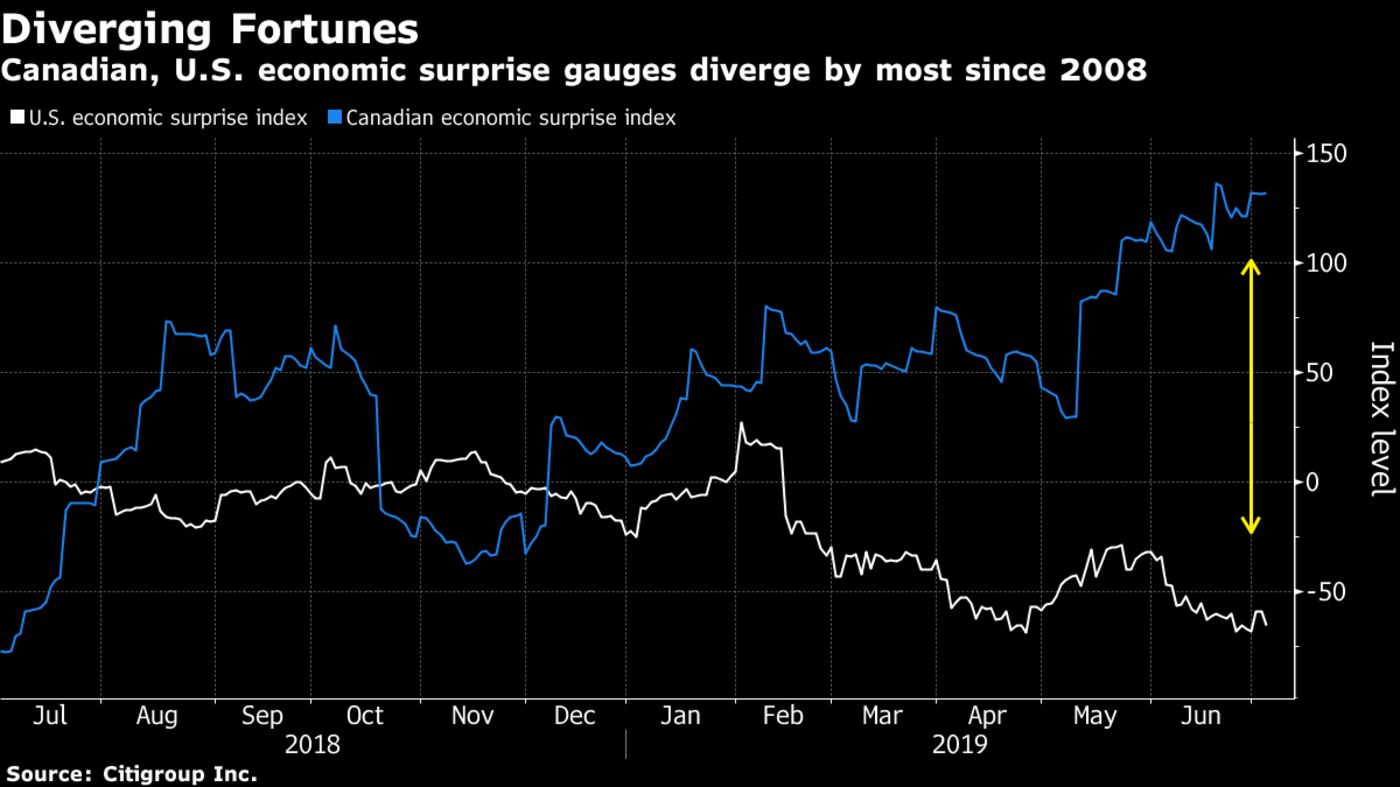

Indeed, as shown below, the divergence between Canadian and US economic surprise indicators has widened year to date by the most since the onset of the 2008 recession.

In reality, the Canadian economy and Loonie do not hold up for long once its largest trading partner enters a persistent downturn. Thus when the US Fed responds to falling demand and tanking stocks with rate cuts, the Bank of Canada is never far behind. Even in 2001, when Canada did not follow the US into an official recession, the Bank of Canada slashed its policy rates to weaken the loonie and boost exports, but the Canadian stock market–including Canadian bank shares–still dropped by 50%.

In reality, the Canadian economy and Loonie do not hold up for long once its largest trading partner enters a persistent downturn. Thus when the US Fed responds to falling demand and tanking stocks with rate cuts, the Bank of Canada is never far behind. Even in 2001, when Canada did not follow the US into an official recession, the Bank of Canada slashed its policy rates to weaken the loonie and boost exports, but the Canadian stock market–including Canadian bank shares–still dropped by 50%.

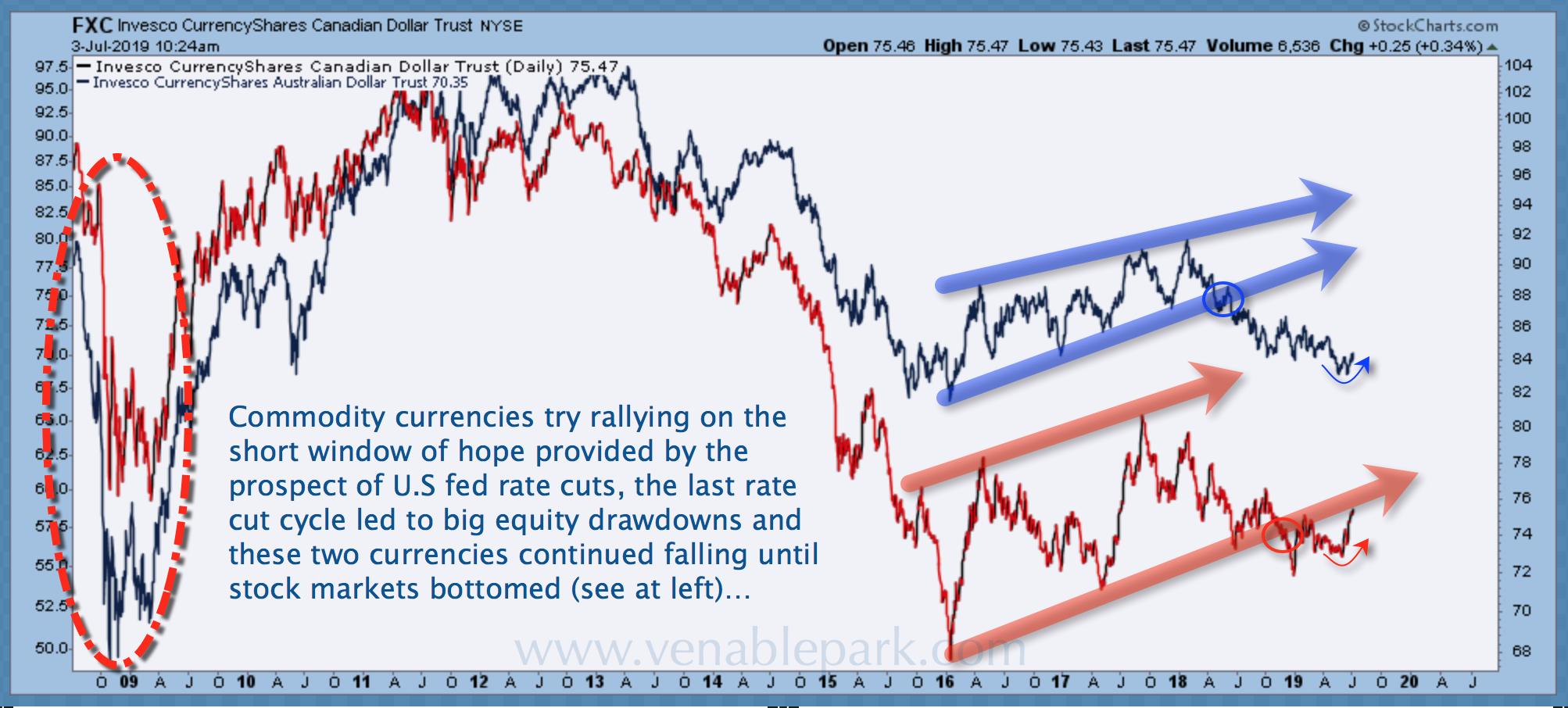

As shown in the chart below from my partner Cory Venable, in late 2007 similar patterns emerged as commodity currencies, the Australian and Canadian dollar, initially held up as the US Fed turned dovish, and then tanked with stocks and global demand as the BOA and BOC deployed every monetary tool they had, for years thereafter. They wish they had the same policy room today, alas they do not.

At the same time, Canadian and Australian households are world record holders for indebtedness–far worse than at the outset of either of the last two US recessions.

We can hope for unprecedented decoupling from the US dowturn this time, but the odds aren’t compelling.