We are living through the final scenes of one of the most financially-destructive chapters in human history.

I was an investment analyst in the 2000 dot.com bubble and the 2007 China/commodities/subprime bubble and, yes, they were mad times too. But unprecedented ‘free’ money over the last seven years has managed to magnify the destructive behaviours that ought to have asphyxiated in the last two busts. Like homeowners threatened by raging fires, self-preservation demands that we stay clear of structures destined to collapse, but this takes self-discipline and constant mental effort.

Indiscriminate buyers funnel capital into the market inferno every day, while those insisting on value for capital risked, find a meagre opportunity set at hand.

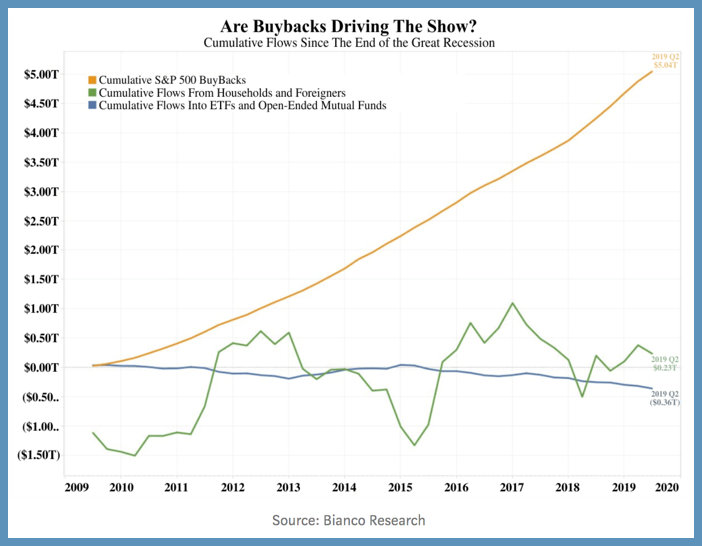

As shown in Jim Bianco’s chart below, large companies have kept the Ponzi afloat to date by using their cash flow and record borrowing to buy their own shares (in orange since 2009), while the relative flows from households and foreigners (in green), ETFs and mutual funds (in blue) have stagnated.

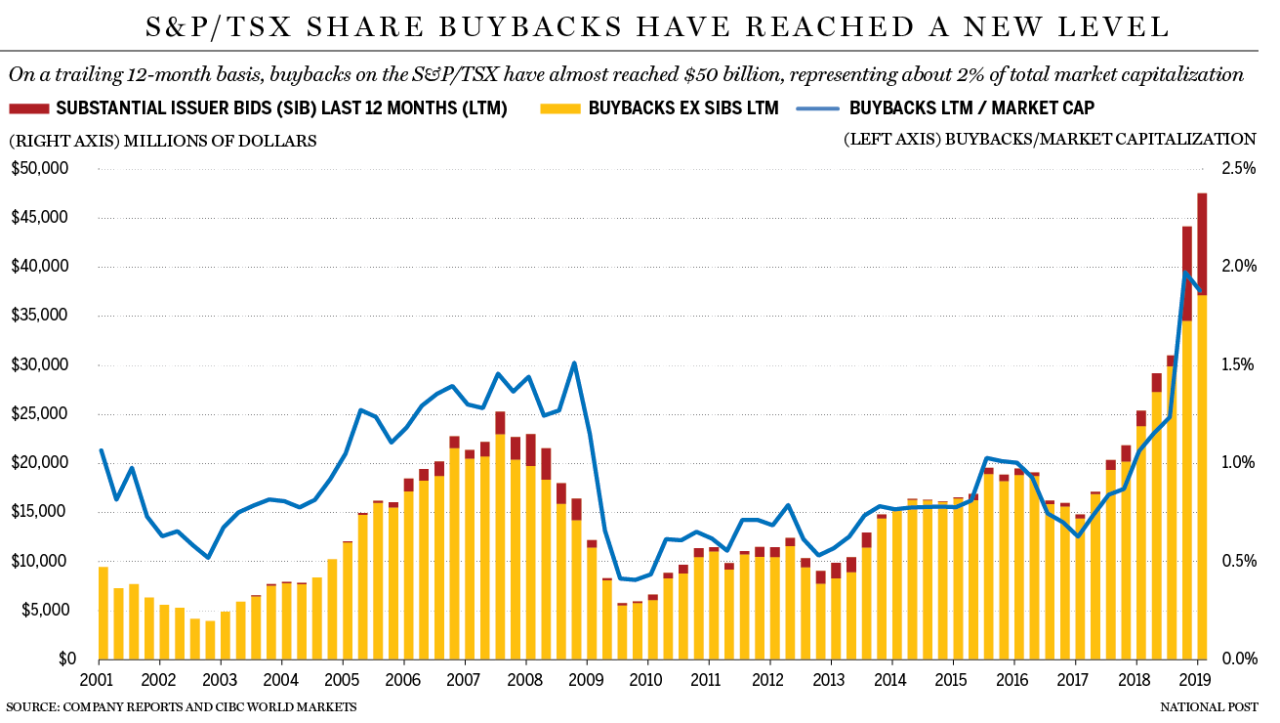

Buybacks of common and preferred shares by the largest TSX 60 Canadian companies are also up, more than doubling from 2015 to 2018 as shown below, led by Royal Bank, TD Bank and Thomson-Reuters Corp. See: ‘The American disease’: Canadian companies pouring cash into stock buybacks as backlash grows abroad.

Buybacks of common and preferred shares by the largest TSX 60 Canadian companies are also up, more than doubling from 2015 to 2018 as shown below, led by Royal Bank, TD Bank and Thomson-Reuters Corp. See: ‘The American disease’: Canadian companies pouring cash into stock buybacks as backlash grows abroad.

In the process, corporate debt has tripled along with a 50% increase in total debt globally to $247 trillion by Q1 2019 (companies, governments and households), and has undermined financial resilience and increased downside risks.

We saw a similar playbook in the 1920s and 30s, and the next reckoning period threatens to be similarly harsh. This video explains the history of buybacks and how they became a destructive force over the last decade, as well as some necessary changes from here.

For a long time, it was off-limits for a corporation to buy back its own stock. Not anymore. Here is a direct video link.