The U.S. stock market has reached 100-year highs versus global equities in terms of relative price and valuations. While other world markets have risen an average of 50 to 60% over the last decade, US stocks have lept 250% in terms of price.

This unusual outperformance has been driven by a handful of tech companies, largely in the past 6 years, as central banks pumped unprecedented liquidity and companies ploughed trillions into buying back their own shares.

The Chief global strategist of Morgan Stanley Investment Management, Ruchir Sharma explained this week that US outperformance is unlikely to continue in the 2020s. U.S. stocks now account for 56% of the world’s market value but only 25% of global economic output. Sharma warns that this “huge disconnect” is unlikely to continue.

Here is a direct video link.

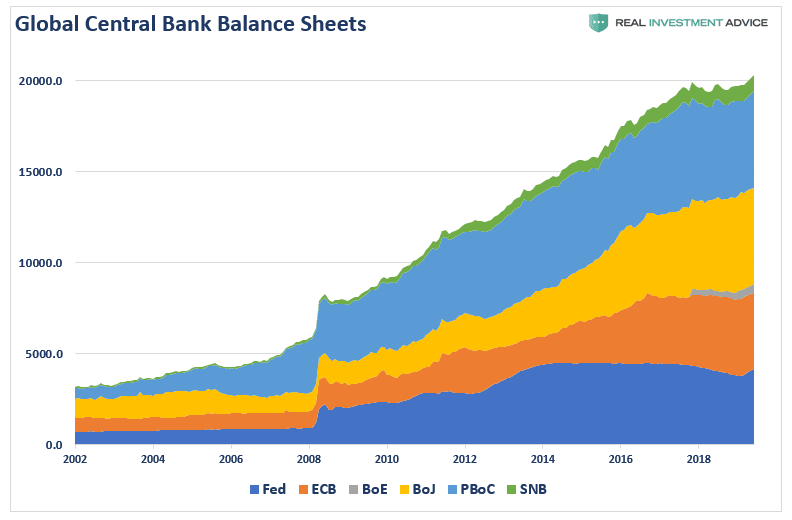

The chart below shows the Everest of central bank-backed funds that inflated asset markets over the past decade.

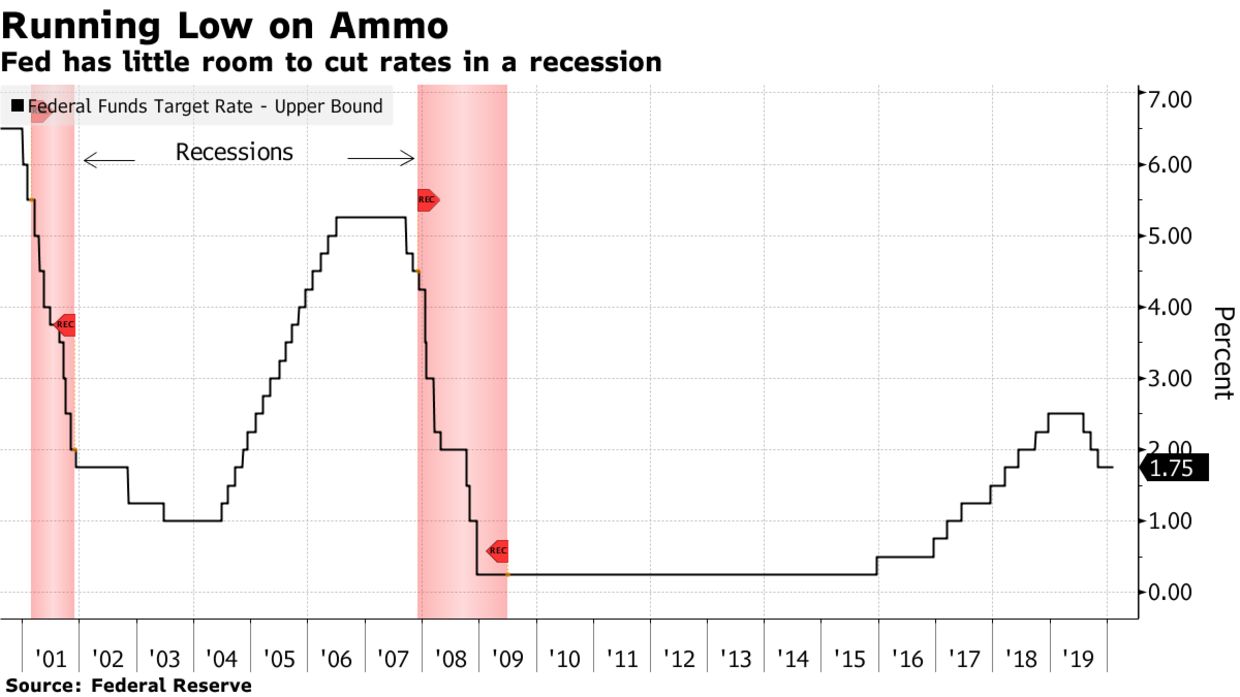

Yesterday, US Fed Chair Powell warned that the Fed is meeting the global slowdown now at hand with little ammo to help offset it. This chart courtesy of Bloomberg shows the more than 5% rate-cutting room in the Fed rate coming into the last two recessions (pink bars) versus today at 1.75%.

Yesterday, US Fed Chair Powell warned that the Fed is meeting the global slowdown now at hand with little ammo to help offset it. This chart courtesy of Bloomberg shows the more than 5% rate-cutting room in the Fed rate coming into the last two recessions (pink bars) versus today at 1.75%.

Eye-watering valuations in US equity markets have prompted value-desperate capital to migrate to other global equity markets in search of better return prospects. But this does not have to mean positive return prospects. Most managers and funds seek to be perpetually allocated to stocks through full cycles up and down. In this approach, success is defined as losing less than others in bear markets.

Non-US equity markets that are less extremely overvalued coming into 2020, may fall less than the US but, we should make no mistake, holders sell in mass as prices tank and panic infects markets globally. The U.S. Fed and corporate security markets have led the world on the way up this cycle, and they will also lead on the way down. Capital losses will not be contained in America.