After bouncing 10% between March 20 and September 1, the Canadian dollar continues its allegiance with risk assets, dropping 1% against the US dollar today and rolling over at the 74.50 resistance range, highlighted in my partner Cory Venable’s chart below since 2007. A restest of the March low in the .67 area (pink band below) is likely as recession and an equity bear market continue into 2021.

With global demand faltering afresh, the Bank of Canada is stuck near zero (.25% on overnight rate) and already buying 4 billion in government bonds weekly (which they dialled back from $5 bn). There is no more monetary cavalry to rescue zombie borrowers and highly levered asset holders.

Oil (WTI -6% today), back under $38 a barrel knows it, with another retest in the $18 to $25 range likely ahead (as we noted in our September month-end client letter).

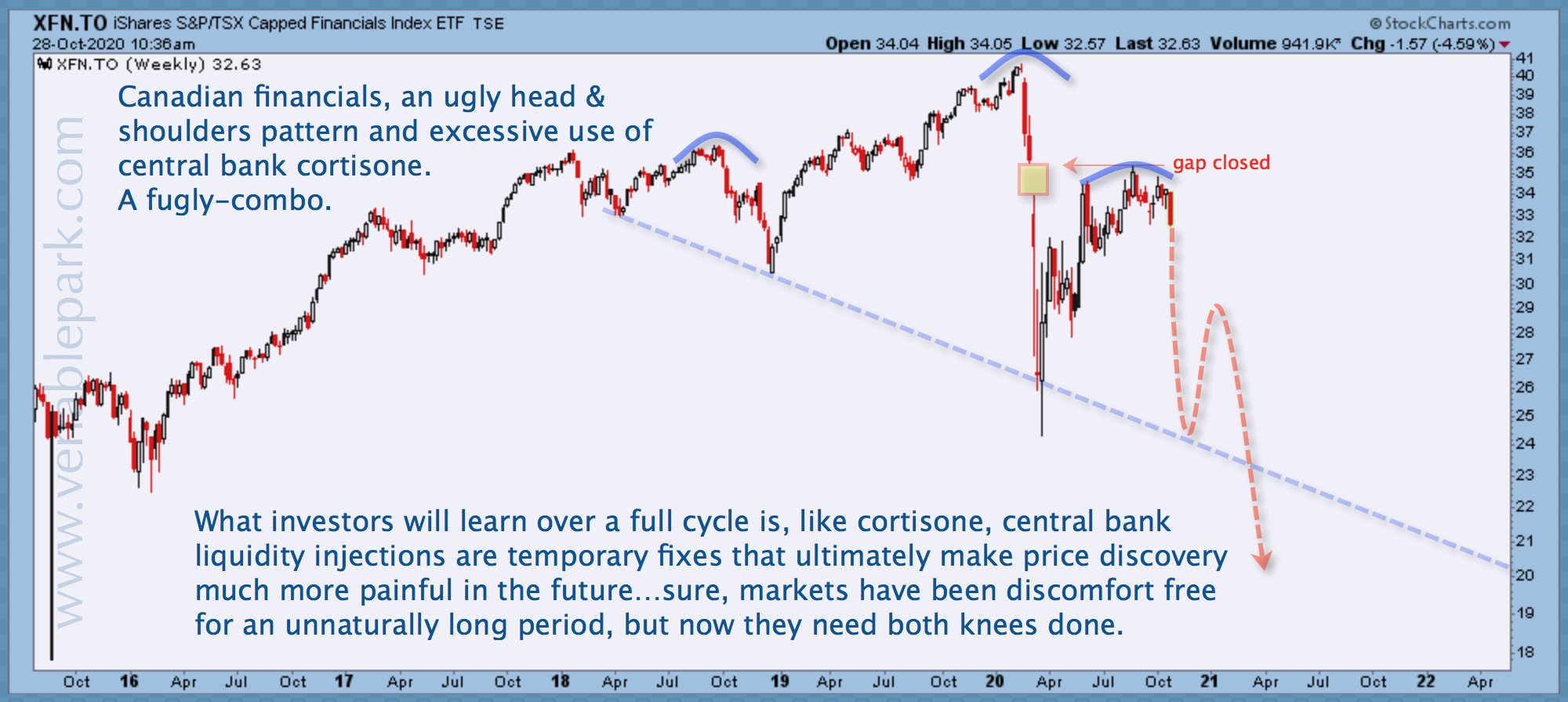

With just five TSX companies in the green today, even index-leader Shopify (-5.8% on the day) can’t catch a bid. The heavy-weight oil and gas sector (now 11.8% of the TSX index) is -55% in 2020, and the widely held Canadian banks are wallowing: -22% since February 20. As shown in Cory’s chart below of the financial index (XFN), a nasty head and shoulders formation beckons Canadian financials (31.6% of the TSX) to give up ill-gotten gains as the fruit of their reckless lending years now rots.

More sustainable business models are needed and, fortunately, they exist.

Lower asset prices are essential in restoring attractive investment opportunities. Waiting for them to materialize can be hard, but not nearly as hard as holding them while they drop.