After a rough couple of weeks, the risk trade is bouncing. While those in the business of selling us risk (in exchange for our cash ‘trash’) advise that investing requires bravery, the truth is that risk management, discipline, and math-based assessments are the best predictors of longer-term financial outcomes. Unfortunately, discipline and realism tend to have less mass appeal.

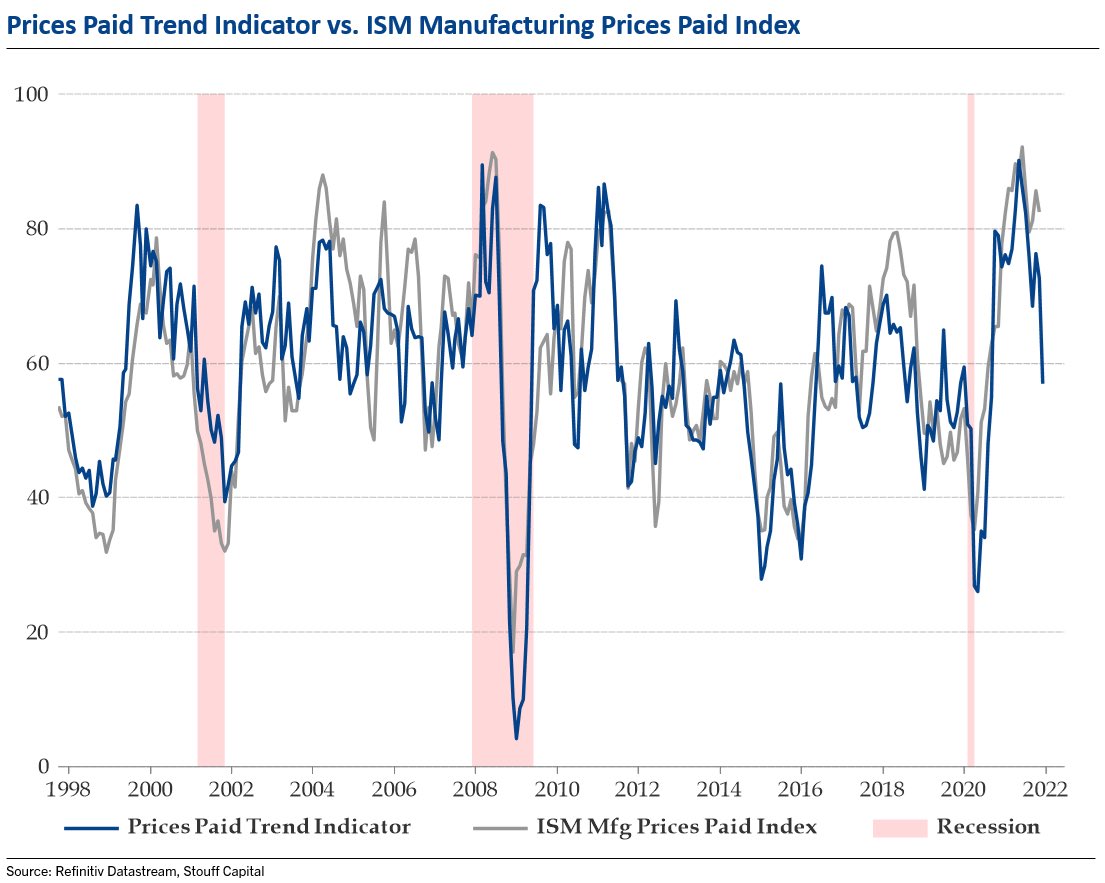

As we look back on 2021, some key trends stand out. First, as shown below, since 1998, despite ongoing inflation hype, the U.S. prices paid trend indicator (blue line) peaked in June 2021 and turned down–this typically leads ISM Manufacturing prices (below in grey) by 2 to 3 months and suggests inflationary pressures will continue to reverse. Treasury yields are in agreement. As shown below from my partner Cory Venable, the U.S. 10-year Treasury yield peaked at the start of April and has made lower highs since. From 1.475% today, the 1% yield area is the next downside test, with capital gains for Treasuries along for the ride.

Treasury yields are in agreement. As shown below from my partner Cory Venable, the U.S. 10-year Treasury yield peaked at the start of April and has made lower highs since. From 1.475% today, the 1% yield area is the next downside test, with capital gains for Treasuries along for the ride.

Commodities are signalling a similar story with the Goldman Sachs Commodity Index (GSCI below) now 11% below its late October peak and back where it was in 2018. On the other end of the commodity teeter-totter, as shown below since 2016, the greenback has also gained against the commodity-centric loonie since last spring, with 1.30 being the next upside test.

On the other end of the commodity teeter-totter, as shown below since 2016, the greenback has also gained against the commodity-centric loonie since last spring, with 1.30 being the next upside test.

Widely overlooked is that eighty-eight percent of global trade, sixty-one percent of foreign bank reserves, and about 40% of the world’s loans are in U.S. dollars. To make payments, debtors and buyers of goods and commodities must acquire the currency, either through incoming trade flows or by selling other assets and currencies. Less global trade means fewer dollars circulating into the hands of those needing them.

Widely overlooked is that eighty-eight percent of global trade, sixty-one percent of foreign bank reserves, and about 40% of the world’s loans are in U.S. dollars. To make payments, debtors and buyers of goods and commodities must acquire the currency, either through incoming trade flows or by selling other assets and currencies. Less global trade means fewer dollars circulating into the hands of those needing them.

As the U.S. fiscal and monetary impulse retreats sharply from two years of unprecedented spending, global GDP growth is reverting to a 3% annualized pace in the fourth quarter, from 6% last, and lower than the 4% pace before the pandemic.

A world long on the same levered assets and tons of debt but short on cash and cash flow will increasingly need to liquidate what they can—understanding why and positioning ahead of the pack is essential to risk management.