Many believe that home prices will continue to rise year over year on a never-ending stream of able and willing buyers. This has never been true historically. Most people borrow heavily to buy real estate, so prices have always followed credit cycles up and down.

After ending its Q.E. injections to the banking system in October, last month, the Bank of Canada (BOC) blinked and did not increase its overnight lending rate from the emergency lows of March 2020, as widely expected. Central banks are under great pressure to hike as the cost of housing, food and energy have jumped over the past two years. A total of five BOC rate hikes is the consensus forecast for 2022 taking Canada’s base lending rate from .25% now to 1.50% by year-end–a 500% increase over 9 months.

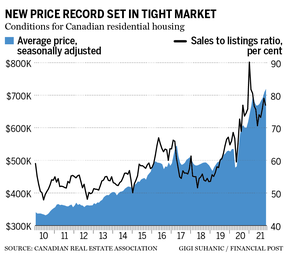

Of course, without the BOC making any hikes, Treasury Bond prices, on which fixed mortgage rates are based, have already sold off enough that fixed mortgage rates in Canada are back to where they were in 2016. The problem is that as shown on the left, home prices have about doubled nationally since then, so affordability is a problem even with 2% mortgage rates. See Average home price in Canada hits all-time high of $720,850.

Any hikes that are made in 2022 will increase carrying costs on business and personal loans, lines of credit, HELOCs, and variable-rate mortgages. Half of the mortgages taken on in Canada last year were variable.

These conditions are full of risk for borrowers, lenders and the overall economy. But with most of the nation’s economic growth dependent on the inflating property sector over the past decade, few are able or willing to acknowledge the property elephant now filling our economic room. And of course, as usual, the commission-engorged realty sector sees only more upside–forecasting a 9.2% increase in average residential sale prices (twice the long-term norm) across Canada in 2022.

Last week, Canada’s federal banking regulator described the housing market as being in the late stages of a “speculative fever,” and warned that prices could plunge by as much as 20% in some markets with negative implications for investors in the properties and securities markets. See Banking watchdog warns housing prices could plunge 20% when ‘speculative fever’ breaks:

Canada’s housing market has been setting records for the better part of a decade, led by Vancouver and Toronto. The frenzy has spread to other cities during the pandemic, as demand for bigger houses, or cheaper ones than can be found in major centres, caused Toronto-like price increases in places such as Ottawa, Montreal, and Moncton, New Brunswick.

Investors took note and jumped on the opportunity to turn a profit. Routledge said a “speculative boom” in housing has added extra heat to the market. Typically, investors account for about 15 per cent of home sales, but currently they are responsible for about 22 per cent of sales, he said.

“Even though that seems like a little bit, it’s quite significant incremental demand into the system,” Routledge said.

However, investors’ interest in the housing market likely is about to decline. “With rates going up, with the general recognition that, ‘Boy, housing is pretty fully valued,’ I’m not sure your expected return in the housing sector … I think a smart investor would think twice and maybe look at other outlets,” he said.

Former CMHC head Evan Siddall issued similar warnings before he was bullied into apologizing and finally stepped down in 2020.

We highly doubt that central banks will follow through with even a third of the tightening presently forecast, before tanking asset markets and financial strain prompt them to pause and seek new stimulative prods for buyers.

Some believe this means home prices can continue to rise because interest rates will remain low indefinitely.

But here’s the thing, even if rates stay low, property increases in line with long-term historical norms of 5% per year would be a problem for highly levered families and investors who are presuming the continuation of abnormal capital gains. Just a few years of flat prices would be a huge negative for these participants too.

Mean reversion back to historical appreciation norms–some combination of double-digit price declines and/or a decade-plus of stagnant prices–would be a catastrophe. And yet, this is the most probable outcome. Preparing for this is responsible and wise.