BUSY WEEK!!! Where to start!?

Let’s start with the most widely held and highly leveraged asset globally, housing.

In the past few months, bond prices have dumped (spiking their yields) to discount for a whopping 3% of central bank rate hike plans over the next year. The carrying cost of fixed-rate loans (which rise with government bond yields) is now doing a lot of demand-quashing work before central banks even do much tightening. It’s no wonder.

As shown courtesy of my trustee in bankruptcy friend Doug Hoyes below, Canada’s lowest average 5-year fixed mortgage rate available in March was 3.38%, compared with 2.63% in March 2020. At the same time, the median detached home price in the Greater Toronto Area rose from $902k to just under $1.3m. The 44% increase in the median home price and 28% higher interest rate drove the median mortgage payment 56% higher in just two years. Spoiler alert, median household incomes have not risen along with housing costs.

Even if the buyer had a 20% down payment and no other debts, the minimum income needed to qualify for a mortgage on the median home last month had risen to $138,820 (43% debt-t0-income ratio) from $89,506 two years earlier.

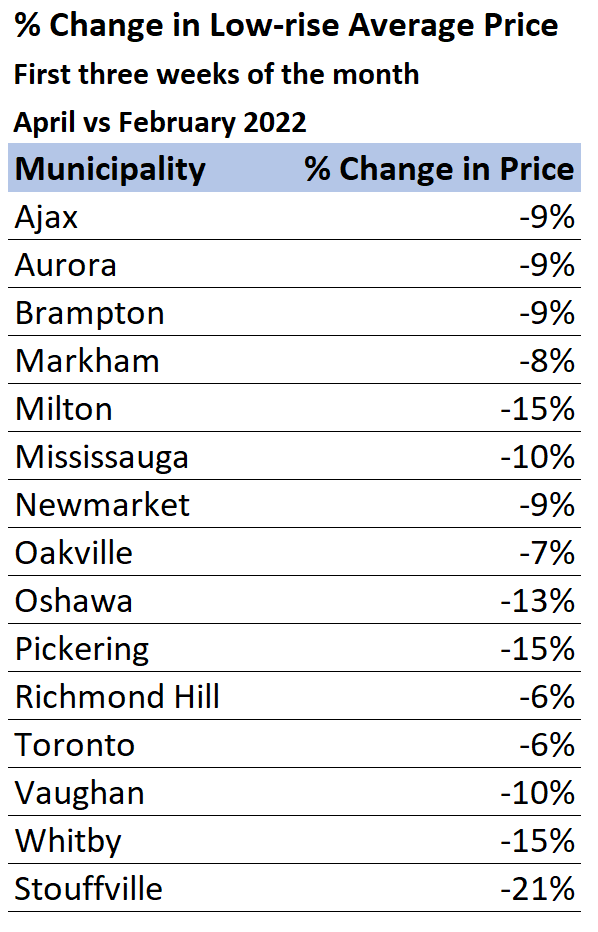

In April, mortgage rates rose further, with the offered 5-year fixed-rate at the big five banks above 4%. Despite many still having lower pre-approved rate offers (from before the latest hikes), the median single-family sale price in the first three weeks of April was significantly lower than in the first three weeks of February (as shown on left, courtesy of realtor John Pasalis.) Math is starting to matter again.

4%. Despite many still having lower pre-approved rate offers (from before the latest hikes), the median single-family sale price in the first three weeks of April was significantly lower than in the first three weeks of February (as shown on left, courtesy of realtor John Pasalis.) Math is starting to matter again.

These changes may seem relatively modest. But only if you are not one of those who bought above the current market price. Imagine the many who purchased to see most of their equity evaporate within the last two months.

Imagine that the history of credit cycles suggests property prices could revert by 30% nationally and remain moribund for several years.

How many of the leveraged investors/speculators, homebuyers, refinancers, lenders and developers (see Greater Toronto Real Estate Development files insolvency after inflation squeeze) who banked on ever-escalating prices and ultra-low interest rates will be content or able to hold on through a housing bear market where the economy slumps and unemployment rises. Looks like we are going to find out.