Since its peak at the end of 2021, nearly $8 trillion in market cap has been knocked off the S&P 500 alone. This comes with a 24% loss in the average NASDAQ stock and a 55% drop in Bitcoin, not to mention even larger declines in many individual stocks and crypto-currencies globally.

Asset bubbles give and then their busts taketh back. Losses naturally hit the wealthiest most since the top 1% owns more than half of US equities and equity funds, while the bottom 90% owns less than 12% (Fed estimates).

So far, the two wealthiest people in the world, Elon Musk and Jeff Bezos, who made fortunes as their company shares ballooned in recent years, have lost an estimated 41% and 39% of their net worth since just November. Though still billionaires, net worth declines tend to have a negative psychological impact on everybody. For the masses though, significant losses can be life-plan-harming.

At the same time, borrowing costs have risen and corporate profits are declining. The combination is starting to prompt the usual cutbacks and layoffs just as households are indebted, cash light and highly levered on a housing bubble that’s now also beginning to mean-revert. This has broad impacts because the bottom 90% owns more than half of the housing market cap (the top 1% holds less than 14%).

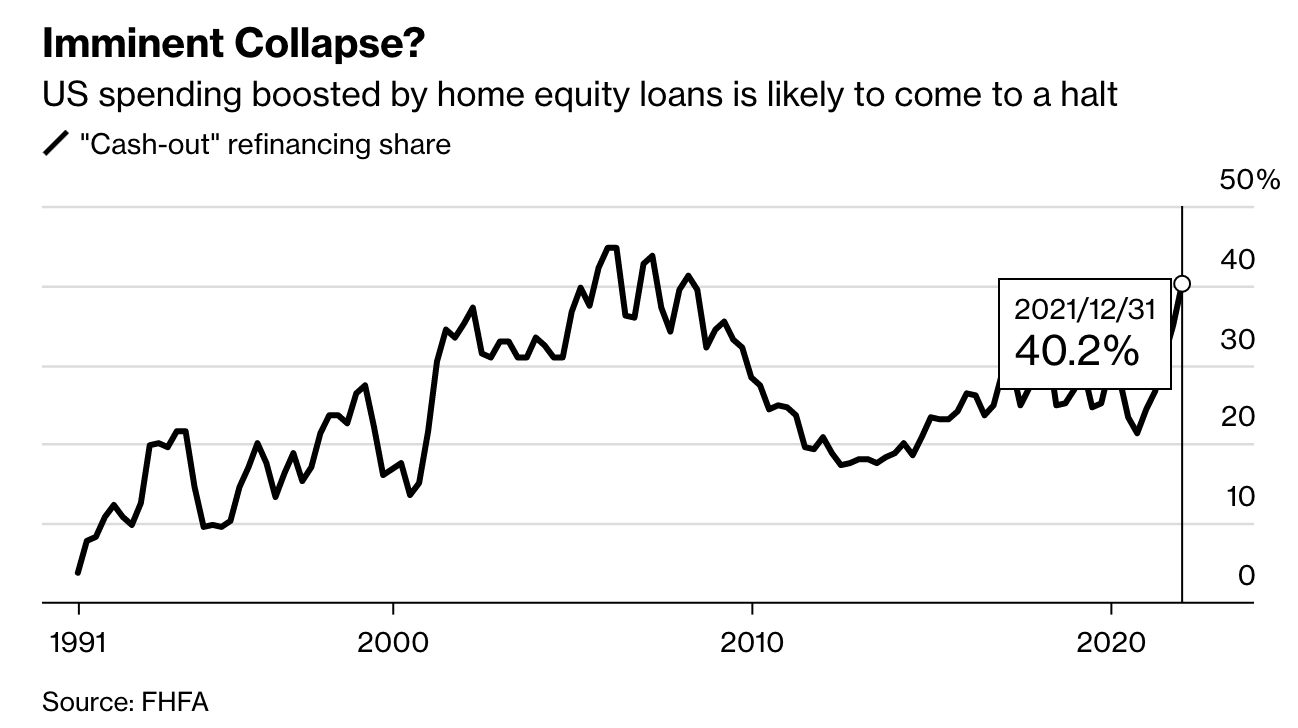

As home prices were leaping over the past few years, households sustained spending by borrowing against their rising equity. As shown below, the US ‘cash-out’ refinancing share revisited 40% at the end of last year. See: A ‘wealth shock’ is cracking American’s nest eggs. We saw this movie in the 2003-06 cycle when low rates drove similar behaviour into the 2007 bubble top.  Now that rates have risen and home prices are stagnating and reversing in many markets, consumers are less able to tap their home equity to access more credit. Home prices that rose 30 to 50% in the last two years can decline that much and only return to where they were before the pandemic.

Now that rates have risen and home prices are stagnating and reversing in many markets, consumers are less able to tap their home equity to access more credit. Home prices that rose 30 to 50% in the last two years can decline that much and only return to where they were before the pandemic.

A ‘paper loss’ of home equity does not have to be a big deal for those who have not borrowed against notional prices in recent years. But for those who have, it can be catastrophic. Many used ‘cash out’ loans to buy other inflated assets or help family members also lever into the property bubble.

A correction of 20% can completely evaporate the notional equity that conventional mortgagors thought they had and leave negative equity for years to come. This is why housing busts tend to be deeply scarring– financially, psychologically and economically.

It’s spooky that this cycle has combined the worst elements of the 2000 tech top and the 2007 housing top into one super-bomb for net worth and the consumption-dependent global economy. And yet, here we are.

The 2022 Housing Crash has started. Home Prices are dropping by 20% in some neighborhoods. Check Zillow to see for yourself. The US Housing Market Bubble is turning into a Crash very fast. Here is a direct video link.