With most assets dropping in 2022, the US dollar (DXY) has been a rare standout, up 25% against a basket of global trade currencies since December 20, 2020, and 17% year to date. As with most trends, it’s common for humans to expect the status quo to continue indefinitely. Nothing ever does.

After bouncing for a couple of days earlier this week, risk markets are under pressure again, and the DXY topped $112 this afternoon, up from $110.06 on October 5.

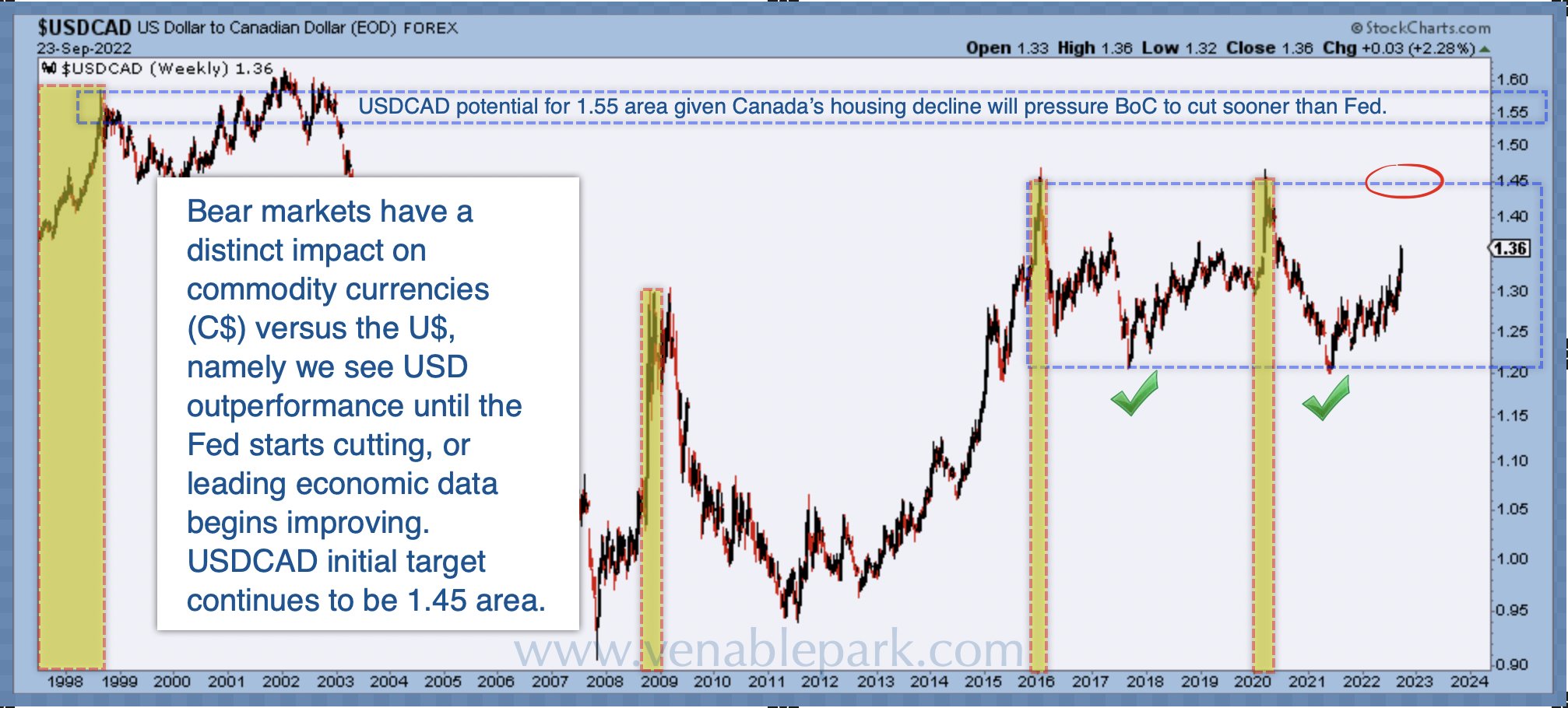

The greenback has gained against Canada’s petro-dollar even as oil has bounced this week on news of OPEC output cuts. The USD/CAD, above $1.374 today, is nearing the $138.26 high last touched on September 30.

It is important to remember that markets are discounting mechanisms and relative moves are cyclical, not permanent. It’s typical for the USD to outperform in the early stages of recession and bear markets as commodity demand falters with global manufacturing and trade, and capital flows seek relative safety. We are there now.

The World Trade Organization joined the bearish chorus this week in lowering its global 2023 economic growth to 2.3% (below 3% is considered recessionary) from earlier expectations of 3.3%. They also warned of an even sharper slowdown if central banks continue sharp monetary tightening to squash inflation.

As shown below, since 1998, from my partner Cory Venable, the USD/CAD could well trade up to the 1.40-1.45 range (red circle) in the coming months as equity markets work towards a bottom. With the double whammy of housing weakness in Canada’s highly levered economy, we could even see the loonie revisit the $1.50+ area reached during the 2000-02 equity bear market. Canada didn’t enter a recession in 2001, but our dollar still dumped, and our stock market halved. The great white north comes into this downturn with a more vulnerable setup than in 2000 or 2008. We shall see.

The US Fed will eventually abandon its demand and inflation-crushing mission; however, monetary policy moves through the economy with a multi-month lag. When the Fed pauses, USD weakness and a fleeting stock market rebound are typical, but the economy does not turn on a dime.

Equity bottoms have historically come with loonie bottoms several months after the Fed returns to slashing rates again (marked with yellow bands above). Still, wise capital management does not bet on definite timing for these cycles to unfold.