Today, we have news that the Canadian and US economies are estimated to have created more jobs in September than forecast. Still, hourly earnings moved down, and unemployment rates in both countries have moved above cycle lows.

It is helpful to remember that unemployment is a lagging indicator, with the bulk of upward moves happening 12 to 24 months after central banks end their tightening efforts. As we enter the final quarter of 2023, central banks still threaten more rate hikes while contracting their monthly balance sheet (QT). Unfortunately, we are early in this job loss cycle.

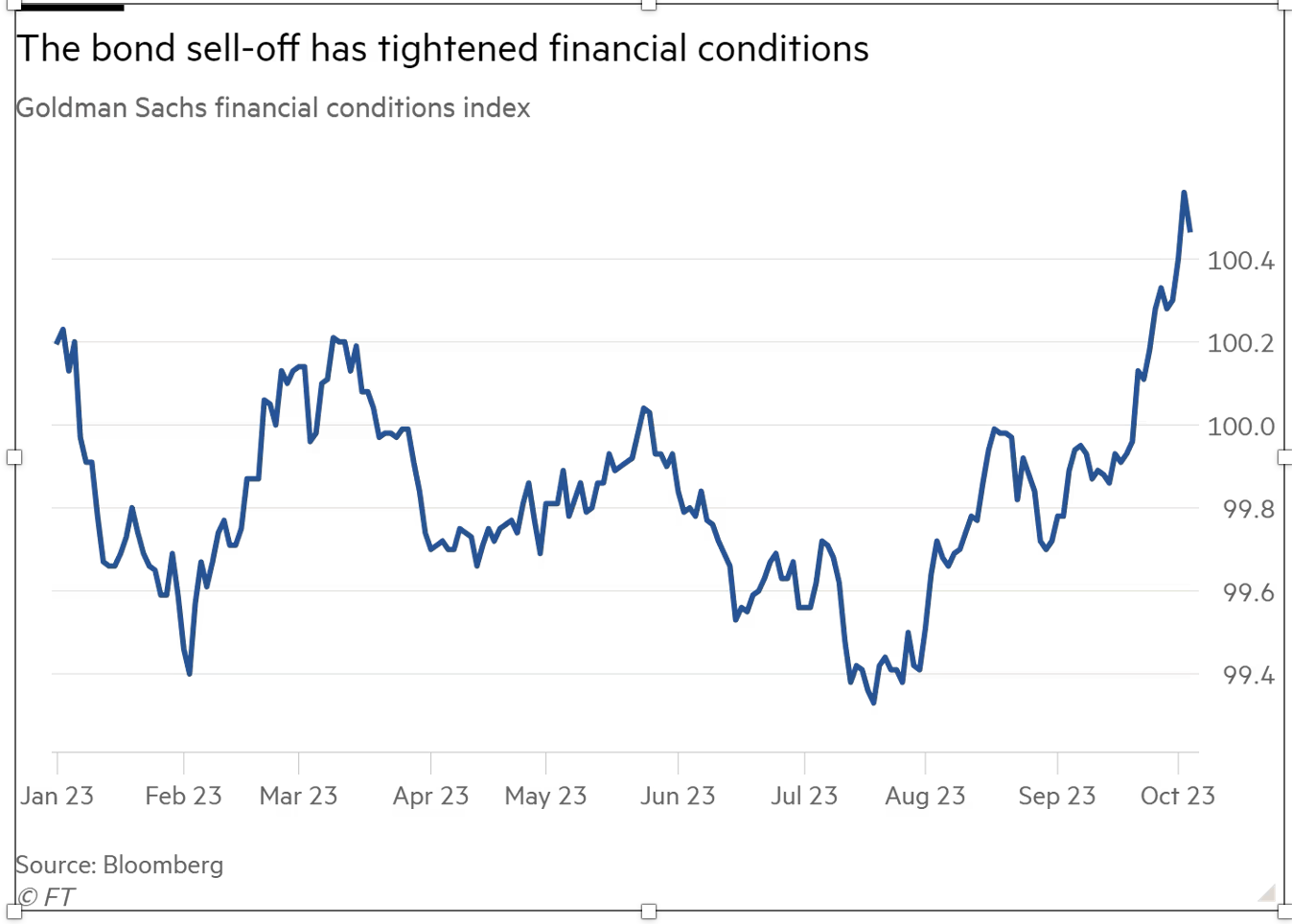

Stock, bond, real estate and commodity markets are all in the red on the fear that more robust job creation will prevent central banks from loosening credit conditions. That may be true. But the bond market sell-off has already done a mother-load of tightening work for central banks, especially in the last month.

As bond prices have fallen, their higher yields have jacked financing costs for households, businesses, and governments to the highest in over 15 years. This is beginning to exert an enormous drag on the global economy and increases the odds that central banks will want to ease financial conditions in 2024 more than most imagine. See Treasury rout bolsters view that Fed will call time on rate rises. Buying power has slumped for all manner of goods, services, and assets, including share buybacks–all no longer enabled by cheap credit.

Buying power has slumped for all manner of goods, services, and assets, including share buybacks–all no longer enabled by cheap credit.