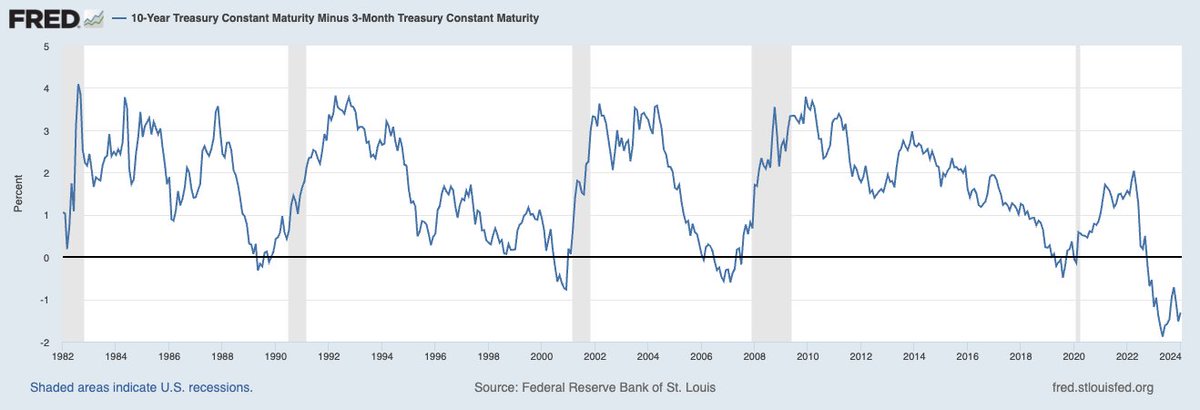

The US 10-year Treasury yield has been below the 3-month yield since November 2022 (14 months and counting). This rare yield ‘inversion’ has preceded each recession (grey bars) since 1982, with no false signals. As usual, equity bulls perpetually bet this time will be different. In past cycles, the US Fed stopped hiking when the yield curve inverted, but unusually, this time, they overlooked the warning and continued to hike as the inversion deepened.

In past cycles, the US Fed stopped hiking when the yield curve inverted, but unusually, this time, they overlooked the warning and continued to hike as the inversion deepened.

These are complex systems with variable lag times, and being alert for recessions requires attention span, independence, maturity and discipline. However, given the significant financial implications, not staying alert for recessionary signals ends up being much worse in the end. Individuals must decide how to manage their financial risk accordingly.

The economist who first documented the predictive power of inverted yield curves explains the history in the segment below and why a recession is indicated in 2024. Cam Harvey is a Professor of Finance at Duke University’s Fuqua School of Business, Research Associate of the National Bureau of Economic Research (NBER), Director of Research and Partner at Research Affiliates.

Harvey argues that since his 10-year / 3-month signal inverted in the fall of 2022, the first and second quarter of 2024 is when a potential economic slowdown would occur (the average lag between the inversion of the 10-year / 3-month spread is 12 months, but the longest lag is 22 months). However, Harvey notes that there are several positive forces supporting the U.S. economy, such as fiscal stimulus and a strong labor market, as seen by job vacancies in excess of unemployment. While Harvey hopes that these forces can induce a “soft landing,” it is his base case that the 10-year / 3-month inversion will go 9 for 9 in forecasting an economic slowdown. Here is a direct video link.