A recent Pew report on the dilapidated condition of most public pension funds today, offers perspective on the trouble with highly manipulated, over-valued investment markets and unreasonable return assumptions. See: State Public Pension Investments shift over past 30 years.

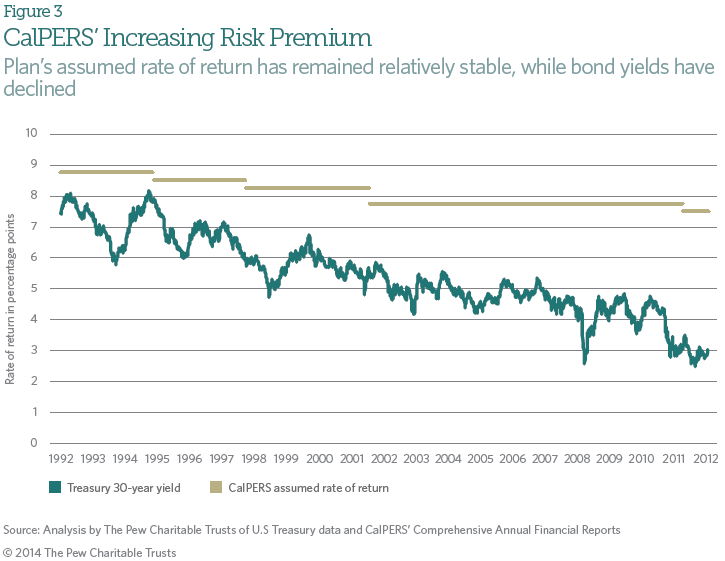

As shown in the chart below, US 30-year government bond yields have fallen steadily from north of 8% in 1992 to a low of 2.55% in July 2012 (green line below). But rather than admit math, reduce return expectations and increase contribution levels as rates fell, pension boards and individuals maintained return assumptions above 8% (gold line below) and looked to investment gurus and financial wizards for magic “strategies” to bridge funding gaps.

In 1982, nearly 80 percent of public pension assets were held in the lowest risk bonds and cash; by 2012, the share had fallen to 25 percent, with a whopping 75% of pension assets now reliant on the fate of the riskiest asset classes of stocks, commodities and other derivatives. At the same time, fees paid to financial consultants and managers jumped by 30 percent between 2006 and 2012, according to the Pew report.

While greater risk concentrations look genius during periods of price expansion, they encourage continued under-funding and unreasonable expectations. Then when the repeated down cycles hit they prove financially devastating–wiping out years of apparent investment gains in a matter of months.

Clearly the strategy is not working as even after an unusually large rebound in stocks the past few years, per the latest data available (2012), states still had only $3 trillion in funds to meet the more than $4 trillion in benefits earned by public workers. A recent Bridgewater study estimated that 85% of public pension plans are likely to be bankrupt within 30 years on present funding plans.

Unreasonable expectations, also enable politicians, individuals and managers to make short-term focused, long-term harmful financial decisions: New Jersey, Republican Gov. Chris Christie, recently announced a plan to divert $2.4 billion in pension payments to close the state’s $2.7 billion budget gap. The pension plan was already woefully underfunded: New Jersey contributed just 39% of the annual required to meet its estimated $47 billion pension liability.

The next bear market will once more reveal the reckless ideas and foolish strategies so widely in vogue today. There will be lawsuits and blame to go all around; but none of that will make up for the gaping capital holes caused by unreasonable belief in risky assets and chronic under-saving.

The time to see the error of these ways and adjust financial plans and behavior is now, before the next mean reversion in risk markets hits.