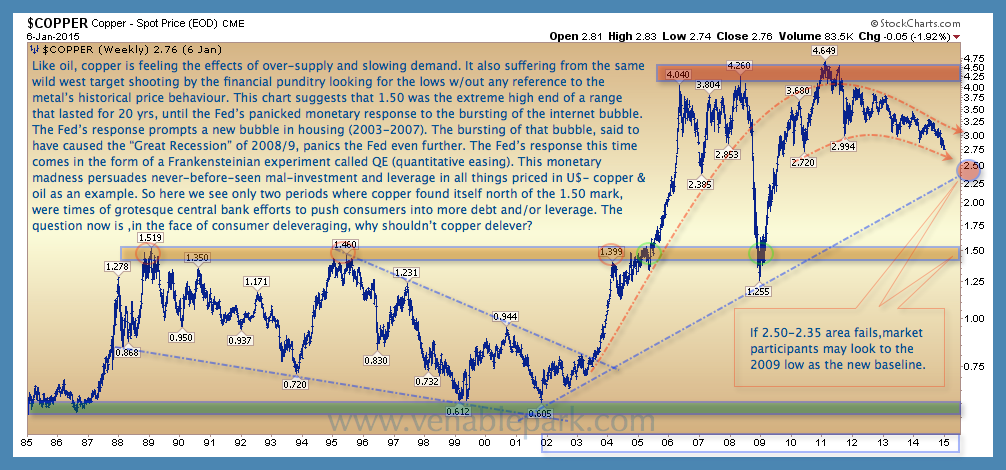

This afternoon’s Fed minutes reflect the usual team of congenitally confused academics wandering around in circles of economic theory. Bottom line: they still think inflation and growth will pick up this year (as they have expected every single year) and that they are likely to raise interest rates by April. The bond market seems to disagree: the 10 year treasury yield has continued to move lower today, now handily below 2%.

And Dr. Copper–that much maligned and manipulated economic indicator the past 4 years–seems to be yawning in the Fed’s general direction. Today at 2.76 (down 41% since QE-faith peaked in 2011), a breach of the 2.35-2.50 secular support line (since the credit-fueled commodity boom began in 2002), would confirm longer-term deflationary forces that the Fed so far believes are ‘transitory’. After that, we would look for a round trip back into the pre-credit bubble band below $1.50 a pound (between green and orange lines below).