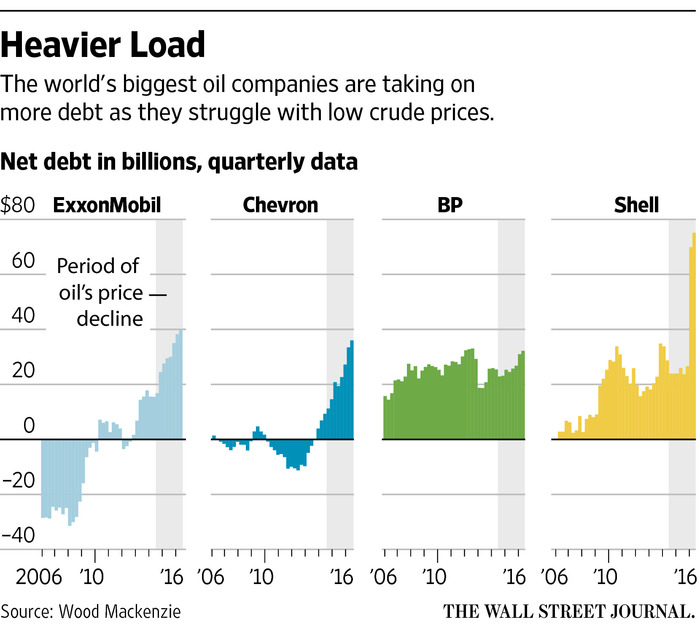

The world’s largest fossil fuel companies, Exxon Shell, BP and Chevron have more than doubled their debt levels since oil prices turned down in 2014.

Unfortunately they have not borrowed to proactively reinvent themselves into cutting edge energy companies focused on a diverse range of smart, clean resources and technology–nope, these dinosaurs have borrowed to maintain antiquated operations, share buybacks and dividend payments to shareholders.

Unfortunately they have not borrowed to proactively reinvent themselves into cutting edge energy companies focused on a diverse range of smart, clean resources and technology–nope, these dinosaurs have borrowed to maintain antiquated operations, share buybacks and dividend payments to shareholders.

See Big Oil Companies Binge on Debt:

Here is madness that any small business owner could recognize: the companies spent more than 100% of their profits on dividends last year. Sound management?

This year, the problem got worse. In the April-June period, Exxon paid $3.2 billion in dividends and had just $1.7 billion in net income, according to S&P Global Market Intelligence. Shell paid $1.26 billion in interest in the first half of 2016, compared with $726 million in the same period a year earlier.

The c-suite says it’s confident they should be able to maintain current operations and dividend payments so long as the oil price stays between $50 and $55 a barrel next year. There is no plan B. And of course, none of these experts ever expect price declines.

As usual management has been incentivized to focus on boosting share prices and dividends rather than smart business operations, and are taking another page from the Kodak playbook. (see: We’re paying CEO’s all wrong). No need to evolve or innovate or embrace the future, just maintain the status quo, keep borrowing and hope that price turns up before the companies go bankrupt. How much did you pay for that MBA diploma again?

Bond funds and managers desperate for income have been buying the debt to date, but it seems already highly exposed banks, are finally getting nervous and pulling back. See: Oil patch taps funds for credit as Canadian banks pull back.