Retirement savings shortfalls are not a new problem, they have been visible on the horizon for at least the last 20 years. Willfully blind workers and savers have been misled by dishonest projections from financial sales firms and academics that have collected fees and refused to address the underlying problem of savings deficits.

Lance Roberts correctly points out that markets compound a smoothed annual return in theory, but not in real life. In real life, negative returns and bear markets set capital projections many years behind target. Pretending that these set backs will be caught up over time without topping up contribution levels to target each year, is irresponsible, wishful thinking. The savings deficit problem grows larger every day it remains ignored.

Here is a link to Lance Robert’s recent article The pension crisis is worse than you think. Here’s a key excerpt:

Given real-world return assumptions, pension funds SHOULD lower their return estimates to roughly 3-4% in order to potentially meet future obligations and maintain some solvency.

They won’t make such reforms because “plan participants” won’t let them. Why? Because:

It would require a 40% increase in contributions by plan participants which they simply can not afford.

Given that many plan participants will retire LONG before 2060 there simply isn’t enough time to solve the issues, and;

The next bear market, as shown, will devastate the plans abilities to meet future obligations without massive reforms immediately.In a recent note by my friend John Mauldin, he discussed an email Rob Arnott, of Research Affiliates, sent regarding this specific issue.

“If our logic is sound, we earn 0.8% from our bonds (40% allocation x 2% return) and 2% to 3.2% from our stocks (60% x 3.3%, or 60% x 5.4%). Add up the return from stocks and the return from bonds, and we get 2.8% to 4% from our balanced portfolio.”

For those who are fully invested at present levels, this best case portfolio return of 2.8% to 4% annually is before fees and taxes, and assuming no negative or bear market loss years in the investment horizon. Sound likely?

Even if one is able to attain this best case return target, most retirees will have to learn to live on much lower income than they are expecting, and/or continue working at least part time well into their 70’s, and/or start saving a much higher percentage of their income asap so as to increase their savings to the target level of capital needed.

In addition to spending less in order to increase our savings levels now, a higher probability approach to achieving desired capital targets is to minimize exposure to over-valued assets today in ‘the everything bubble’, in preference for holding cash and liquid equivalents (highest quality bonds and certified deposits) while we patiently wait for the opportunity to buy equities, corporate bonds and real estate again when they are on sale in the next bear market.

If we can avoid capital losses in the near term and then buy investment-worthy assets after they have dropped in price and offer much less capital risk and much higher income yields again, then there is hope for higher compound returns for many years thereafter. It’s getting from now to then that takes great personal discipline and fortitude amid the madness of crowds.

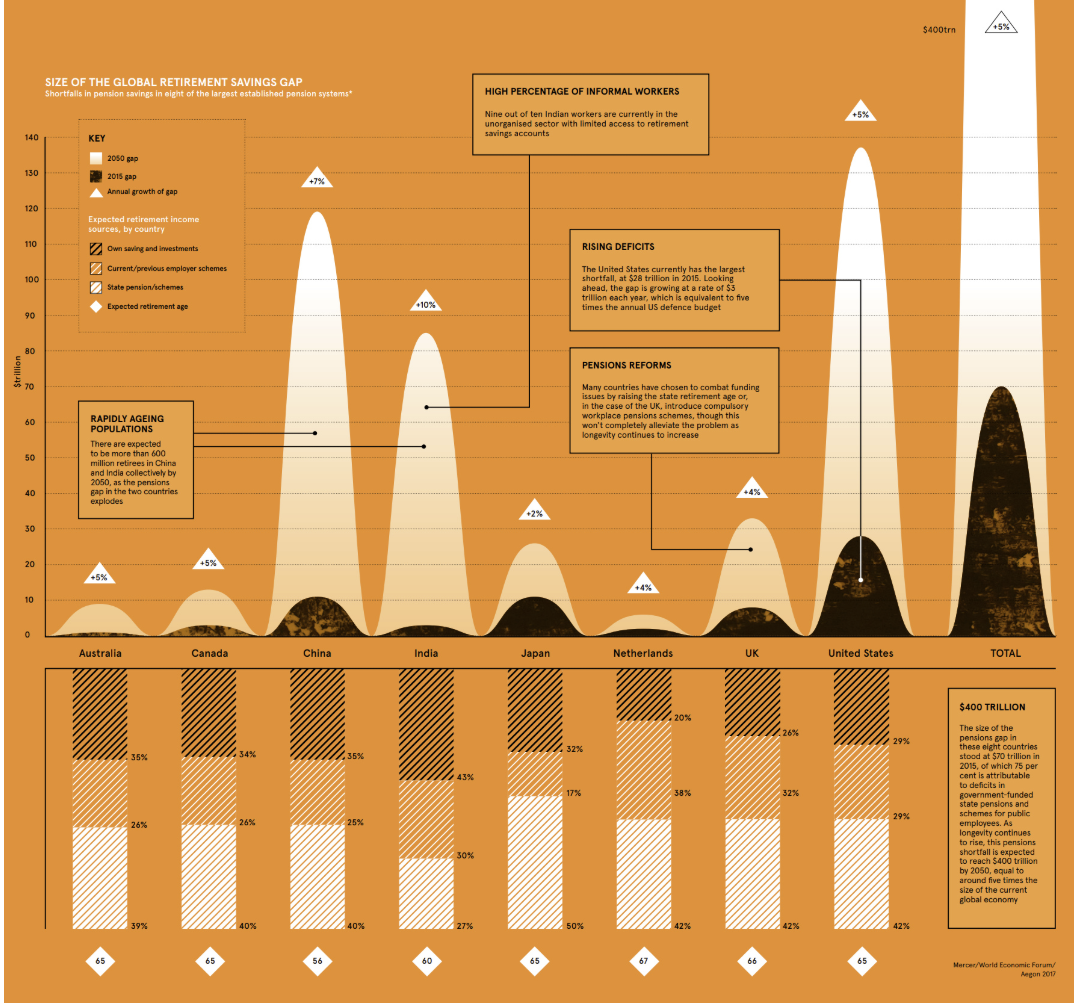

In the meantime, see The Pension time bomb: $400 trillion by 2050. Here’s the graphic of savings deficits for the masses globally.