For an important historical perspective on the tensions playing out between China and other trading partners today, I recommend reading ‘How Asia Works.’

Other numbers to illuminate the relative bargaining power between China and the US are that US exports to China make up just .55%, and imports from China just 2.38% of America’s GDP, while China’s exports to the US make up 18% of its GDP (21% to North America overall). China is the second largest importer of global goods (10%) behind the US (14%), however much of this is for processing and export rather than domestic use. Netting this out, economist A. Gary Shilling has estimated that two-thirds of the net value of all Asian exports are bought by Americans.

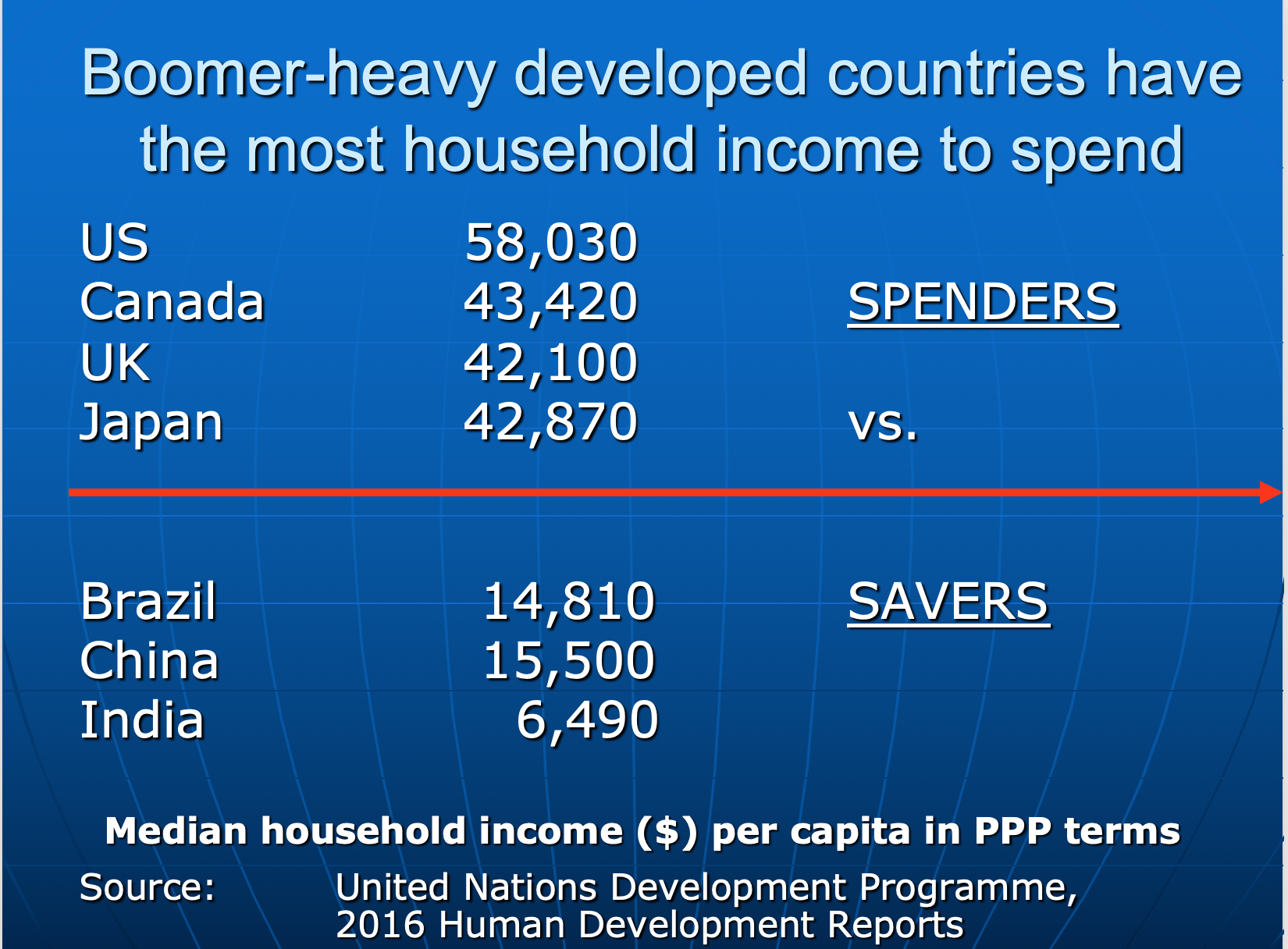

At the same time, as s hown on left, China enters this global downturn with average household incomes still about one third of those in developed nations like the US and Canada (purchasing power parity). It is not surprising then that Chinese household consumption drives just 39% of their national GDP compared with 77% in the US and 58% in Canada.

hown on left, China enters this global downturn with average household incomes still about one third of those in developed nations like the US and Canada (purchasing power parity). It is not surprising then that Chinese household consumption drives just 39% of their national GDP compared with 77% in the US and 58% in Canada.

In short, China has most to lose in a highly indebted world of aging western consumers, now pushing back from two decades of globalization and hyper-consumption, in favor of downsizing, experiences more than things, and rebuilding coffers at home. Meanwhile, resistance to Chinese companies acquiring businesses abroad is also rising, as explained in this clip.

Over the last five years, China has spent unprecedented amounts overseas, but now the acquisitions are drying up as national security concerns worry the west. James Fontanella-Khan and Arash Massoudi, the FT’s corporate finance and deals experts, explain why the US, Europe and others have become wary of China and brought in measures to limit foreign takeovers. Here is a direct video link

.