Two thousand twenty-two vaporized $25 trillion of notional equity value from global balance sheets, and the global bond market lost nearly $10 trillion more. Together, the decline in these two asset classes amounted to about a third of the world’s 2022 103.86 trillion GDP, not counting ongoing losses in real estate, commodities, or the crypto space.

So far, 2023 has come in like an ongoing bear for stocks and commodities, while government bonds have seen their best start to any new year in more than 20 years. These moves make sense in the macro context of a 2023 global recession where revenue, profits inflation and interest rates are due to decline.

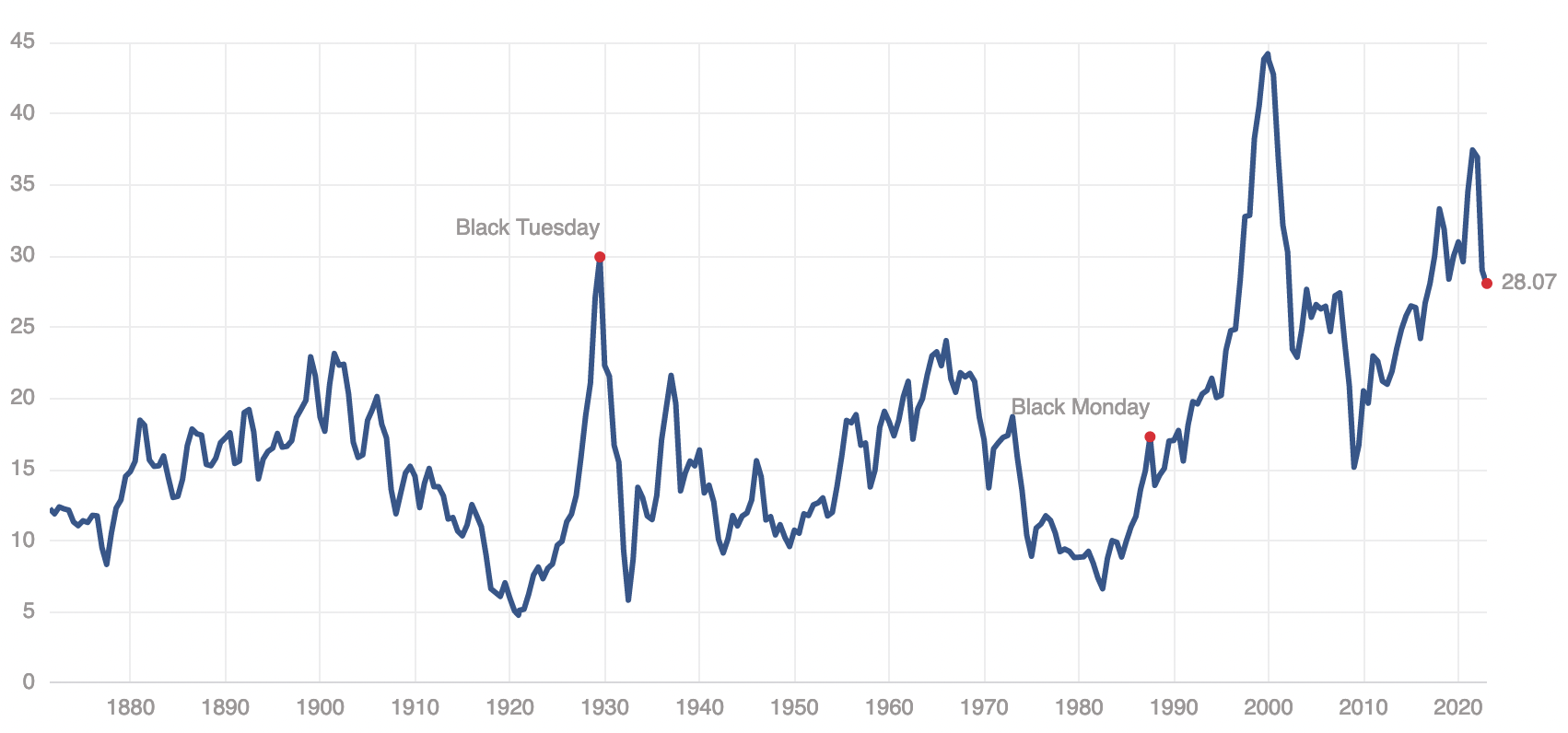

Stocks remain especially vulnerable since, even with last year’s drubbing, they enter 2023 still at the high end of historical valuations. The S&P 500’s Shiller CAPE (shown below since 1870) closed in 2022 at 28, down from 38.3 at the end of 2021. A CAPE of 28 is nearly identical to the stock market peak in October 2007 and nearly double the 50-year mean of 14.6. At past cycle lows like March 2009, this reading was 13.3, 22 in October 2002, 17.8 in July 1990, and 6.6 in August 1982. We still need to head significantly lower in equity valuations if we are to restore longer-term investment prospects. Thus far, the Powell-led Fed seems willing to serve as the repricing catalyst.

For those hoping that 2023 will bring positive equity returns because 2022 saw losses, it’s worth noting that past equity bubble busts in 2000-02 and 1973-74 saw consecutive negative return years.

It takes some effort to appreciate the extent of the asset bubbles that have been, but doing so helps to imagine the mean reversion that would be historically typical from here.

One of many poster children for the mania aftermath is Tesla. Tesla’s fundamentals have been solid, with new car deliveries (+185% between Q1 2020 and Q3 2022), revenue (+175%) and net income (+1876%). Yet, Tesla shares have fallen nearly 74.5% from their cycle peak in November 2021 (from $411 to $105 at yesterday’s close). Still, even with the deletion of 75% of notional equity over the last 13 months, Tesla shares remain 268% higher in the previous three years. They are vulnerable to further mean reversion as speculative mania enters its typical depression phase.

Valuable investment opportunity lies ahead for many asset classes, potentially within the next year or so.