With higher oil prices expected to impact inflation, financial markets shifted from anticipating rate cuts to considering the possibility of rate hikes in Canada. In response, longer-term bond yields rose for the first couple of weeks of March, pushing up borrowing costs.

About 1.15 million Canadians are expected to renew their mortgages in 2026.

Renewing at today’s best 5-year fixed bank rate of 4.45% (up from 3.94% at the end of 2025) would push monthly payments above $3,400 for a typical borrower (average home price of 698K with 10% down and a 25-year amortization) — an increase of roughly $1100 per month since 2020 (when rates were about 2%)–payments up about 45%. Also, as credit conditions tighten and employment conditions weaken, it becomes harder to qualify for loans.

Weak labour data and downside risks associated with the upcoming review of the Canada‑United States‑Mexico Agreement (CUSMA) help reduce pressure on the Bank of Canada to hold tight against what may prove to be a temporary, highly uncertain, supply shock.

Many forecasters now frame 2026 as a set of competing scenarios — a prolonged hold at the current 2.25% overnight rate if trade uncertainty drags on, a mid-year cut if growth falters materially, or a late-year hike if resilience persists and inflation proves sticky.

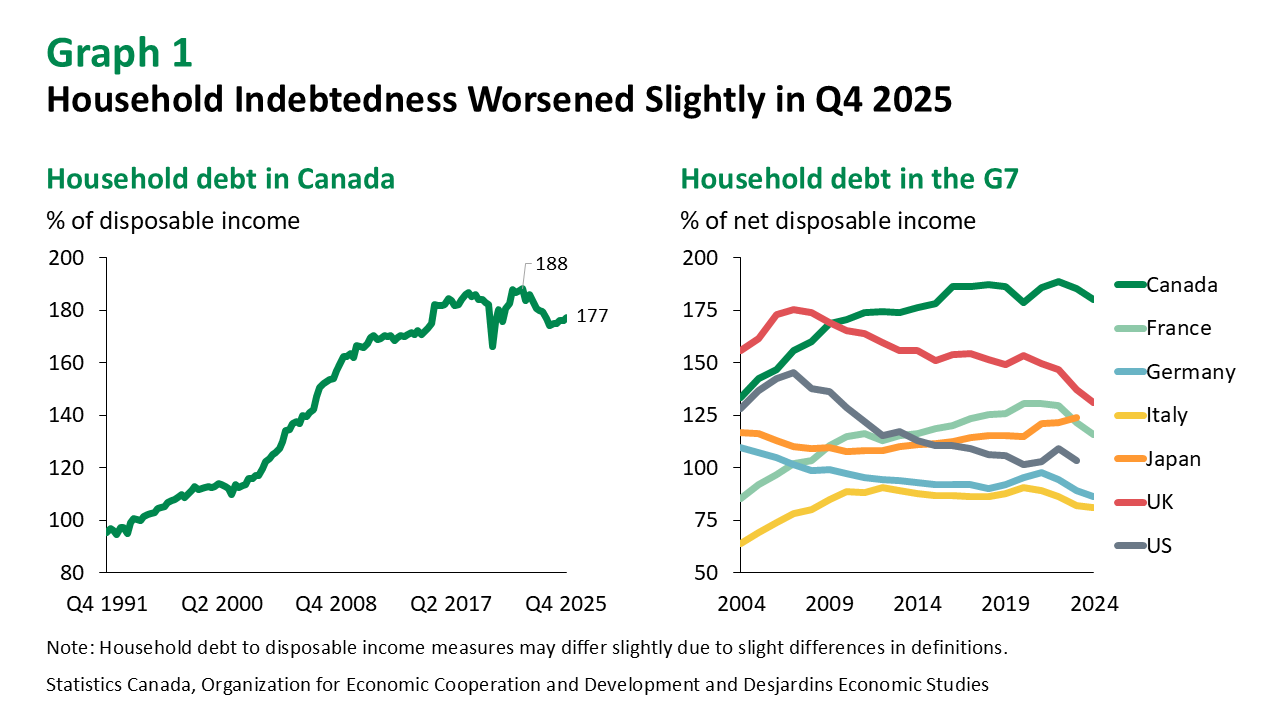

Facts on the ground show that despite the BoC lowering its policy rate from 5% to 2.25% since June 2024, a record 15% of Canadian household disposable income is today going toward servicing debt payments — a larger percentage than when policy rates were double-digit in 1990. Today, it’s the level of debt that’s the problem.

Canadian household debt was above 177% of disposable income in the final quarter of 2025 (as shown on the lower left since 1991), and still, by far, the highest of G7 nations (shown on the right since 2004, courtesy of Desjardins).

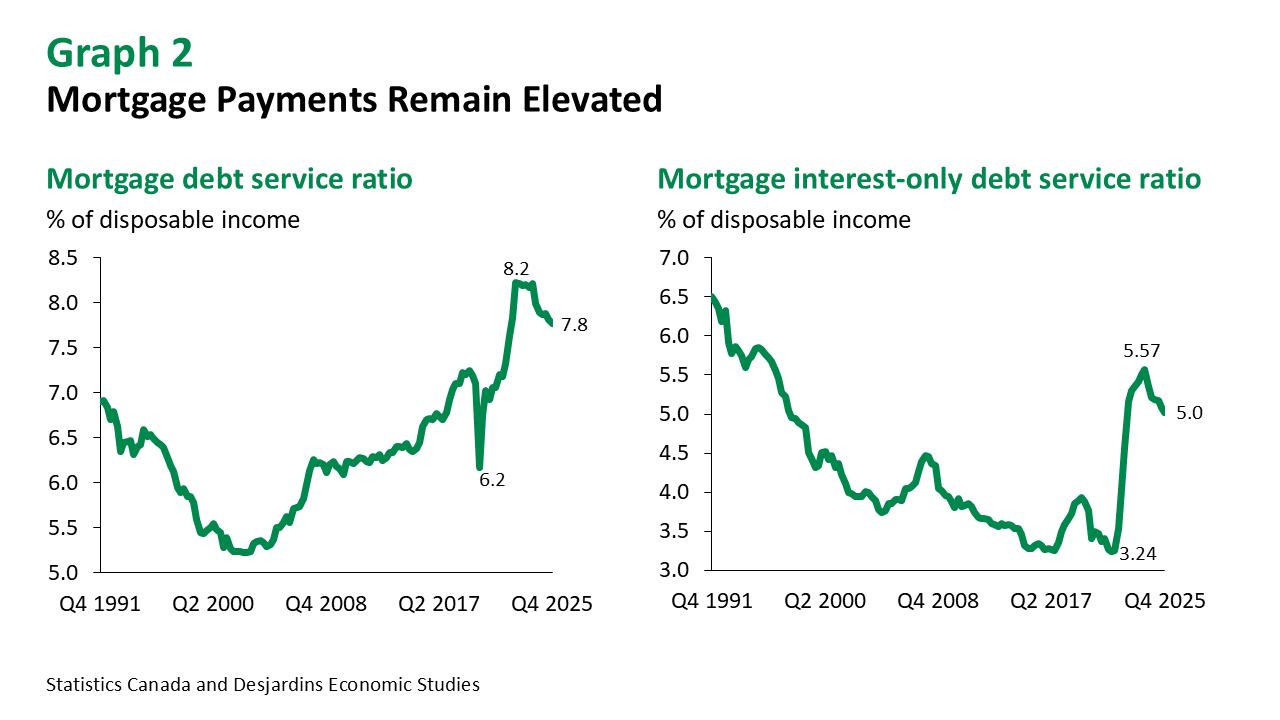

The home price bubble ballooned mortgage debt along with it. While prices have been falling in many areas, mortgage debt remains elevated, with those payments swallowing up nearly 8% of disposable income alone (on the lower left since 1991). The mortgage interest debt service ratio is barely off its 2025 high (lower right since 1991).

The home price bubble ballooned mortgage debt along with it. While prices have been falling in many areas, mortgage debt remains elevated, with those payments swallowing up nearly 8% of disposable income alone (on the lower left since 1991). The mortgage interest debt service ratio is barely off its 2025 high (lower right since 1991).

The Bank of Canada estimates that the weighted average interest rate paid by households across all credit types is 4.75% today, and 4.48% for businesses (link here), significantly higher than the cycle low of about 3.5% in 2020-21.

The Bank of Canada estimates that the weighted average interest rate paid by households across all credit types is 4.75% today, and 4.48% for businesses (link here), significantly higher than the cycle low of about 3.5% in 2020-21.

As employment conditions deteriorate, the share of Canadian households more than 60 days behind on debt payments reached multi-year highs across all loan types in the 4th quarter of 2025 (Equifax).

We think rate cuts remain more likely than hikes in 2026, and they won’t help as much as hoped.

If the economy slows enough, treasury prices should rise (they started to this week) and that will bring fixed interest rates down some more. But it’s still going to take time to work debt levels down to where households can rebuild financial resiliency and free cash flow.

Douglas Porter Chief Economist at BMO Financial Group talks to Financial Post’s Larysa Harapyn about how the energy crisis unfolding in the Middle East could impact Canada’s economy. Here is a direct video link.