History does rhyme.

The OPEC oil embargo began in October 1973, when Arab members of OPEC announced an embargo against the United States, Canada, Japan, and Western European nations in retaliation for their support of Israel during the Yom Kippur War.

The embargo lasted until March 1974, and its effects were long-reaching:

Oil prices quadrupled almost overnight, from about $3 per barrel to nearly $12.

Long gas station lineups became a defining image of the era in North America.

To curb demand, speed limits were lowered, daylight saving time was extended, and energy conservation became a national priority in many countries.

It triggered a broader economic recession and fundamentally changed how Western nations thought about energy security.

There was a second oil shock in 1979, triggered by the Iranian Revolution, which caused another dramatic spike in oil prices and is sometimes conflated with the 1973 crisis.

Together, the two events reshaped global energy policy, spurred investment in fuel-efficient cars, and accelerated interest in alternative energy sources, which ultimately helped reduce oil demand and prices.

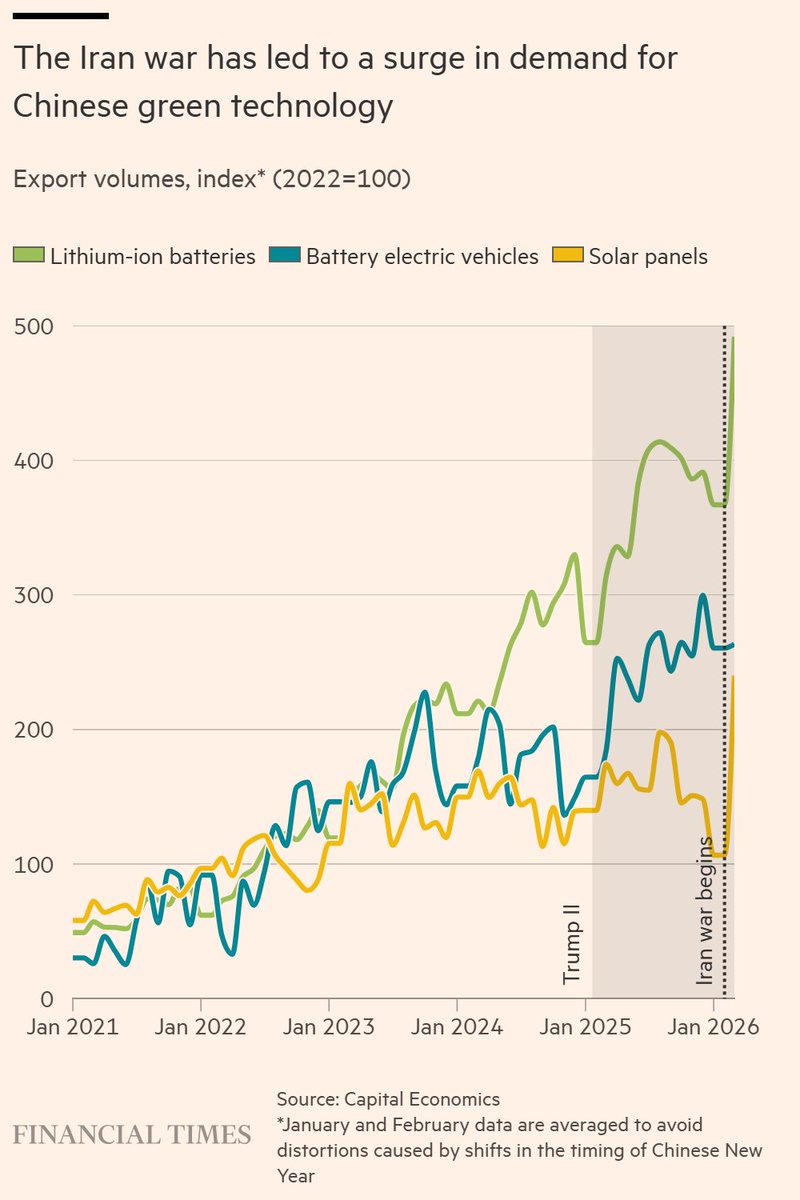

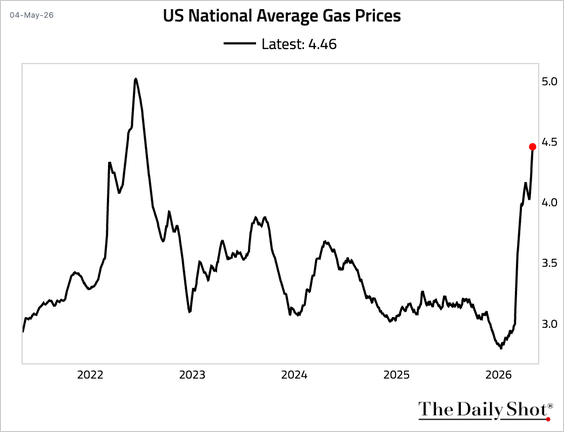

Similar effects are happening now. See, the U.S. president has inadvertently increased the appeal of renewable energy and EVs worldwide. The surge in the average price of gas from less than $3.00 US a gallon in January to $4.46 US is a heavy tax on already stressed consumers and businesses (below since 2021, via The Daily Shot).

The surge in the average price of gas from less than $3.00 US a gallon in January to $4.46 US is a heavy tax on already stressed consumers and businesses (below since 2021, via The Daily Shot).

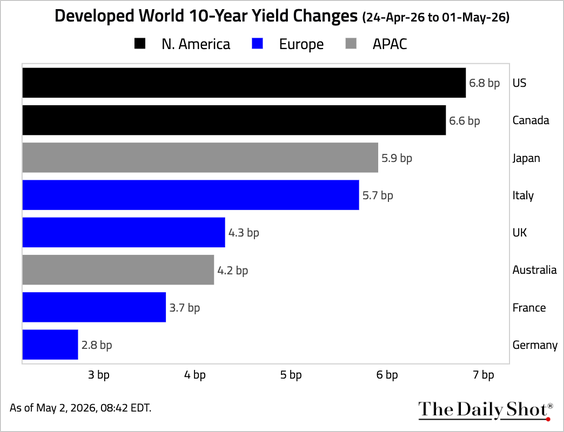

At the same time, fears about how long inflationary pressures may last have caused a rise in Treasury yields (and therefore an increase in fixed borrowing rates) in most major economies (shown below since April 24), along with expectations that central banks will stay on hold before raising policy rates in 2027. We shall see.

At the same time, fears about how long inflationary pressures may last have caused a rise in Treasury yields (and therefore an increase in fixed borrowing rates) in most major economies (shown below since April 24), along with expectations that central banks will stay on hold before raising policy rates in 2027. We shall see. Since the late 1970s, the US Fed has not raised its policy rates during an oil price spike while unemployment was rising (Rosenberg Research), because these conditions worked to curb growth and inflation without central bank tightening. The economic downturn then led central banks to ease monetary policy, and Treasury yields to fall as the economy slumped.

Since the late 1970s, the US Fed has not raised its policy rates during an oil price spike while unemployment was rising (Rosenberg Research), because these conditions worked to curb growth and inflation without central bank tightening. The economic downturn then led central banks to ease monetary policy, and Treasury yields to fall as the economy slumped.

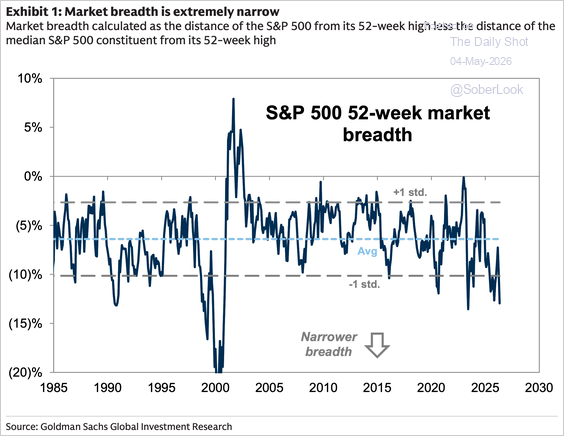

While a handful of companies led another sharp rebound in stock markets since the end of March, participation has been slim: equity market breadth (the number of companies making new 52-week highs) has been among its lowest levels on record (shown below since 1985). Eventually, the weight of the world is likely to exert more force than a frothy few.

In January 1973, the Dow Jones Industrial Average peaked at an all-time high of around 1,050 before falling sharply — by late 1974 it had dropped about 45%, bottoming out around 577 in December 1974. This crash was driven by the OPEC oil embargo, stagflation (high inflation + low growth), and the Watergate political crisis, undermining confidence.

In January 1973, the Dow Jones Industrial Average peaked at an all-time high of around 1,050 before falling sharply — by late 1974 it had dropped about 45%, bottoming out around 577 in December 1974. This crash was driven by the OPEC oil embargo, stagflation (high inflation + low growth), and the Watergate political crisis, undermining confidence.

Although the stock market recovered through the mid-to-late 1970s, it never convincingly broke back above that 1973 high during the decade. It wasn’t until 1982–1983 that the market finally broke decisively above that 1973 peak and began the great bull market of the 1980s, which began from single-digit price-to-earnings multiples and rich dividend yields.

So in short, if you had invested at the 1973 peak, you essentially waited nearly 10 years to get back to even — and given inflation over that period, you actually lost significant purchasing power in real terms. It’s often cited as one of the most difficult extended periods in U.S. stock market history. That said, those who were able to deploy cash into dividend-paying equities during the 1973-74 bear market benefited for years to come. Those who live to see it will discover whether this cycle rhymes.

DDB offers a worthwhile review of economic impacts in the segment below.

We are breaking down the latest Federal Reserve split, Jamie Dimon’s private credit warning, and why the K-shaped economy is masking a hidden middle-class recession. Kitco News Anchor Jeremy Szafron sits down with Fed insider Danielle DiMartino Booth, CEO of QI Research, to expose the real data behind the Wall Street headlines. From the largest Fed committee dissent since 1992 to major private credit write-downs and hidden job losses in the labor market, DiMartino Booth explains why the central bank may be “too late” to the easing process. The discussion also covers commercial real estate stress, the freezing housing market, how AI is impacting temporary employment, and what Tether’s $20 billion physical gold hoard signals for the U.S. dollar and global capital flows. Here is a direct video link.