A few charts to illuminate the start of another week.

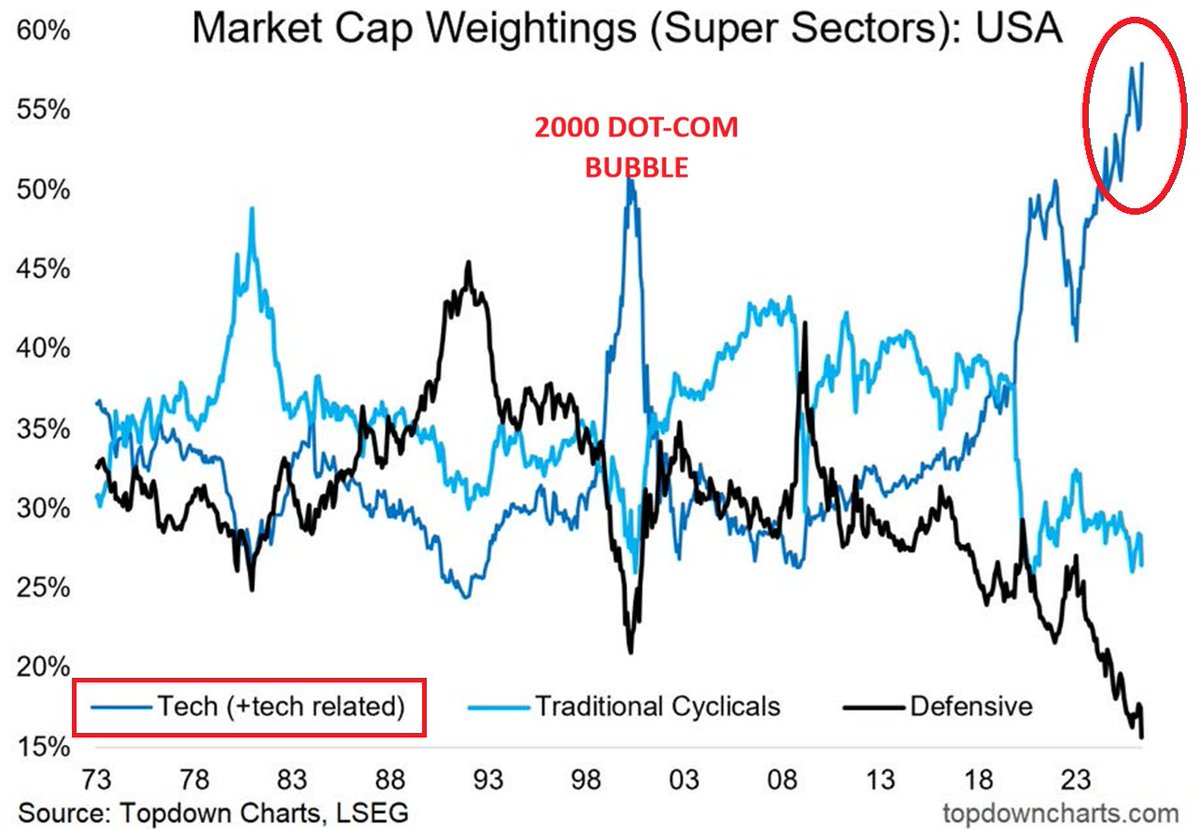

First, another look at the record overvaluation in tech and tech-related companies (dark blue below via topdowncharts.com) versus the S&P 500 traditional cyclicals (light blue) and defensive sectors (black) since 1973. Again, the conclusion here is not that traditional and defensive stocks are cheap but rather that tech and tech-related sectors have never been so inflated. This makes the entire index and all the portfolios that track it the most vulnerable to mean-reversion losses in at least 53 years.

Fresh highs in stock market indices (S&P 500 shown below in dark green) have opened a glaring gap between “Wall Street” sentiment and the University of Michigan Consumer Sentiment Index (red below) since 2024. Finance is supposed to be a service that supports and feeds off the real economy. When finance is euphoric, and its customers are depressed, something is fundamentally broken and unsustainable.

Current market conditions are so extreme that the masses believe they are normal and durable. Such assumptions have historically proven painful.

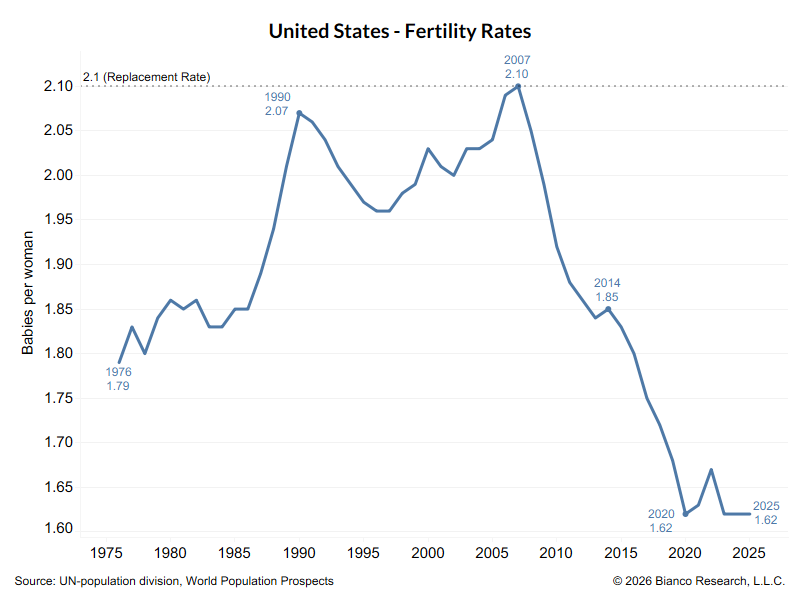

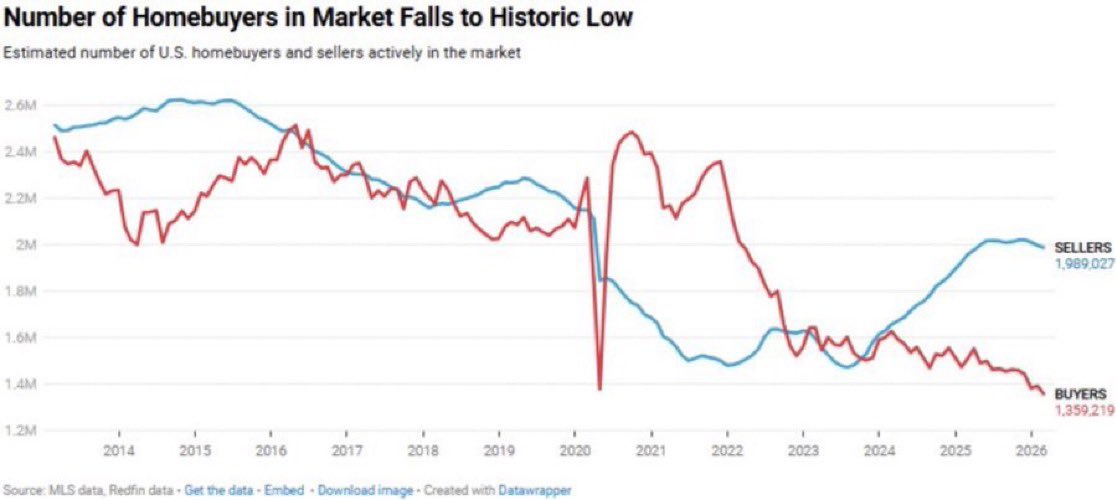

There is a reason that young people are unable to launch and fertility rates have plummeted. Since the tech wreck in 2000, governments and central banks have repeatedly bailed out the finance sector and asset prices at the expense of everything else. But in the end, a shrinking pool of customers is a recipe for stagnation and eventually deflation. Aging asset owners increasingly need buyers to cash them out. The widening spread between would-be buyers and would-be sellers suggests that transaction prices lie somewhere below the current ask.

Aging asset owners increasingly need buyers to cash them out. The widening spread between would-be buyers and would-be sellers suggests that transaction prices lie somewhere below the current ask.

The segment below offers a worthwhile macro update.

The segment below offers a worthwhile macro update.

DiMartino Booth with Competent Investor’s Tom Bodrovics: Warsh’s Fed Takeover-A Quiet Coup Brewing? Here is a direct video link.