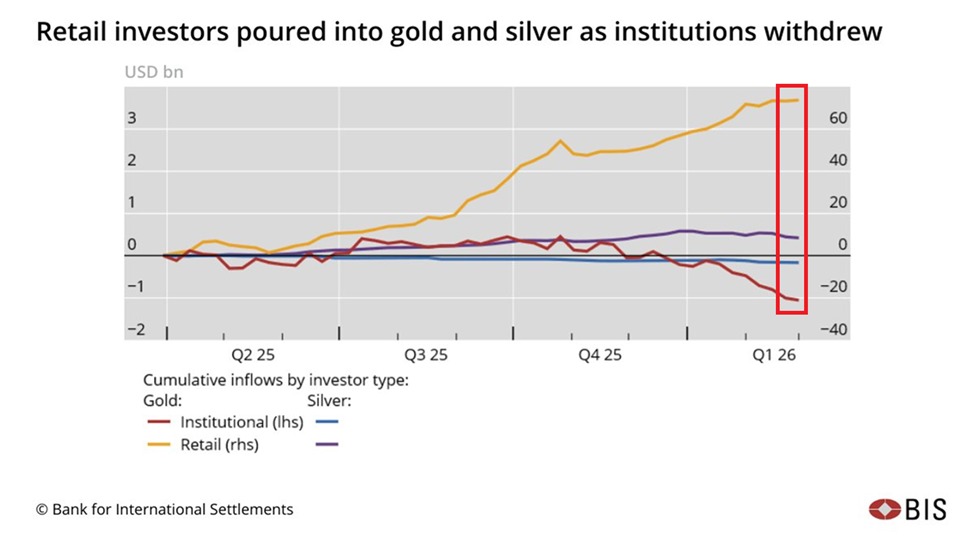

Crypto bounced alongside fossil fuel prices since the Iran war broke out on February 28 — though it’s still down 43% since October. Other global markets generally plunged along with metal prices (shown below, courtesy of The Daily Shot).

US and Canadian government bonds held up second best, with Canada’s 5-year Treasury price dropping 2.4% and the US 10-year Treasury price falling 3% as yields rose. Banks use these Treasury yields as a base for setting fixed interest rates, including the influential 5- and 30-year mortgage rates, which rose sharply in both countries.

Investors spent most of the first two months of 2026 stripping out rate-hike expectations — then, over just a few trading sessions, those bets came roaring back as conflict in Iran sparked.

Canadian bond traders were suddenly pricing for two more Bank of Canada hikes over the next 12 months if oil-driven inflation proves persistent. There are some reasons to take the under on that. Should they end up not hiking or even ‘unexpectedly’ cutting rates from here, the case for Treasury gains has rarely been stronger.

The US 10-year yield touched 4.4%, the highest since Trump’s “liberation day” tariff mayhem last spring, and the influential 30-year US fixed mortgage opened around 6.36% today, up from about 6% on February 26.

Suddenly, like last April, President Trump this morning retreated from scorched-earth rhetoric, posting that Iran peace talks (that had not been announced) were going well: “I AM PLEASE TO REPORT THAT THE UNITED STATES OF AMERICA, AND THE COUNTRY OF IRAN, HAVE HAD, OVER THE LAST TWO DAYS, VERY GOOD AND PRODUCTIVE CONVERSATIONS REGARDING A COMPLETE AND TOTAL RESOLUTION OF OUR HOSTILITIES IN THE MIDDLE EAST.”

Other agencies have suggested that no such talks have taken place. Who knows what is true? See Trump tells CNBC, ‘we are very intent on making a deal’ with Iran.

Perhaps Trump’s objective was to buy some rate relief; Treasury yields have fallen sharply, easing rate pressure in the process. Stocks have also bounced, while fossil fuel prices are plunging.

What we know for sure is that the S&P 500 closed decisively below its 50-day moving average on Friday (shown below since October 2023, courtesy of my partner Cory Venable).

Canada’s TSX did the same (below, since October 2024, courtesy of Cory Venable), despite a 16% weighting in the fossil fuel sector.

Canada’s TSX did the same (below, since October 2024, courtesy of Cory Venable), despite a 16% weighting in the fossil fuel sector.

Over the past year, rising asset prices were one of the only things the economy had going for it. Now, bearish trends have reclaimed stocks (joining private credit), and the 50-day (green line) serves as overhead resistance to be tested on rebounds.

Over the past year, rising asset prices were one of the only things the economy had going for it. Now, bearish trends have reclaimed stocks (joining private credit), and the 50-day (green line) serves as overhead resistance to be tested on rebounds.

Fears of the unknown drive volatility, but the likelihood of inflation remaining elevated and central banks hiking rather than cutting, ultimately depends on whether an external shock like oil prices causes workers to secure higher wages to maintain their purchasing power (like they ultimately did in COVID). Higher labour costs could then pass through to higher prices for goods and services, which in turn leads workers to demand even higher wages, and the cycle continues to feed itself.

But today, we have the weakest labour markets in years. The US unemployment rate is 4.4% as of February 2026, with approximately 7.6 million people unemployed. There were 6% more unemployed people than job openings in the latest data.

The labour force participation rate slipped to 62% in February, its lowest level since December 2021. Long-term unemployment also rose, with the average duration of unemployment hitting 25.7 weeks — the longest since December 2021.

In Canada, the official unemployment rate is 6.7% as of February 2026, up from 6.5% in January. Canada lost 84,000 jobs in February (before the oil shock), one of the worst monthly job losses in years outside the pandemic.

The current 64.9% labour force participation rate is at that long-run average, but has been drifting lower as population growth slows, younger workers struggle to find jobs, and discouraged workers exit the labour force. Canada’s unemployment rate is arguably worse than the headline number suggests, since some of the “improvement” in unemployment comes from people no longer looking for work rather than actually finding jobs.

And then, of course, we have recently announced government layoffs, the growing use of Artificial Intelligence to replace human workers, and economic drag from falling home prices amid the weakest real estate market in decades, and still record unaffordability. The Bank of Canada admitted last week that it had underestimated the weakness in real estate and would need to downgrade its January economic outlook accordingly.

With consumer sentiment moribund, debt levels high, and President Trump’s approval rating low, there’s little tolerance for rising fuel costs and interest rates. To improve conditions, they will need to end policy mayhem and succeed in re-anchoring inflation expectations. With a mid-term election in less than 8 months, the stakes to ease financial strain could not be higher.

With Canadian housing in the fourth year of its worst downturn since 1980, the desire for lower Canadian interest rates has rarely been more urgent.

The agenda for fiscal and monetary policymakers is clear: reduce the cost of living and coax interest rates lower. Not a quick or easy feat, but job number one.