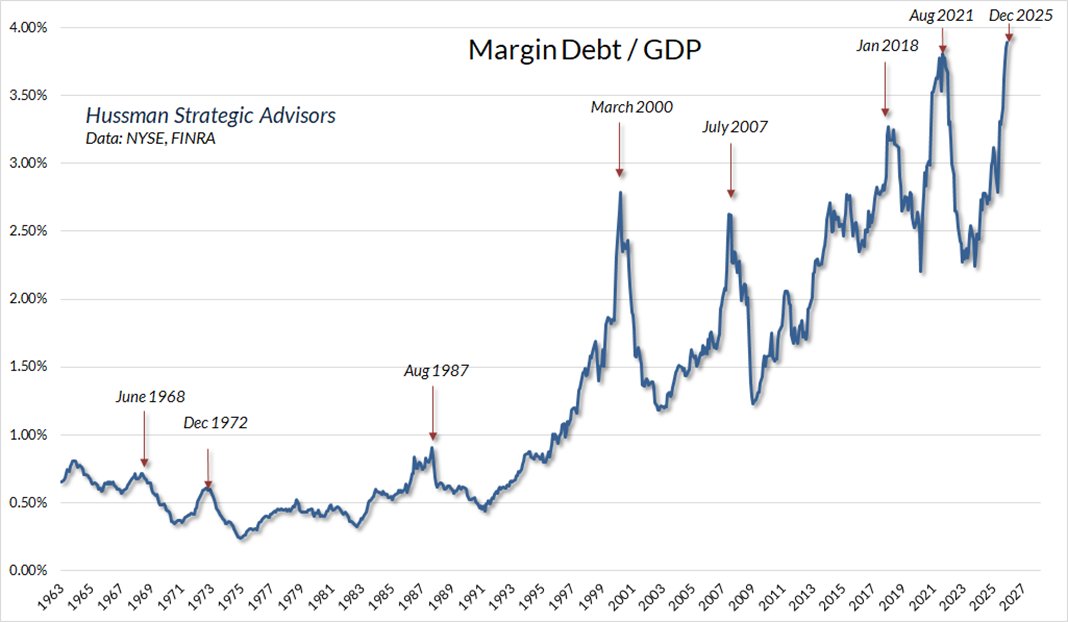

At some point in every cycle, bullshit stops baffling brains, and blind faith is beaten into submission. Revelation is making some progress in a few areas; see “Investors See Big Losses From President’s Brand.” To wit:

Shares of Trump Media & Technology Group, which operates the president’s Truth Social platform, have tumbled 75% since Trump’s inauguration. Digital “meme coins” named for Trump and first lady Melania Trump are down 86% and 99% since inauguration day, respectively. One of the Trump family’s crypto ventures, a token called World Liberty Financial, has dropped roughly 40% since its September launch.

At the same time, Goldman Sachs’ basket of unprofitable technology companies, which had surged early in 2025, has plunged by more than 20% since the mid-October peak.

Nearly $1 billion in leveraged crypto positions have been liquidated during another sharp price drop, bringing fresh momentum to a sector-wide dash for cash. Bitcoin (below since 2023) has tumbled 32% since October 6; see ‘Stock Rally Takes a Break as Crypto World Gets Hit.’

Still, speculative hopes are riding on a Trump ‘yes’ man being named to head the Fed in May 2026, in the presumption that easier monetary policy will keep asset bubbles growing a while longer. Irrational behaviour is admittedly a wildcard. But every bubble ends in a bust — there are no exceptions.

Still, speculative hopes are riding on a Trump ‘yes’ man being named to head the Fed in May 2026, in the presumption that easier monetary policy will keep asset bubbles growing a while longer. Irrational behaviour is admittedly a wildcard. But every bubble ends in a bust — there are no exceptions.

As always, individuals must make risk management decisions and live with consequences.

Charles Mackay’s timeless quote from Extraordinary Popular Delusions and the Madness of Crowds (1841) comes to mind:

“People, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.”

There’s a reason that Mackay’s book has never been out of print since it was published 185 years ago.