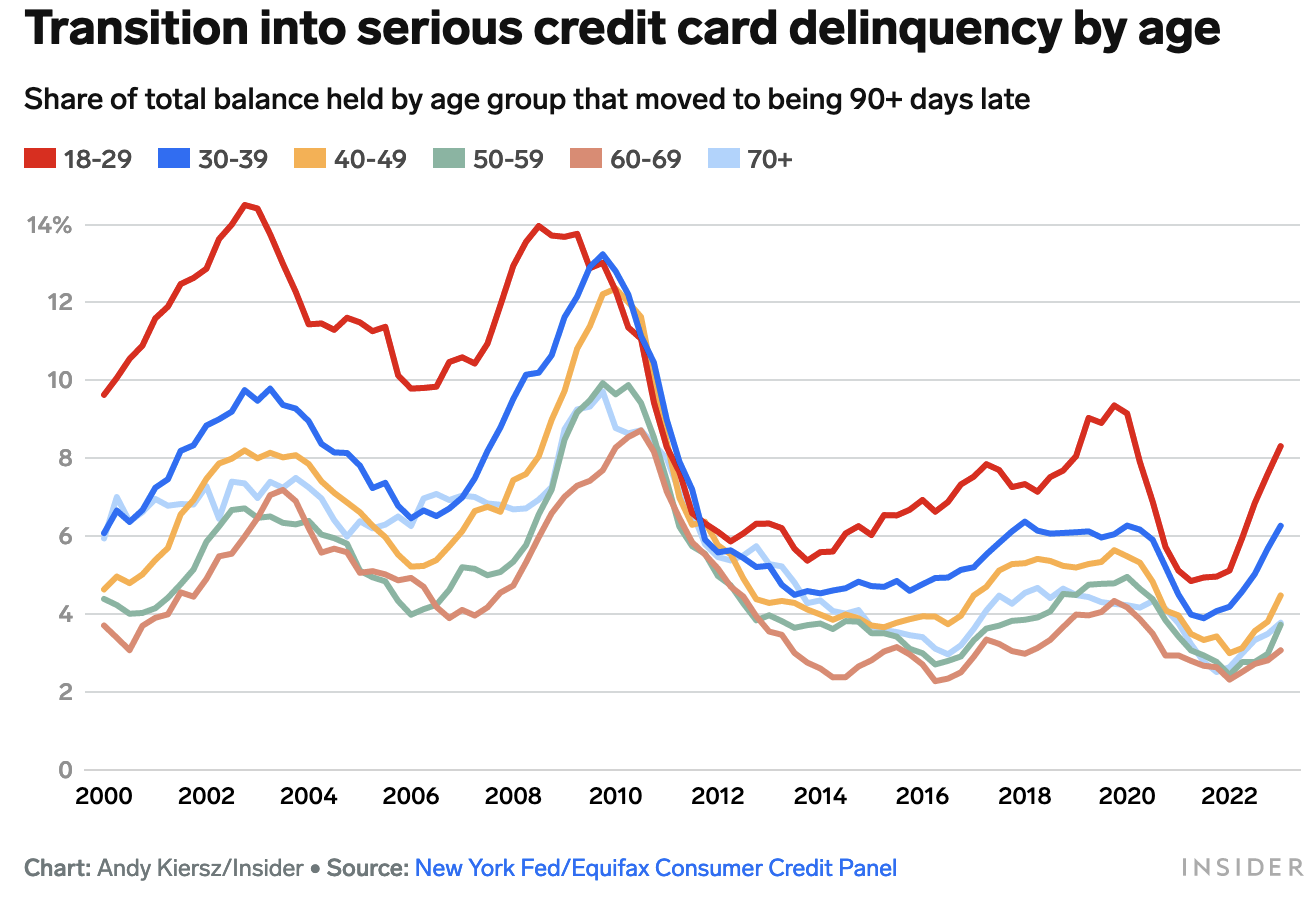

Historically it has been typical at the beginning of real-estate downturns for listings to decline as owners try and extend loans rather than sell properties at lower prices. That has happened over the past year with residential and commercial properties. At first, this suppresses inventory for sale and reduces price discovery, stalling the clearing process.

In the first quarter of 2023, investors purchased just $10.7 billion of office property, down 68% from last year (MSCI Real Assets data).

There’s a reason that real estate downcycles tend to take 4 to 6 years to bottom. In the next phase of the downturn, cash-strapped owners cut their losses and list properties to reduce overhead and raise cash. That’s starting now; see Rise in Distressed Sales Signals New Chapter For Beleaguered Office Market:

In recent weeks, Blackstone sold the Griffin Towers office complex in Santa Ana for $82 million, or about 36% less than the firm paid in 2014, say people familiar with the matter. Principal Financial Group sold a Parsippany, N.J., office building for $14.3 million, down from the $52 million it paid in 2008, according to participants in the sale.

The tower at 350 California in San Francisco, valued at $300 million in 2019, is expected to trade at about $60 million, or roughly 80% below that previous valuation.

Office building values have steadily declined during the pandemic as shifting workplace strategies reduced demand for space and vacancies rose. Higher interest rates have also hammered the sector, making it much more difficult for landlords to refinance a property or fund the building improvements and amenities needed to attract tenants.

Someone told me last week that they are holding their real estate investment trusts (REITs) and mortgage funds because they don’t think a downturn in the physical property market will much impact them. That is wishful thinking, to be sure, but not historically supported.

So far, stocks in the US real estate sector are down about 28% from their cycle peak in 2022, and the Canadian Real Estate Investment Trust (XRE) is off 21.7%. A favourable outcome would be a 50% drop for these overvalued, widely-held securities from peak to trough.

As property listings pick up, price pressure intensifies, and public and private investment funds increasingly mark their values down to market–something they have not had to do for a decade.