The speakers take a few minutes to turn on their cameras in this segment, but they get there, and ECRI’s economic cycle update is always worth a listen. Big picture context is useful in avoiding common financial mistakes.

Lakshman Achuthan is being interviewed by Dale Pinkert during the F.A.C.E. webinar. Lakshman is calling the pullback in inflation ,”The Immaculate Disinflation. He is still expecting a hard landing from late June’s forecast. Here is a direct video link.

Independent economist A. Gary Shilling also writes a monthly Insight letter for subscribers only, but his latest update was summarized in a free article available here.

Shilling expects a 40% drop from the S&P 500′s peak in January 2022, with the bulk of the decline to come in 2023 as an unfolding recession decimates corporate earnings:

“With hope springing eternal, many equity investors continue to believe that a recession, or at least another leg down in the equity bear market, will be avoided. That’s despite the Fed’s continual statements that it is resolved to kill inflation … regardless of the negative consequences for the economy.”

Posted inMain Page|Comments Off on Hard landing in motion

Our coverage of the VRIC continues with a discussion about the U.S. dollar, and it’s status as a reserve currency, including the role gold plays in protecting wealth and how the dollar’s dominance affects the broader market. Brent Johnson, Danielle Park, Grant Williams, and Russell Gray give their opinions on what is often a hotly contested topic. Here is a direct video link.

Further to comments in the panel discussion about gold outperforming in currencies other than the US dollar, the argument remains rather specious. Things like physical and mental strength, shelter, food, water, a vehicle, a supply of fuel, and medicine all have immediate utility in their own right. Things not used in the present can be stored for future needs or wants. How well something works as a store of value depends on its utility between when it is stored and when it is used.

If a store of value pays an income or reduces expenses for its owner during a holding period, that goes in the benefit column. If it costs to store or hold the item, that’s a negative. In the case of something like gold and other financial assets, the value also depends on whether and in what ratio they can be converted or traded for other items when desired.

Changes in value for the owner will always be a combination of changes in the asset’s market price plus changes in the currency it is priced relative to the currency of one’s spending and needs. It is pretty irrelevant to a Canadian or a European that an asset may have risen in yen unless they have expenses, spending or wants for which they need yen.

As mentioned in my comments on the panel, most assets of international exchange are traded in US dollars. In other words, to get a relative picture of how well a US-denominated asset stored value, one needs to separate the change in its price from the change in its currency exchange relative to one’s home currency. If a US-denominated asset like gold rose in total value by 10% over a particular holding period, while the dollar rose 12% relative to one’s home currency, then we would have fared 2% better holding just US cash rather than gold. And on a risk-adjusted basis, the gold was less liquid (it required a sale and a currency conversion to be useful for our needs) and so came with greater risk and less return.

Over the last decade, the price of gold in U$ appreciated by 3.99% overall and 39.68% relative to the Canadian dollar, but 34.5% of that gain came from the greenback’s appreciation against the loonie. In other words, over ten years, Canadians picked up a gross of 5.18% in notional net benefit by holding gold versus just holding US cash–not an attractive risk-reward equation. However, those who see gold as a form of insurance feel the cost of insurance is justified. And that is ok with me.

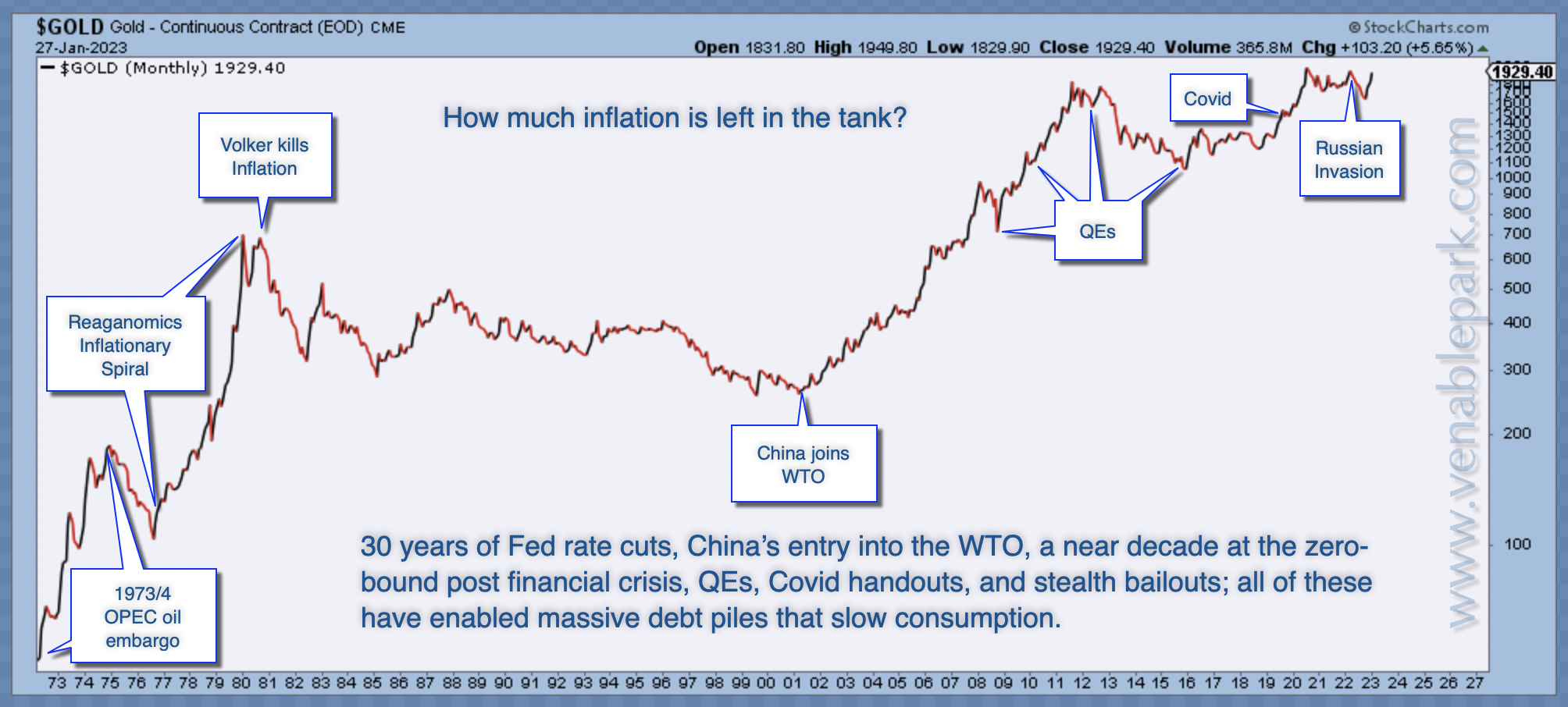

My partner Cory Venable’s chart below shows gold’s price change in US dollars since 1972 and highlights some of the drivers I mentioned in the panel discussion. If inflationary and monetary impulses continue to deflate for the next little while, gold may too.

Posted inMain Page|Comments Off on VRIC: Stocks, gold and the dollar

The US Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) is used by monetary policymakers to gauge credit conditions. Over the past year, banks have reported tighter lending standards on commercial loans to small, large and middle-market firms (blue bars below since 1990, courtesy of The Daily Shot). This indicator has traditionally led US corporate defaults by three months (light blue below) and suggests rising payment defaults from here.

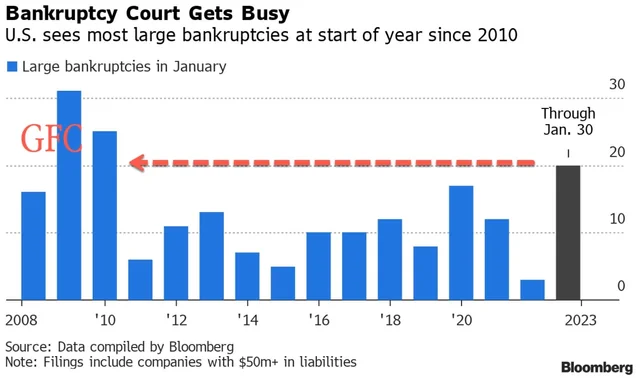

Already (as shown below) through the end of January, large corporate bankruptcies (companies with more than $50 million in debt) have spiked the most since the 2008 financial crisis.

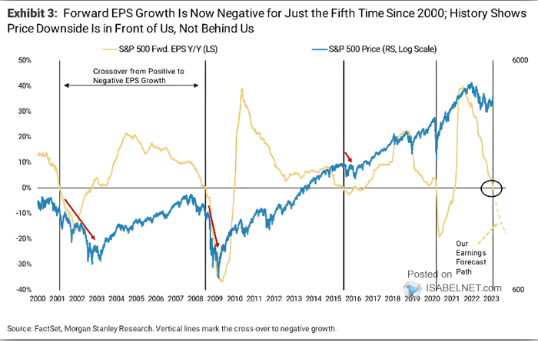

Coming into 2023, forward S&P 500 earnings per share (EPS) growth has turned negative for the fifth time since 2000 (shown below in yellow, courtesy of ISABELNET.com), and the downtrend is forecast to continue (dotted line). Stock prices have always followed EPS lower (S&P 500 in blue), with the bulk of bear market losses happening after the earnings trend crosses from positive to negative (black lines below).

For all the people talking about low unemployment rates being bullish for economic growth and equity markets, the truth is that the unemployment rate (lower line below since 1950) is the most lagging of indicators and has always been lowest at the start of recessions (grey bars below, aka the end of each economic expansion phase). Stock valuations (S&P 500 price-to-earnings ratio is the top line below) typically tumble during recessions as the unemployment rate spikes.

Today, the most historically reliable leading indicators suggest a near certainty of recession within the next 12 months (US 3m-10-year curve is at 100%, far right bar below). The riskiest assets, meanwhile, like junk bonds (HY credit circled below), most commodities (copper below) and stocks, remain in denial, still broadly over-valued.

Highly leveraged financial markets have been trained to hang hope on endless bailouts from central banks. But the economy is the big dog that wags the tail of spending, capital investment, jobs, revenue, and ultimately earnings, not central banks. Moreover, today the US Fed is still tightening financial conditions with monthly QT and possibly more rate hikes. When they move to loosen credit conditions again, it will take many months for the easing efforts to disseminate. A lot of distressed selling is due to occur before then.

Posted inMain Page|Comments Off on The financial noose tightens

“An explosive critique about the investment industry: provocative and well worth reading.”

Financial Post

“Juggling Dynamite, #1 pick for best new books about money and markets.”

Money Sense

“Park manages to not only explain finances well for the average person, she also manages to entertain and educate while cutting through the clutter of information she knows every investor faces.”

Toronto Sun