As I have noted many times, historically, a maximum of 3x household income has been considered the limit of what is considered “affordable” for homes. In Canada, with a median household income of 84k, this would mean homes priced at no more than $252,000. Today, the national average home sale price is $660k (down from $ 852k in February 2022), but it is still about 8x the median household income.

In 1991, our first family home cost 2x our household income, and the same 2x ratio held as we upscaled to our second and third family homes in 1996 and 2000.

Today, in the Greater Toronto and Vancouver areas, the average home sale price is in the $900K to $1.1M range (about 10 times the median household income). In the Prairies and Atlantic regions, the median home sale price has been in the $300K to $500K range, roughly 4 to 8 times the median household incomes of $75K and $65K, respectively.

The good news is that prices are finally coming down, and so are rents. See Condo crash pushes down Toronto asking rents to $2,500 a month due to ‘sheer volume of supply’.

The bad news for existing homeowners, investors and lenders is that lower rents pencil to lower home prices and significantly more downside is needed before bubble pricing is mean-reverted once more; see More Toronto condos are selling in the $300,000s as prices finally become (slightly) more affordable:

It’s not just condos experiencing price dips, but the entire market from detached homes to micro units. In January, the average selling prices for all home types in the GTA was $973,000 — the first time prices fell below $1 million in five years. The feeding frenzy of the pandemic, which saw over-leveraged buyers jump into the market and speculators push prices to their limits, is gone. Sales hit their lowest number in 25 years, and prices are down 27 per cent from the February 2022 peak.

A growing share of single-family homes are popping up in the market for under $1 million, and an increasing number of condos are selling for less than $500,000.

These properties act as an appealing entry point for first-time homebuyers looking to get into the market at prices not seen in years, and for those outside the GTA who have returned to the office and want a pied-à-terre in the city to cut down on long commutes. They’re also attractive to buyers simply looking for a long-term investment — though experts warn economic challenges will continue to dampen consumer confidence, hindering potential price or sales growth in the year ahead.

A pickup in mortgage defaults and foreclosures is part of the process, as it forces price discovery and inevitably reduces comparables for other properties.

John Pasalis, president of Realosophy Realty Inc., talks to Financial Post’s Larysa Harapyn about how many financially stressed homeowners facing higher mortgage rates and lower home prices are running out of options. Here is a direct video link.

Similar trends are spreading across many U.S. markets as well.

Houses are starting to cheap in some U.S. cities as we enter the 2026 housing market. This house in Houston, TX is a 4×2, move-in ready, and on the market for $204,000. It’s being sold by an investor. Access housing market forecasts and data on Reventure App: https://www.reventure.app In the surrounding neighborhood, rental signs dot the landscape as inventory across the Texas housing market surges in 2026. Landlords are heading for the exits, and could soon be forced to stop buying if the Trump administration moves forward with the investor ban. Homebuyers, agents, and investors should expect a deflationary housing market environment across the South and West Coast of the U.S. in 2026. Inventory has stacked up, there’s plenty of homes for sale, and buyers are not coming back – because it is simply too expensive. Another headwind building for the housing market is with immigration. We could be coming off the lowest immigration levels ever in 2025 – suggesting that landlords and Wall Street investors could face issues in their properties. In this community in Houston, over 50 houses were for rent when I toured. Here is a direct video link.

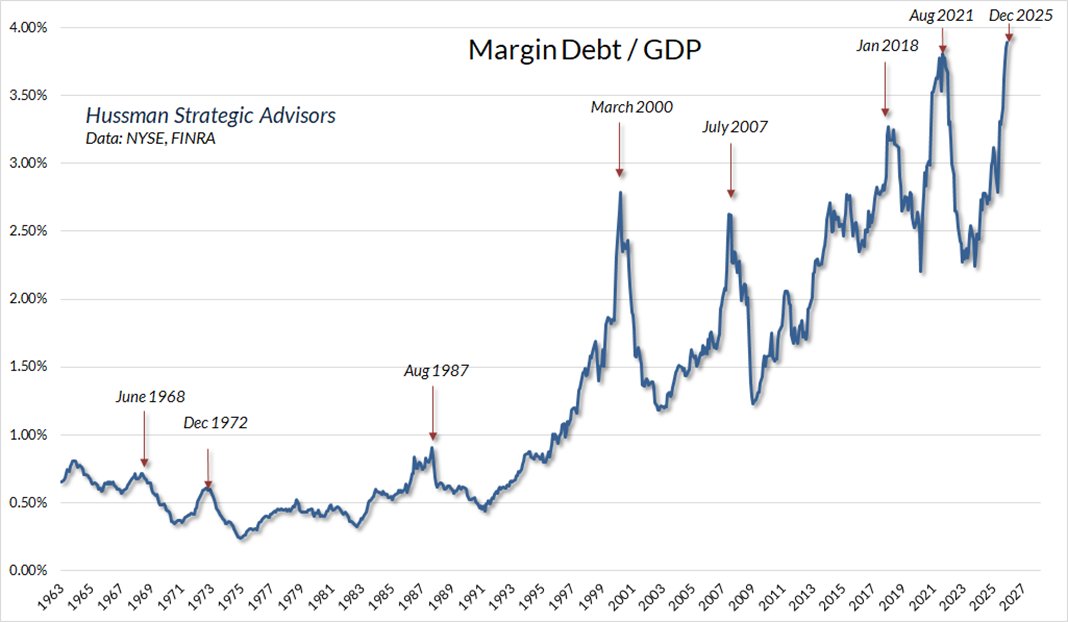

U.S. stocks account for approximately 63% of global equity market capitalization, the highest since the 1966 secular bubble top, after which equity markets entered a secular bear period that lasted until 1982 (shown below since 1900).

U.S. stocks account for approximately 63% of global equity market capitalization, the highest since the 1966 secular bubble top, after which equity markets entered a secular bear period that lasted until 1982 (shown below since 1900).