Our month-end letter for January discusses the links between private equity, private credit and elevated financial risks for the rest of us. The segment below offers a primer. Opacity and complexity in financial products often cloak elevated risk and even deceit.

Private credit, a form of lending by non-bank financial institutions to businesses outside of public markets, was once a niche corner of Wall Street. Now, private credit is going mainstream as it seeks funding from retail investors. CNBC’s Hugh Son breaks down the rise of private credit, why retail investors are looking into private credit and the risks and upsides of investing in the space. Here is a direct video link.

Posted inMain Page|Comments Off on Why Private Credit Wants You to Buy In

Empirical research suggests that expanded gambling access—particularly low-friction, online sports betting—has been associated with measurable increases in consumer financial distress, including higher bankruptcy filings in U.S. states following legalization.

The evidence is strongest where gambling becomes more accessible and continuous, rather than episodic (e.g., mobile wagering versus destination casinos).

At the individual level, a robust body of clinical and public-health research in both the U.S. and Canada links problem gambling to sharply elevated risks of depression, financial collapse, suicide, family trauma and violence.

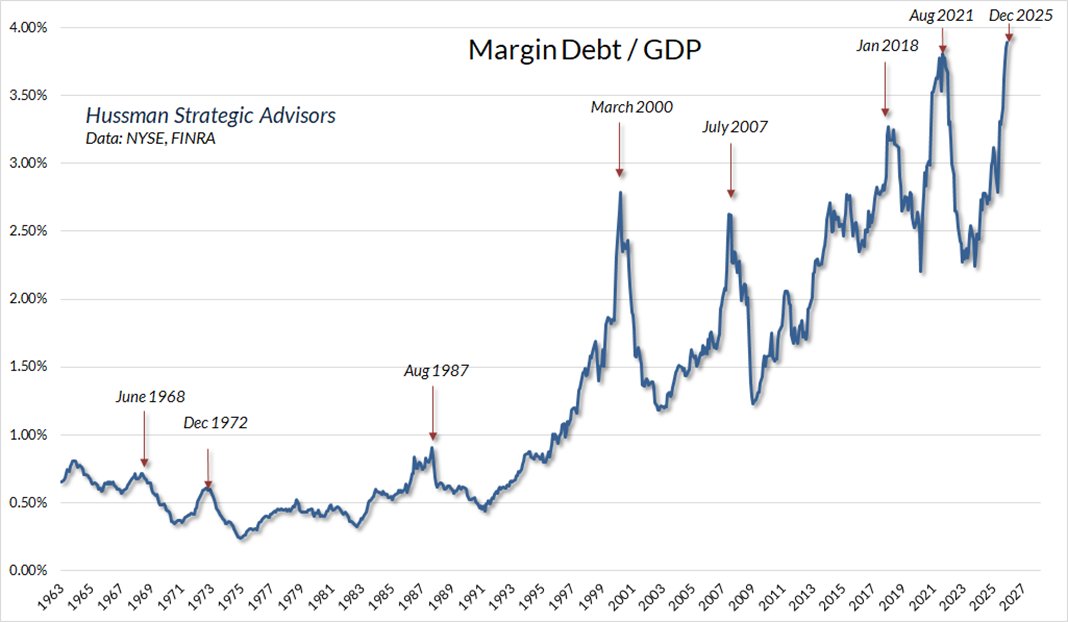

A growing body of behavioural finance and public-health research suggests that gambling activity can bleed into financial market behaviour, particularly where trading becomes fast, leveraged, and game-like.

Studies show that individuals who engage in gambling are more likely to trade frequently, concentrate risk, pursue lottery-like payoffs, and persist in loss-chasing behaviours when investing.

The expansion of zero-commission trading, options access, crypto assets, and 24-hour markets has lowered the psychological barrier between wagering and investing, blurring the distinction for some participants. While long-term capital allocation and disciplined portfolio management remain fundamentally different from gambling, periods of speculative excess often coincide with an influx of behaviorally driven capital whose decision-making resembles gambling more than investing, amplifying volatility, mispricing, and eventual drawdowns.

In June 2022, Canada’s Cullen Commission concluded that weak oversight of casinos in British Columbia enabled widespread money laundering by organized crime, with clear links to broader financial crime and asset inflation, including ballooning home prices.

The findings highlighted regulatory failure, institutional incentives that discouraged enforcement, and the risks that arise when high-cash industries expand faster than supervision.

The inquiry stands as one of the most comprehensive confirmations in Canada that gambling venues, when inadequately controlled, can become conduits for crime and financial corruption.

A large majority of the Commission’s 101 recommendations have not yet been fully implemented. Major structural reforms, including a dedicated provincial Anti-money laundering (AML) commissioner, broader regulatory and reporting frameworks, and enhanced federal-provincial cooperation, remain in progress or under debate rather than fully enacted. In the meantime, online gambling has become ubiquitous.

Far-reaching, worthwhile discussion in this segment.

On episode 226 of The Compound and Friends, Michael Batnick and Downtown Josh Brown are joined by Jeremy Grantham to discuss: stock market bubbles, the ups and downs of managing money, how the wealth divide has grown so wide, the future of clean energy tech, and much more! Here is a direct video link.

Posted inMain Page|Comments Off on Grantham reflects on six decades of investing

“An explosive critique about the investment industry: provocative and well worth reading.”

Financial Post

“Juggling Dynamite, #1 pick for best new books about money and markets.”

Money Sense

“Park manages to not only explain finances well for the average person, she also manages to entertain and educate while cutting through the clutter of information she knows every investor faces.”

Toronto Sun