So US GDP contracted at a 2.9% annualized real rate in Q1 2014, a full 3% lower than had been originally guesstimated in April, as spending fell across pretty much every component of consumer, business, government and net exports. (Although, we should remember that even this final estimate will continue to be revised in retrospect by NBER over the next couple of years, and the historical revision bias has always been for lower, not higher numbers). So far, this is the biggest downward revision to initial forecasts since the data began being recorded in 1976. Also worth noting perhaps, US GDP quarterly declines at an annualized rate of more than 1.5% have never happened except during or leading into NBER-declared recessions since 1947.

Real world data like low labor participation, stagnant wages, anemic savings and still climbing debt levels all seem to corroborate the recessionary tone in GDP. So do things like shipping rates which have fallen 60% over the past 6 months, and are now vying for the lows reached in the recession of 2008. Bond yields too are putting up no argument, with the US 10 year treasury yield in the 2.55% range today, down from 3% at the start of the year.

Yet if you listen to the mainstream financial commentators who make high fees off of other people’s money when it is placed in the highest risk products that go up with the stock market–(and yes plunge with the stock market, but they will explain how that is not their fault when the lawsuits come…)–apparently we are only just started into a secular bull run which is set to continue for many more years from here. Wow! The evidence offered: “why stocks have gone straight up for nearly 2 years don’t you know! What in the world could ever cause them to do otherwise?”

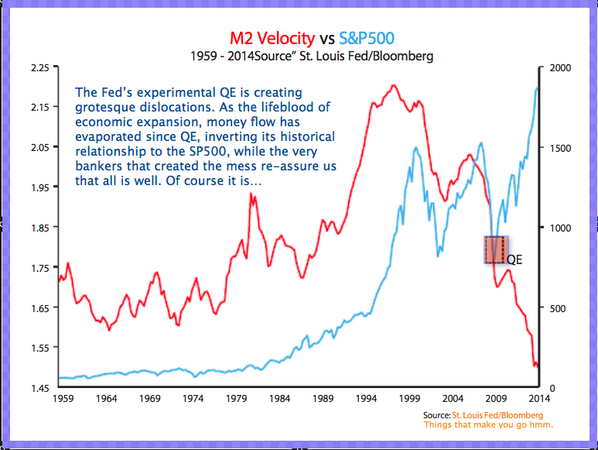

Which brings us to this little picture here plotting the S&P 500 nominal price moves (in blue) and US money velocity (in red) since 1959…and of particular note, since the Fed began flooding banks with trillions in liquidity via QE over the past 4 years. All looking perfectly sustainable and stable here, right? At any moment, money velocity is certain to reverse course and surge into the real economy driving credit into investment and growth through the roof to catch up with those jubilant stock prices and drive them higher still!? (The alternative–that correlations will restore via a collapse in stock prices back in line with nearly dead velocity is not worth considering right?)

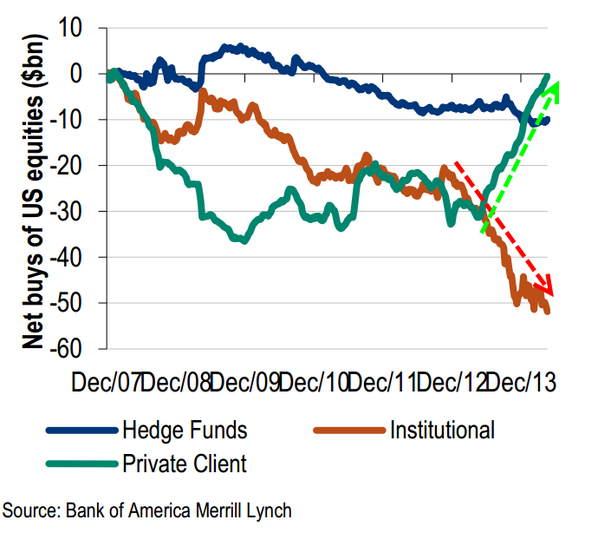

There is no question that the human appetite to gamble rises in lock step with price and capital risk. And since the official goal has been to buy banks time and quick profits while sacrificing enticing what’s left of all the “little people” out into a capital blizzard without guide-ropes, the next chart proves that the strategy has been working beautifully the past 2 years. Alas, poor Yorick! I knew him…