The theory of diversification is undermined in practice when it comes to the Canadian equity market. As graphed below, today the widely bench-marked TSX 60 Index mirrored by most equity funds and asset allocators, is in fact a whopping 61% concentration in the financial and energy sectors.

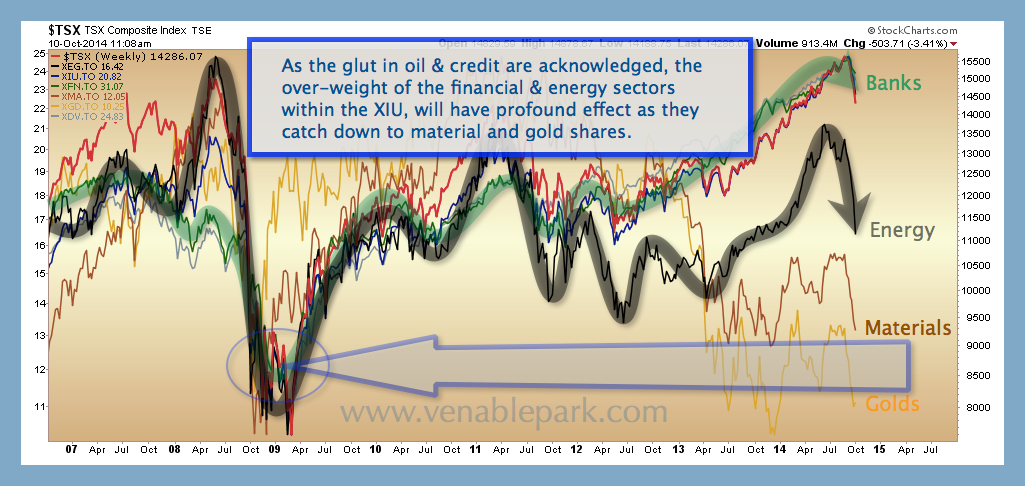

The following chart maps the price performance since 2007 of the broad TSX Composite, TSX 60, dividend paying Index (XDV), financial index (XFN) (all 3 clustered under green arrow at top of chart), energy index (XEG), materials (XMA) and gold companies (XGD) (as marked).

The following chart maps the price performance since 2007 of the broad TSX Composite, TSX 60, dividend paying Index (XDV), financial index (XFN) (all 3 clustered under green arrow at top of chart), energy index (XEG), materials (XMA) and gold companies (XGD) (as marked).

Over 2 years of QE’ mania up to July of this year, dividend-paying share prices went full nut job. Financial shares (conservative??) surged +100% in 24 months alone as Canadian households moved to DEFCON 1 in indebtedness. At the same time, the materials and metals sectors have continued to mean revert along with falling global demand since 2010. Since April, energy shares resumed following the real economy lower as all three sectors look to their 2009 lows as potential support.

Over 2 years of QE’ mania up to July of this year, dividend-paying share prices went full nut job. Financial shares (conservative??) surged +100% in 24 months alone as Canadian households moved to DEFCON 1 in indebtedness. At the same time, the materials and metals sectors have continued to mean revert along with falling global demand since 2010. Since April, energy shares resumed following the real economy lower as all three sectors look to their 2009 lows as potential support.

The bad news for those holding Canadian equity funds and traditionally allocated portfolios today, is that as QE delirium wears off, financial and dividend-paying stocks are likely to recouple once more with the economy-driving–metals-minerals and mining–sectors.

Consider that at decline of 50% in dividend paying stocks would just take them back to their 2012 levels and translate to about -30% for the TSX Index overall. To revisit their 2009 lows would mean losses for these widely touted ‘conservative dividend paying investments’ of about –70% and a broad market decline to about 8000–some -45% from present levels.

It is long past time for complacent holders to review their risk exposure.