The film “Pay it forward”(2000) is about how thoughtful acts in the present can yield a cascade of compounding benefits for the future, when recipients ‘pay forward’ the kindness they receive by helping others. It should be obvious by now, that the successive desperate monetary interventions from global bankers the past few years, have in fact done the opposite of this. By relentlessly trying to ‘stimulate’ ever-escalating demand through the use of excessive debt, bankers have in fact earned the world a financial future that keeps arriving increasingly weakened, year after year.

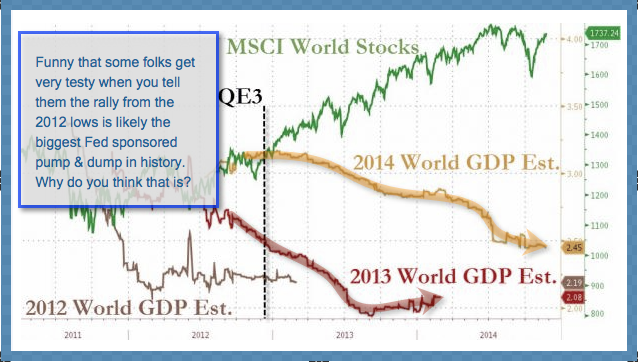

Each short-term focused, self-interested action has ‘spent’ years of future potential growth and recovery. Global GDP sinks lower each year (see below) on near-zero yields, wasting capital, and financial assets pumped to unsustainable levels on leverage (in green). This cartoon from China Daily showing the world economy faltering under the weight of QE oppression, captures the dynamics perfectly.

This cartoon from China Daily showing the world economy faltering under the weight of QE oppression, captures the dynamics perfectly.

John Hussman today explains it well in the quote below. Far from an encouraging sign, the obsessive compulsion of global bankers for more and more QE, only underlines the increasing desperation of these bubble-makers–out of ideas, and sensing their coming fall from grace. See: A most important distinction:

…the inclinations of central banks towards quantitative easing and interest rate suppression are increasingly taking on the tone of desperation in the face of accelerating economic weakness in Japan, Europe and China. While the stated objective is to increase inflation, low inflation isn’t really the economic problem–low growth, intolerable debt burdens, and mis-allocated capital are at the core of global challenges here. Unfortunately, QE only misallocates capital towards more speculation and low-quality debt (primarily junk and leveraged loan issuance), without much impact on real growth. China’s move was prompted in part by a surge in bad loans to the highest level in nearly a decade. The largest European banks now have gross-leverage ratios as high as 30-to-1 (during the credit crisis, one could order the sequence of defaults accurately using this metric, with Bear Stearns, Lehman, and Fannie Mae right at the top). But liquidity does not create solvency, and with credit spreads widening, the growing desperation of monetary authorities is a more negative signal than a positive one.”

One encouraging and historically consistent fact in all of this, is that excessive, short-term greed, eventually breeds its own end. And for that we shall be grateful.