“A system that works powerfully in one direction can work just as powerfully in the other.”

–Micheal Pettis, When do we decide that Europe must restructure much of its debt?

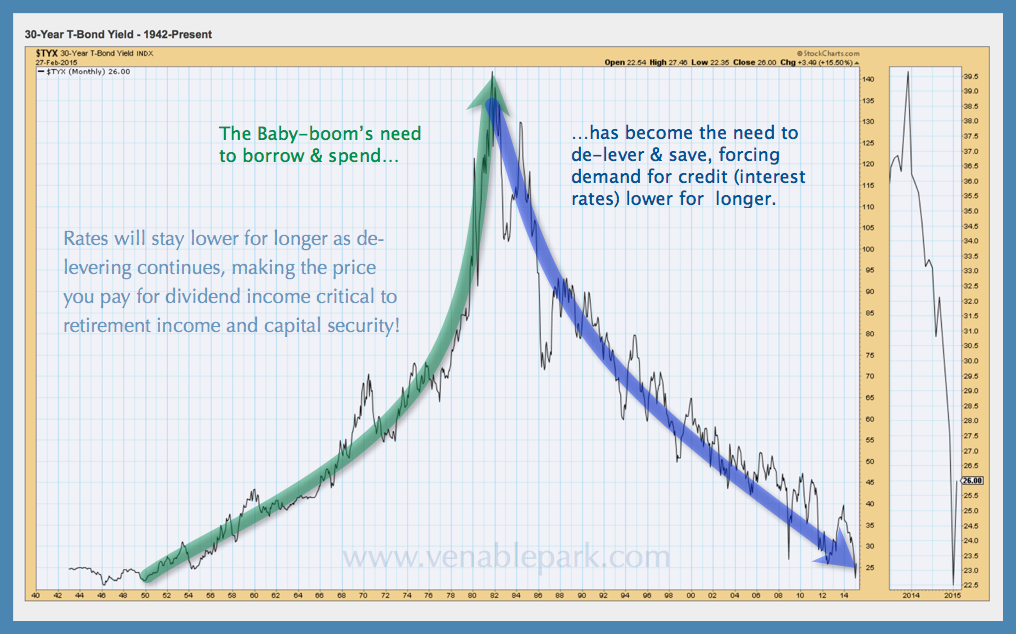

In late 2010 the global recovery out of the 2009 recession peaked and rolled over once more. Massive debts and aging demographics in the developed world, signaled demand would be weak for years and the world was awash in too much supply of everything except common sense. The debt boom that hocked future growth for present consumption as borrowing costs fell from 1980, in 2008, began a long and necessary payback period–equal and opposite in the other direction. This chart shows the 30 year rise in rates from 1950 to 1982 as the baby boomers moved through peak household formation years, and the reciprocal phase as rates fell with inflation thereafter–so far, 24 years and counting. Now fully retraced, rates have reached the zero bound, with only one way to go– up–eventually. In a slow growth world with more debt than ever before, rising rates will prove an impossible weight.

Not liking the necessary price deflation and slower growth now earned, central banks and politicians of the world have repeatedly flooded the banking system with excess (unnecessary) liquidity and ‘get out of jail free’ cards for the global banking cartel.

All of which has only helped to slow world demand further for longer, even while some asset markets have continued to rise on self-destructive financial leverage.

Today historically relevant valuation measures warn of a hideous opportunity set for capital held in assets inanely decoupled from the macroeconomic and corporate earnings trends on which they depend. The price risk, as charted here, is truly garish. Meaning, the coming opportunity for disciplined investors with a rule set, liquid capital and little leverage today, has rarely been as spectacular.

chart source: zerohedge.com

chart source: zerohedge.com