People who fail to appreciate how extreme the global re-leveraging cycle has been over the past 8 years, also underestimate the extremity of the default and asset repricing cycle now likely to follow. See The coming default wave is setting up to be the most painful:

Losses on bonds from defaulted companies are likely to be higher than in previous cycles, because U.S. issuers have more debt relative to their assets, according to Bank of America Corp. strategists. Those high levels of borrowings mean that if a company liquidates, the proceeds have to cover more liabilities.

“We’ve had more corporate debt than ever, and more leverage than ever, which increases the potential for greater pain,” said Edwin Tai, a senior portfolio manager for distressed investments at Newfleet Asset Management.

The interconnections here are global. Central bank inspired QE liquidity sloshing about global markets the past 6 years, have allowed companies that should have gone bankrupt in 2009-14 to extend and pretend by issuing even more debt. See Default Tsunami brewing.

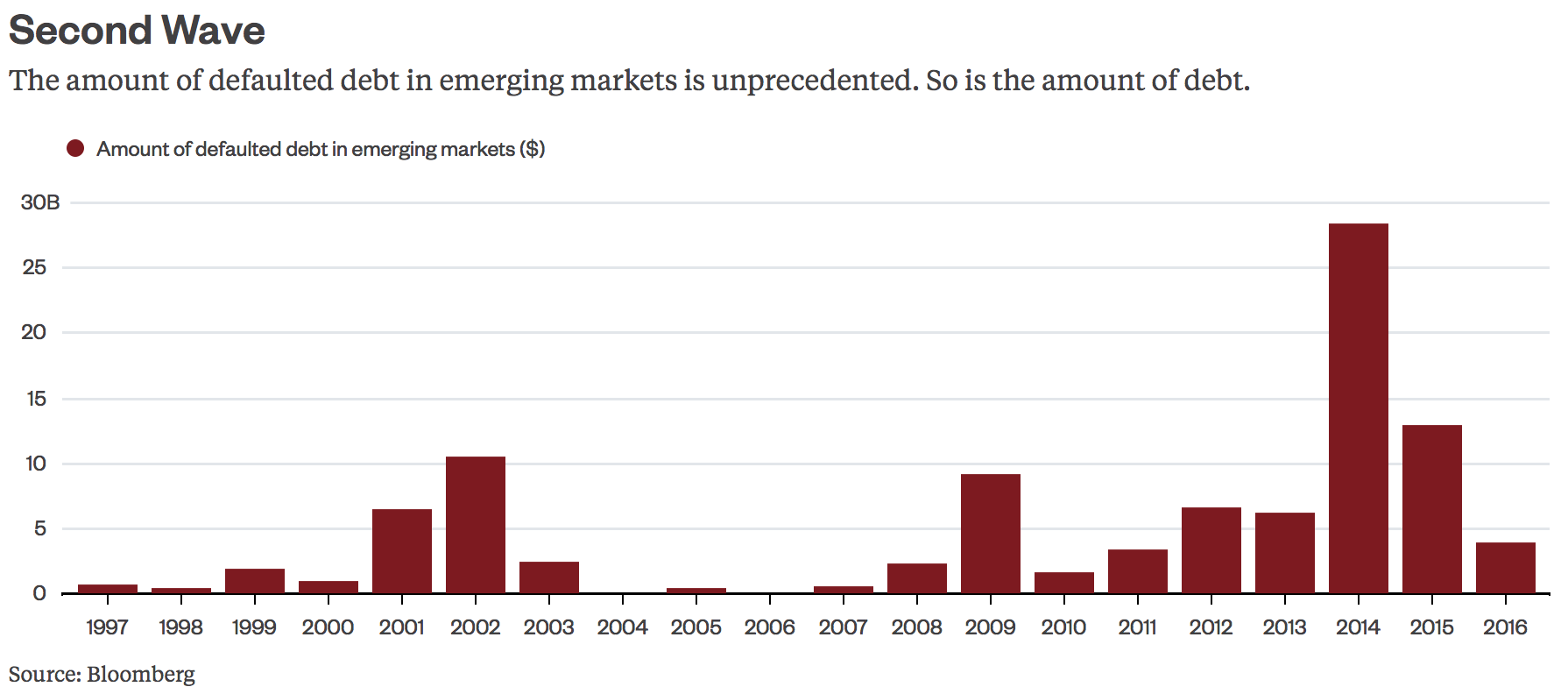

Worse, many emerging market companies were able to issue this debt in U$ to access lower interest rates. But the rising greenback since has served to greatly increase the weight of their repayment obligations.

Less than 4% in 2015, Moody’s says default rates could soar to as high as 14.9% by the end of the year and historically have reached as high as 22% in the 5 years following a credit crisis. In the process, corporate bondholders commonly lose 70% of their investment when a borrower goes bust. In this cycle, that figure could easily be higher.

The inevitable repricing of assets has been baked into reckless valuations over the past few years, and is likely to bring enormous opportunity for those who have been patiently waiting to buy corporate bonds once prices have been clubbed far below reason once more.