Fed Chair Yellen and her colleagues are fantasizing about ‘running the economy hot’. As if central banks at zero rates, had that kind of power.

The trouble is that a secular downturn in global demand–caused by debt hangover, years of malinvestment in non-productive assets, aging demographics and low yields–are thwarting hopes and dreams of inflation topping 2%+. This is not the good old days, when plain old cutting rates spurred more consumption. Today low yields are having the opposite effect–causing people to spend less and save more.

The bond sell off in the past month, has created another buying opportunity for the highest quality North American credits (ie., government issues 1-10 years). The same cannot be said for corporate debt, where credit risk is likely to spike as the economy and sales weaken further, and an increasing number of over-levered, unprepared companies struggle to stay in the black. At least governments can increase taxes when times get tough, companies don’t have that option.

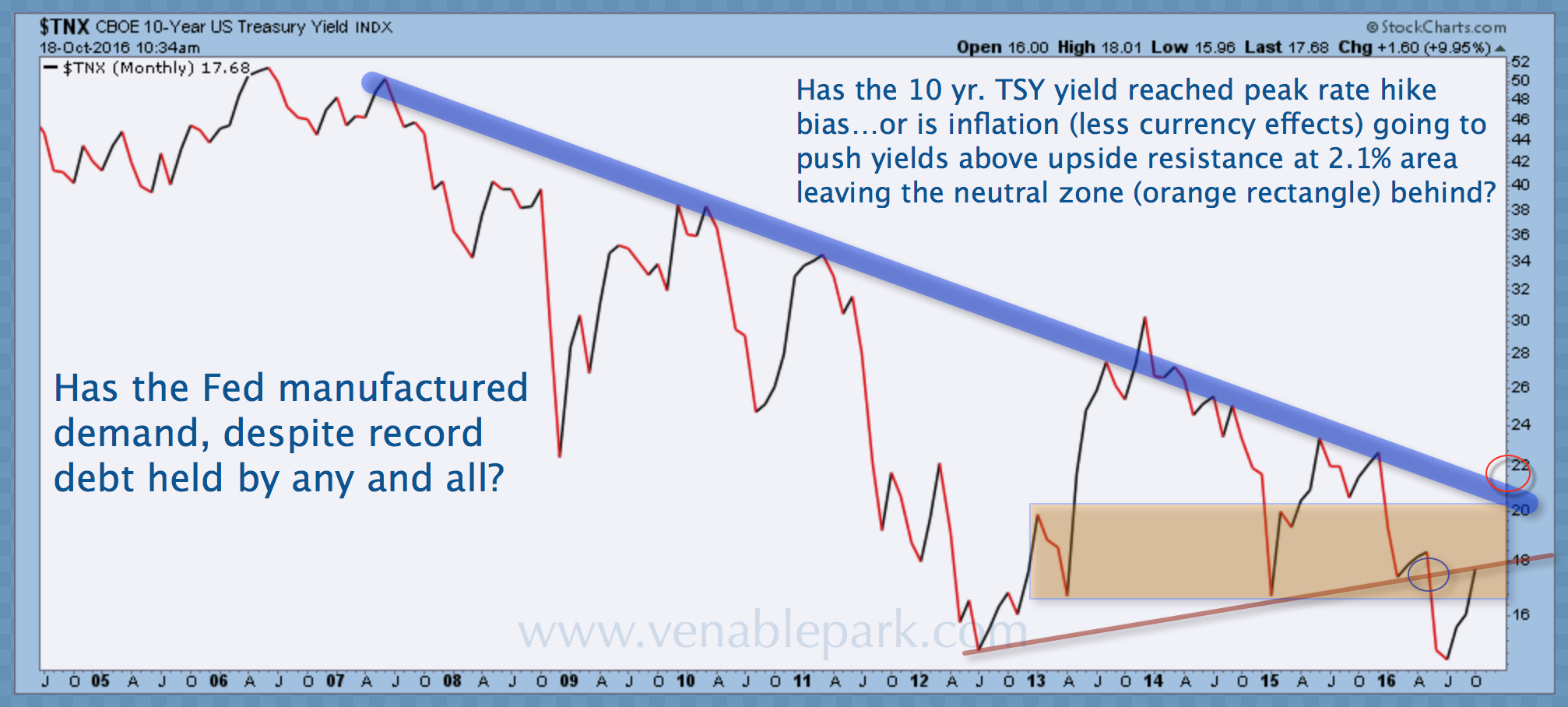

Here is a big picture look at the US 10 year Treasury yield since 2005. With the falling trend since 2007 still in tact (purple line) the back up from all time lows since July is no break out. If the 1.80-2.0 range proves resistance, the lower for longer thesis will be confirmed once more. The Bank of Canada is struggling with monetary impotence as well, see: Poloz poised to mark down recovery, stand pat on rates.

Steven Major, global head of fixed income research at HSBC, and David Bloom, global head of FX strategy at HSBC, discuss their view of lower Treasury yields in 2017. Here is a direct video link.