Central bankers are out in force this week, talking up their growth and inflation expectations once more (that have been wildly optimistic and wrong for years now). In truth they all remain consumed with the same aspirational powers and self-delusion.

Yesterday US Fed Chair Yellen echoed obtuse observations from the Greenspan and Bernanke-led Feds over the past 20 years, saying to an audience in London:

“Would I say there will never, ever be another financial crisis? You know probably that would be going too far but I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will be.”

For a well deserved criticism of Yellen’s comments see: There is no excuse for Janet Yellen’s complacency from economist Steve Keen.

At the same time the Euro rallied the most in a year after ECB head Mario Draghi suggested persistent deflationary forces may be giving way in the Euro zone. Hoping to relieve the resulting currency-carnage for European exporters, today ECB Vice President Vitor Constancio said that market reactions aren’t always understandable and Mr. Draghi didn’t say anything new in regards to ECB policy.

Next up, Bank of Canada’s Stephen Poloz boosted bets for a rate hike at the next July 12 meeting, by saying that Canadian policy rates are “extraordinarily low…It does look as though those cuts have done their job.” The Loonie bounced sharply against the US dollar in response. As shown in this long-term view of the US dollar/CAD ratio since 2009 however, the Canadian dollar, while back to a 4-month high, is so far still within the channel of $US strength that has dominated since 2011 when commodity prices topped out.

But here’s the thing: West Texas Crude (WTIC) was in the $60 and $50 a barrel range when the BOC last cuts rates in January and July 2015. Today WTIC is less than $45 a barrel, global growth has slowed, a protectionist government has taken the White House, and the Canadian economy and households are more indebted and vulnerable to the inevitable and necessary downturn in exuberant realty markets than ever before.

But here’s the thing: West Texas Crude (WTIC) was in the $60 and $50 a barrel range when the BOC last cuts rates in January and July 2015. Today WTIC is less than $45 a barrel, global growth has slowed, a protectionist government has taken the White House, and the Canadian economy and households are more indebted and vulnerable to the inevitable and necessary downturn in exuberant realty markets than ever before.

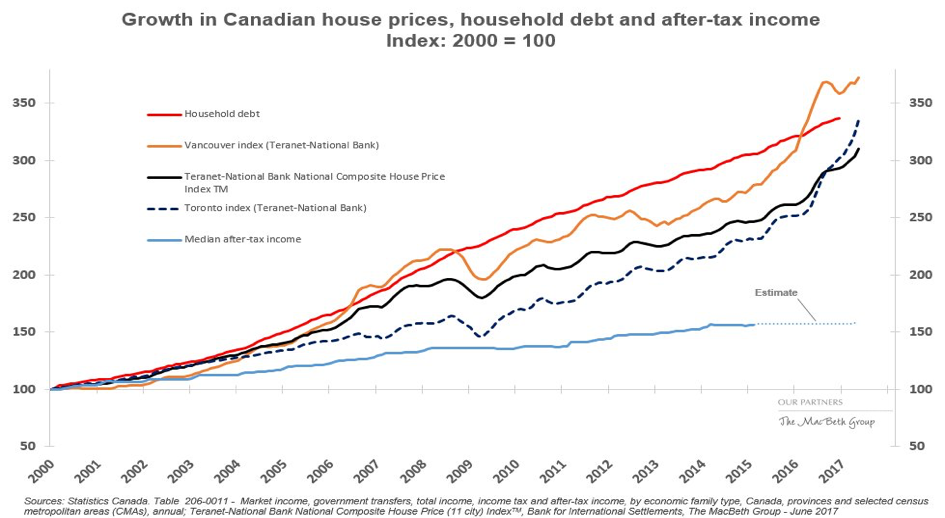

Here’s the chart showing Canadian household debt (in red) versus average home prices (in black) and flat median incomes (at bottom).

No doubt, the BOC (like all zero-bound central bankers) would like to be at higher rates with more monetary torque staring into the next recession. But the fact remains that the Canadian economy is less resilient in 2017 than it was in 2015. Same for the much more indebted global economy, where the debt to GDP ratio has now risen to a record 327% from 276% in 2007.

Central banks orchestrated the present economic mess with years of near zero rates and asset flipping, by all means they should look to back out of their disastrous policies. But pretending that won’t prompt mean reversion in asset markets and the economy, is cowardly nonsense. The monetary piper must be paid. Much better to be prepared, than taken by surprise. But don’t expect bankers and politicians to see anything coming.