Here is a point of reference for the current market cycle: even after a price decline to date of more than 7% from its most recent March 2014 high, the Russell 2000 small cap stock index is currently trading at a (PE) price to 12 month trailing (estimated) earnings of 83!

Indeed all of the quantifiable measures that have proven historically reliable over full market cycles, advise us that from present valuations, future returns for equity and junk bond holders will be negative on every time horizon over the next 7 years–at least.

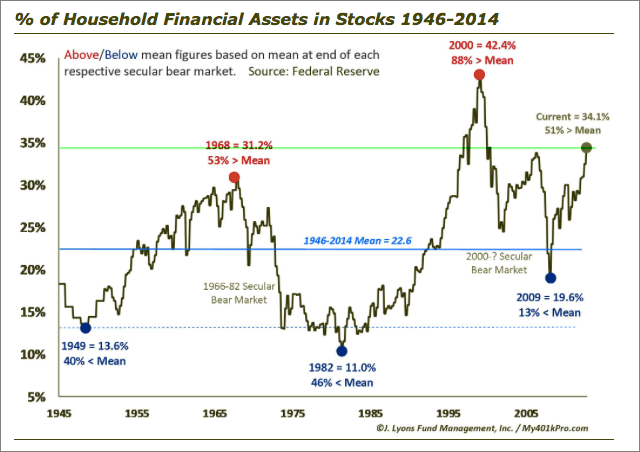

Meanwhile, households who liquidated their risk holdings at 12 year lows in both 2002-03 and 2008-09 and ran for the sidelines have been attracted back like bugs to a flame in the past 12 months of QE-induced mania, and are now holding 34% of their net worth in equities once more. This is a more concentrated risk exposure than at any other time in history but for the late 1990’s. (chart shown here)

It is quite clear that buyers and holders of equities and junk bonds today fall into one of the following groups:

- High frequency traders who purchase advance notice to game the system and skim profits off other slower-moving participants. These participants don’t typically hold trades for more than a second, never mind overnight;

- Those who believe they are ‘long-term investors’ and are irrational or oblivious to the inverse relationship between similar periods of over-valuation and subsequent investment returns;

- Fund managers and pensions mandated by their prospectus/constating documents to be perpetually invested in equities and high yield debt at every point in the market cycle, regardless of capital risk or the individual time horizon of their unit holders;

- Those paid to constantly sell risk to others and so are necessarily reckless or willfully blind to present negative return probabilities;

- Those who are desperate gamblers, doubling down on the miniscule chance that against all odds, they might get lucky and win the lottery.

If you are buying or holding risk assets today, ask yourself a question: which one of the above 5 categories do I fall into? Make sure you are comfortable with your answer…

For those who would rather use, high-probability, math based, objective assessments of investment prospects, John Hussman offered a useful overview at the at the 2014 Wine Country Conference last month. Here is a direct video link.