The four Ds drive real estate listings: death, divorce, default, and discretionary. The first three tend to trigger regardless of market conditions. ‘Discretionary’ and default listings tend to rise with interest rates– both are escalating now.

Ted Oakley discusses real estate with property market expert Ivy Zelman. Here is a direct video link.

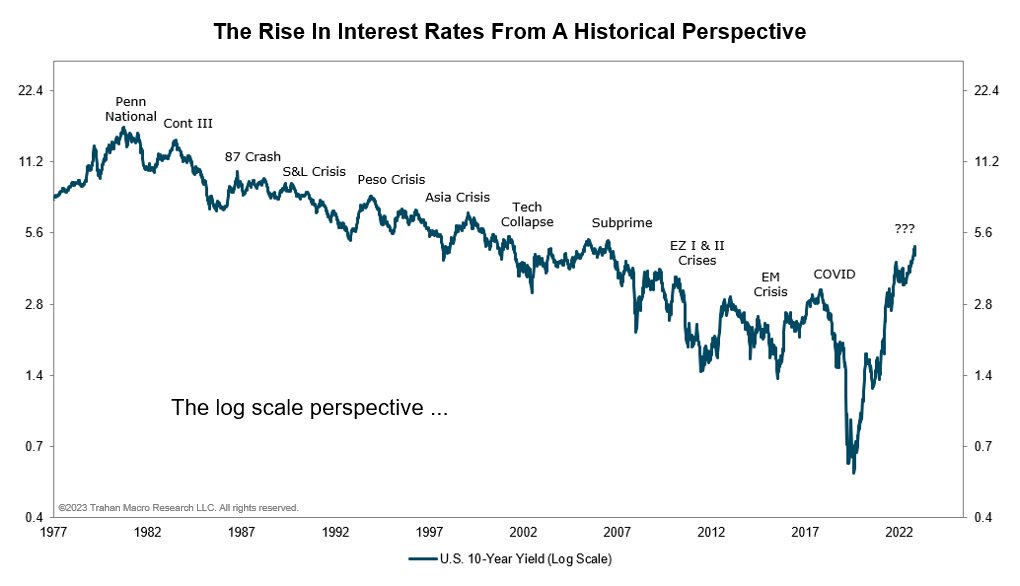

For those who think that interest rates are not high enough to cause significant strain, context is critical. It is the rate of change that matters most. The move from less than 1 percent to more than 5 percent over 16 months is by far the most severe of any previous tightening cycle in at least the last 50 years (chart of the US 10-year yield change in log scale below since 1977 courtesy of Francois Trahan). Moreover, this rate shock hit when all levels of the economy were at record levels of indebtedness—# thisisabigdealfolks.