Hoisington Management’s Third Quarter 2023 Review and Outlook is now available. This is no sugary snack soundbite, but it’s five pages worth digesting. See Impending Recession. Here’s a taste:

The peak in the financial cycle occurred in the fourth quarter of 2021, seven quarters ago. This is right in the middle of the five to nine-quarter average monetary policy lag since World War II.

Monetary conditions have steadily tightened through the end of the third quarter of 2023 and the process is widely expected to hold through the end of the year, and possibly even into 2024.

Historically, these more restrictive conditions will expose, through bankruptcy and liquidation, those who took excessive risk during the monetary largess of 2020 until early 2022.

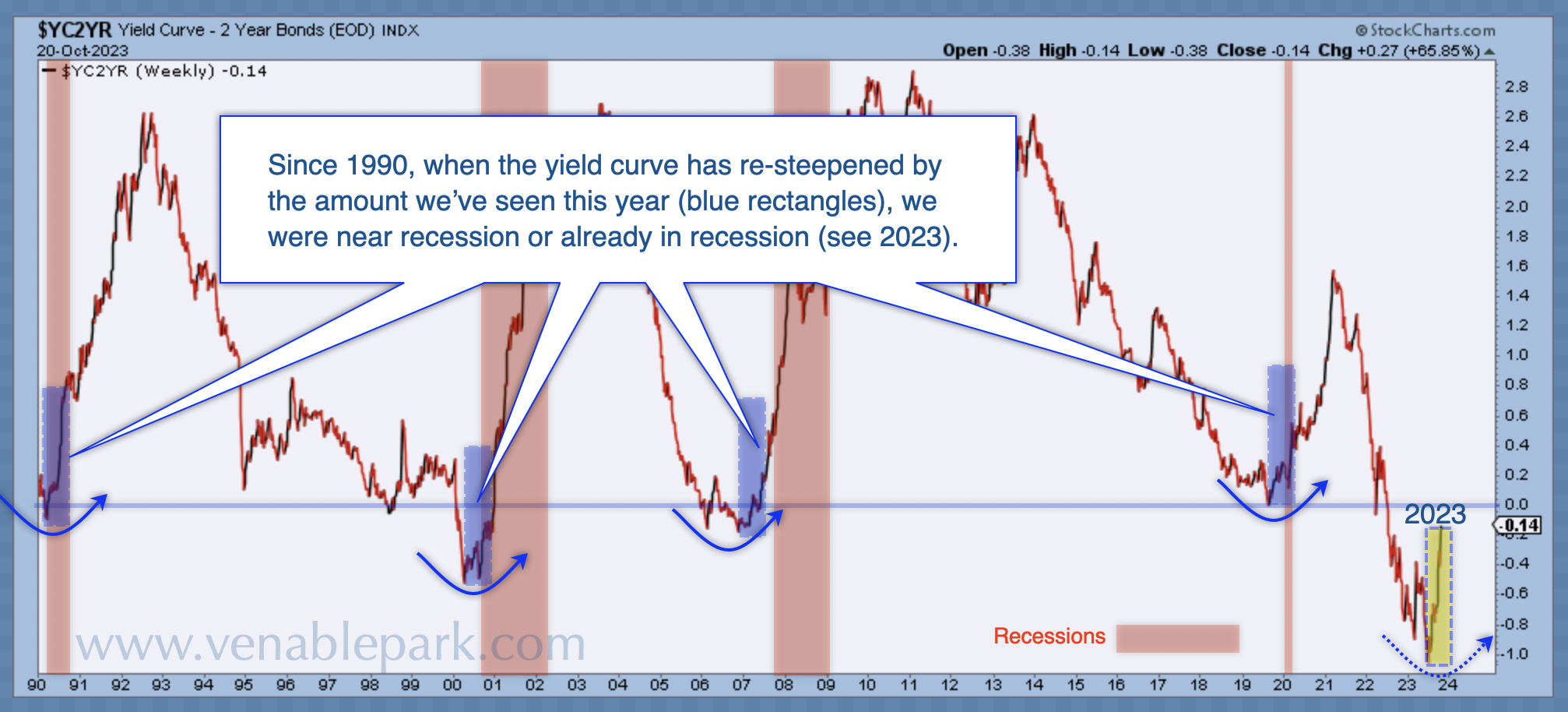

Through September, the yield curve between the two- and ten-year Treasury yields has remained inverted for over twelve months. As Duke Professor Campbell Harvey’s research has shown, this barometer has, without exception, preceded each of the last eight recessions over the course of seventy years. Such developments point the economy in the direction of an economic downturn and lower inflation